Collars

{kind=link}

Learn About Directional Option Strategy

A collar spread consists of a long futures contract, a short call and a long put. The call and put are different strikes. But have the same expiration and the same underlying futures contract.

Traders will collar a futures contract to protect against downside risk of the futures contract. The long-put leg will protect against downside market movements while the premium received from shorting the call will help finance the purchase of the put.

A collar strategy is used when a trader has a long position in the underlying market and wants to protect that position from downward market movement. Executing a collar strategy will cover downside risk but cap the upside potential.

https://www.cmegroup.com/content/dam/cmegroup/education/courses/images/collars-01.jpg

{kind=link}

For example, in June, a trader bought a December futures contract for $100. In July, the future is still trading at $100. The trader still believes the market will move up before expiration, but for the next month, he is worried about the downside and does not see dramatic upside potential.

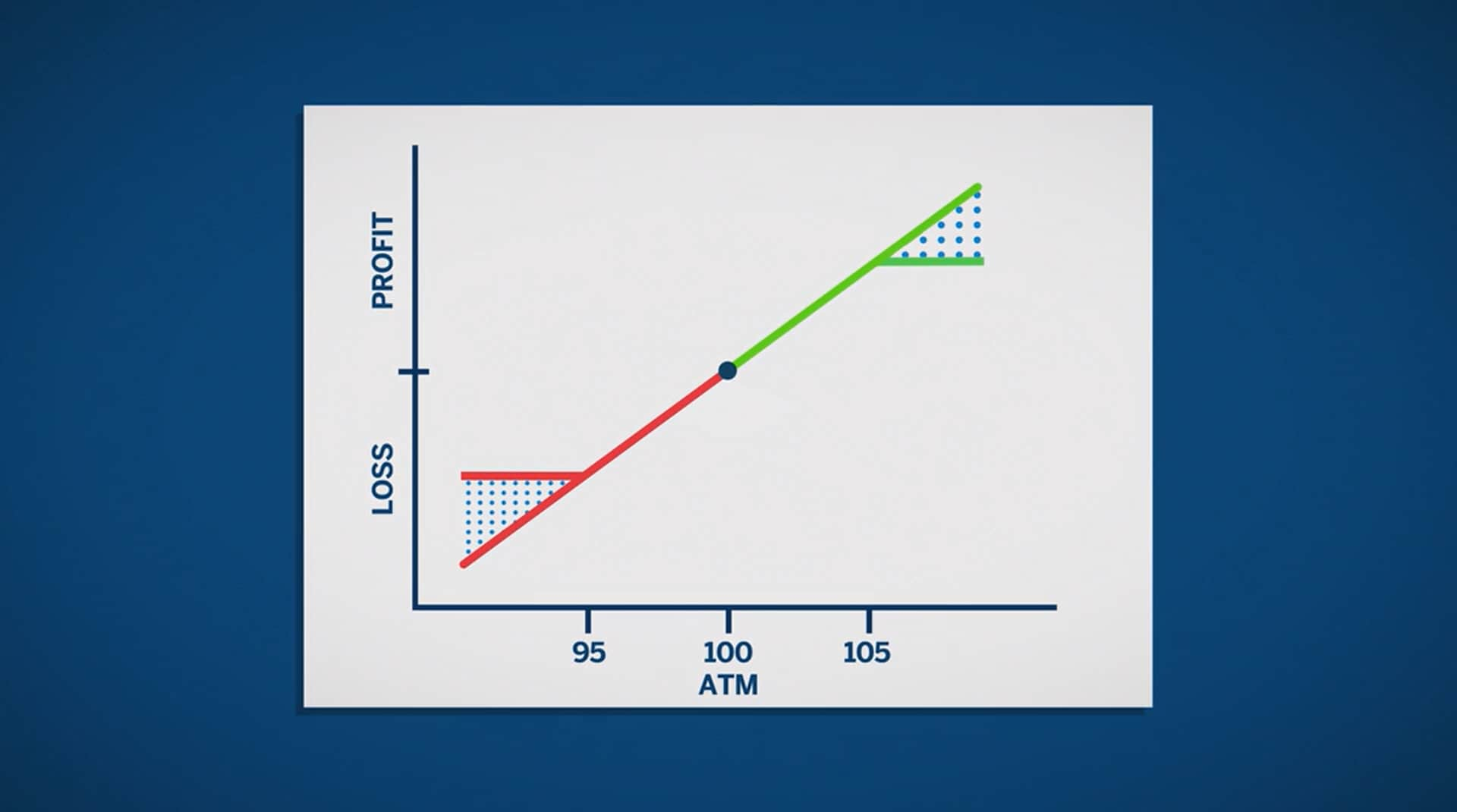

He can manage his risk by buying an out-of-the-money put financed by selling an out-of-the-money call.

He buys the August 95 put for $4 and sells the August 105 call for $4. The spread’s premium is zero.

First, look at the payoff profile for the December future. We can see the unlimited upside potential. Buying the 95 put mitigates the downside risk and the maximum loss for the position is $5.

The dotted area shows the protection provided by the put. Selling the 105 call limits the upside potential to $5 and the dotted area shows the foregone profit from shorting the call. We will look at three different market scenarios for the end of August. One with the underlying market below 95 dollars, one above 105 and the third in the middle.

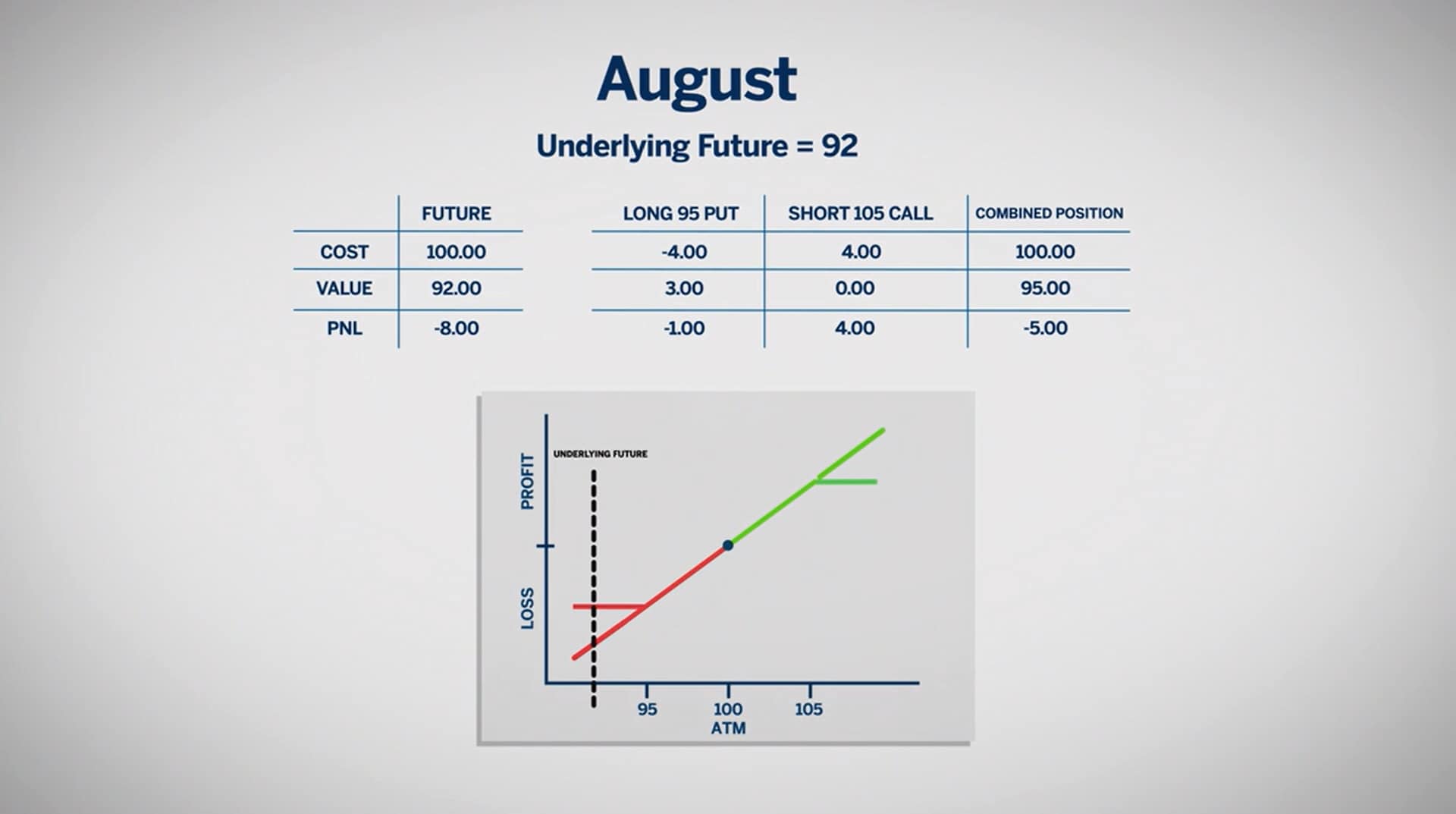

It is the end of August and our options have expired. If the futures ended at 92, the 105 call expires worthless and will not be exercised. The 95 put is in-the-money. Our trader exercises his put, thereby selling his future at 95 thus taking himself out of the market.

Without the put, the trader would have lost $8 on his futures contract. By having the 95, 105 collar, his loss was limited to $5.

https://www.cmegroup.com/content/dam/cmegroup/education/courses/images/collars-02.jpg

{kind=link}

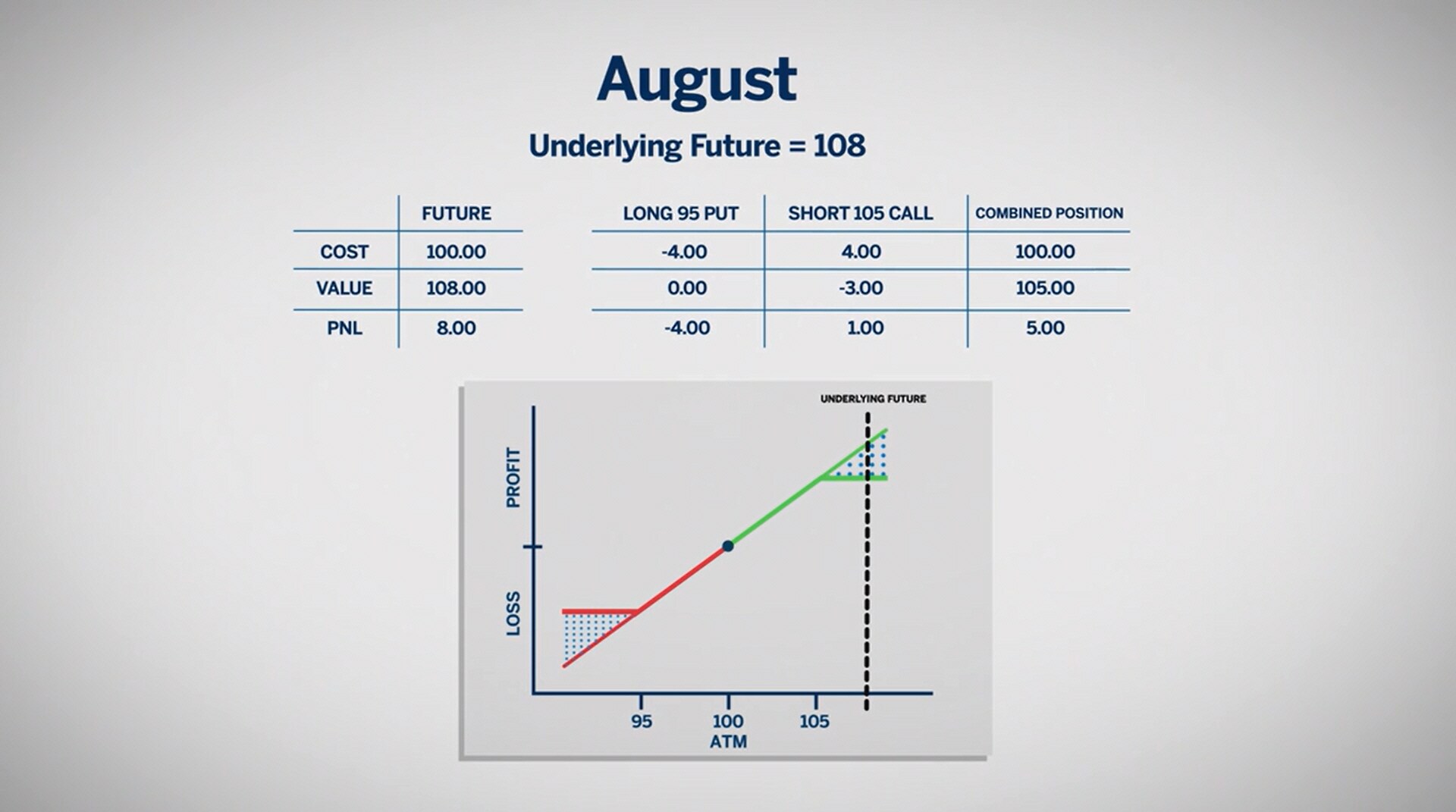

If the futures ended at 108, the 95 put expires worthless and will not be exercised. The 105 call is in-the-money. Our trader is obligated to sell his future at 105 to the call owner. Since the original future was delivered to the call owner, our trader is out of the market.

Without being short the call, the trader would have made $8 on his futures contract. By having the collar, his profit is limited to $5.

https://www.cmegroup.com/content/dam/cmegroup/education/courses/images/collars-03.jpg

{kind=link}

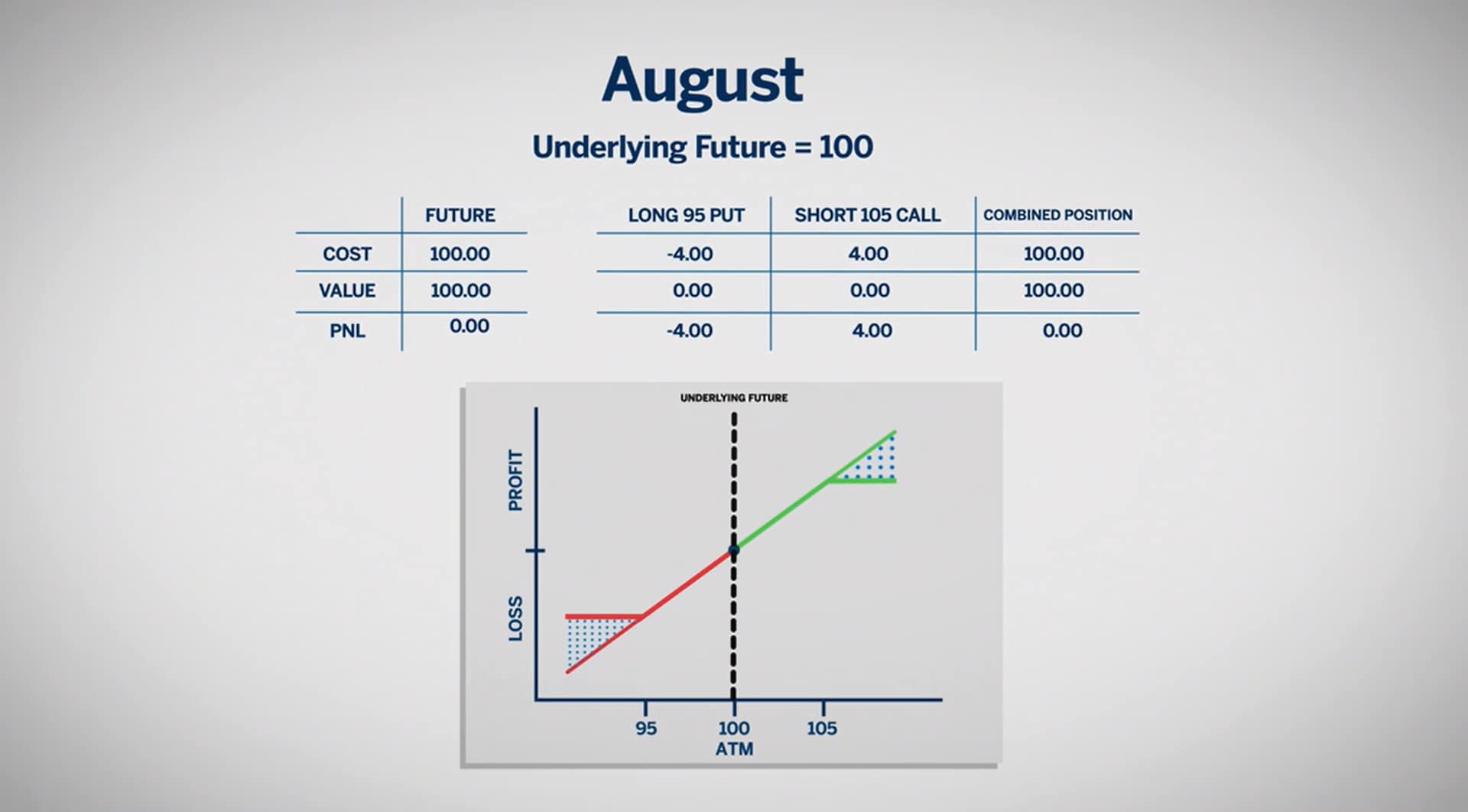

If the futures ended at 100, both the 95 put and the 105 call expire worthless and will not be exercised.

Since neither option was exercised, the trader still holds the original future. Had he not utilized the collar, his position would be the same, namely long one future.

https://www.cmegroup.com/content/dam/cmegroup/education/courses/images/collars-04.jpg

{kind=link}

As we have discussed, if there are significant downward or upward market movements, either option will be exercised. Our trader would need to reevaluate his view of the market and decide on re-initiating a futures position.

Collar spreads allow traders to express an opinion about the market in a defined way - allowing for known maximum profit and loss ranges.