Straddles

{kind=link}

Have you ever heard the saying “straddle the fence?” It means that you support both sides of an issue. Similarly, a common options strategy is referred to as a straddle because a straddle is used when you think the underlying futures market is going to make a move, but you are not sure which way.

Buying a Straddle

If you are buying a straddle, it is referred to as being long the straddle. A trader buys the call and the put of the same strike, same expiration and same underlying product.

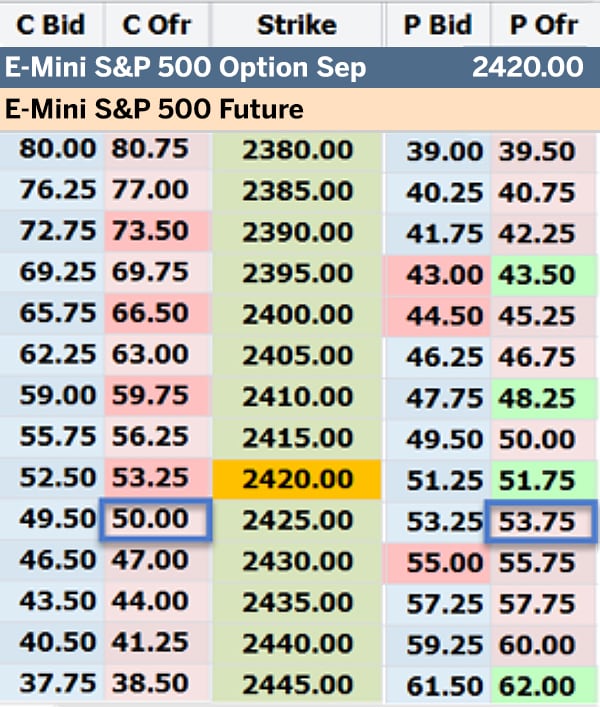

For example, if you want to straddle E-mini Sep 2425, you would buy the E-mini 2425 Sep call and buy the 2425 Sep put. The cost of the straddle in this example would be 103.75.

https://www.cmegroup.com/content/dam/cmegroup/education/courses/images/straddles-01.jpg

{kind=link}

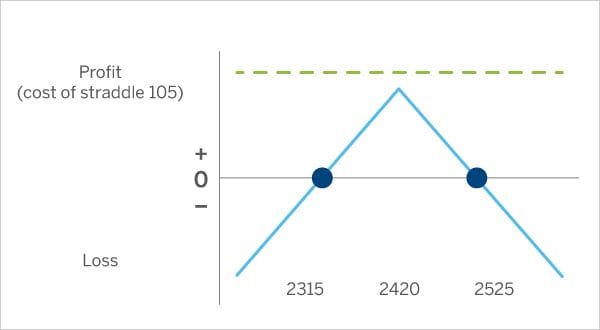

Traders will buy the straddle if they expect the market to start moving but are not sure which way. In our example, the E-mini futures contract would be at 2420 and we expect the future to move up or down but we are not quite sure which way.

The profit potential is much larger than the cost of the straddle in either direction. At expiration, the break-even points are 2525 and 2315. These are the strike plus the straddle cost and the strike minus the straddle cost.

https://www.cmegroup.com/content/dam/cmegroup/education/courses/images/straddles-02.jpg

{kind=link}

Loss is limited to the cost of spread. Maximum loss occurs if the market is at the strike at expiration. Because the straddle is composed of only long options, it loses option premium due to time decay. Time decay is most costly if the market is near the strike.

Selling a Straddle

Traders will sell a straddle, or short the straddle, when they expect the market is going to stagnate. Because the traders are short the straddle, they profit as the options decay, provided the market does not move far from the strike.

Like the long straddle the straddle’s break-even points are at the strike plus the cost of straddle on the call side and the strike minus the cost of the straddle on the put side at expiration. These break-even points are the same regardless if you are long or short the straddle.

For a short straddle, profit is maximized if the market is at the strike price at expiration.

https://www.cmegroup.com/content/dam/cmegroup/education/courses/images/straddles-03.jpg

{kind=link}

Loss potential is open-ended in either direction. Dramatic movements above the strike will make the call much more valuable. Conversely, movements below the strike will make the put more valuable. Because you are short both the call and the put, either case is potentially costly.

Because being short the straddle is essentially short options, you pick up time-value decay at an increasing rate as expiration approaches. You profit from the time decay that the long straddle holder loses. Again, time decay is most profitable if the market is near the strike.