A Look at FX EFP

{kind=link}

An FX Exchange For Physical (EFP), involves simultaneous transactions in the cash and futures markets. EFPs are one type of ex-pit transaction that is allowed to take place outside of the central limit order book under Rule 538.

FX EFP Trade Example

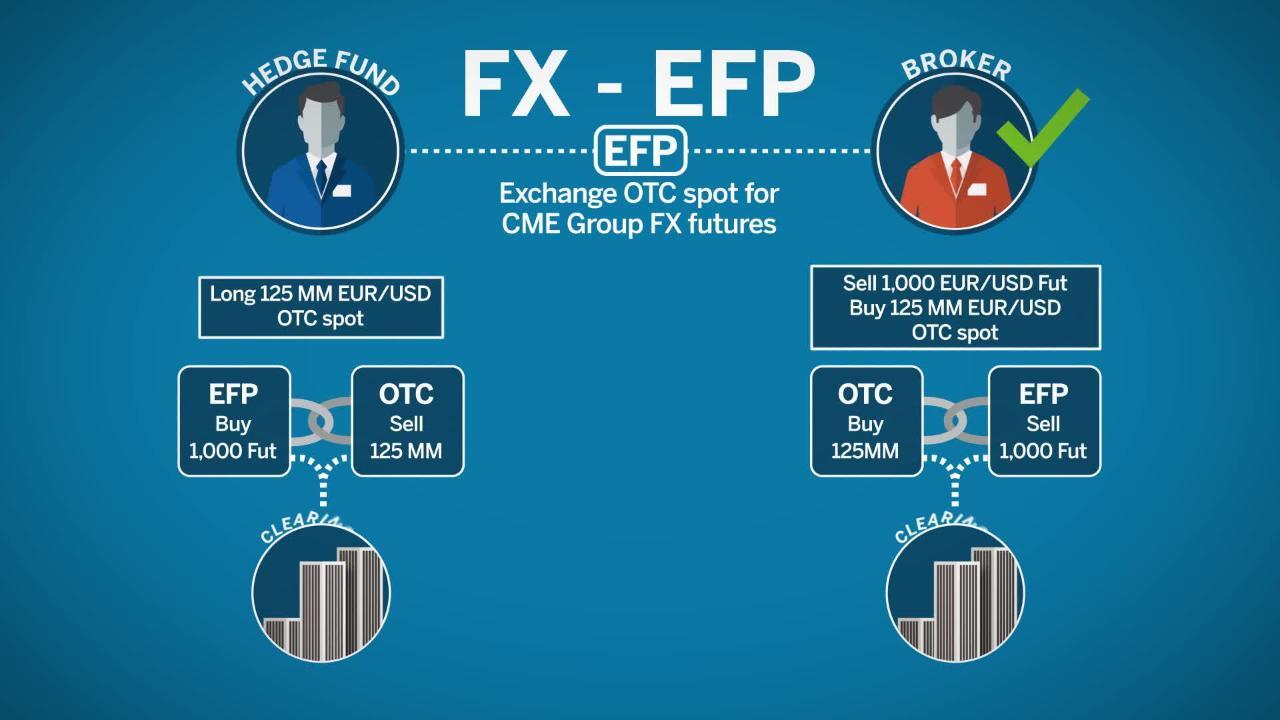

Assume a hedge fund is long a $125 million euro/U.S. dollar (EUR/USD) FX forward in the OTC FX market. He is concerned about counterparty A’s credit risk. One way to mitigate this risk is to utilize futures contracts that are centrally cleared and collateralized.

In this case the OTC FX EUR/USD position can easily be replicated using EUR/USD futures.

To initiate the transaction, the hedge fund contacts his broker to find another counterparty to execute an FX cash versus futures trade (EFP). The hedge fund wants to sell his EUR/USD FX forward position and buy an equivalent position in EUR/USD FX futures using the nearby futures contract. The broker confirms the agreement.

The hedge fund trader writes up his side of the transaction. This consists of two parts, the sell of the cash-side for $125 million EUR/USD FX forwards, and the buy-side of the futures is 1,000 EUR/USD FX contracts.

Why 1 thousand futures contracts?

One euro/U.S. dollar FX futures contract has an equivalent notional value of 125,000 euros.

By dividing the futures contract’s notional value into the existing risk position of 125 million OTC euro/U.S. dollar forward, the result is 1,000 equivalent futures contracts.

The broker writes up the counterparty side of the transaction which is buying $125 million EUR/USD FX OTC forward and selling 1,000 EUR/USD FX futures.

Both parties report their side of the transaction to their respective clearing firms which in turn submit each trade to the clearinghouse. Once the trades are submitted to the clearinghouse, the long futures positions reside in the books of the hedge fund and the short position on the broker’s customer account. The transaction is complete and these new futures positions are just like any other open futures positions. They are subject to margining and can be offset at any time.

The hedge fund now has the euro/U.S. dollar position exposure it wants, and has also mitigated counterparty credit risk by using centrally cleared EUR/USD FX futures.

Immediately Offsetting FX EFP Example

This time assume there is a Commodity Trading Advisor (CTA) who manages money for their customers.

The CTA sees depth and liquidity in the FX OTC market and decides to negotiate a $50 million AUS/USD OTC forward on behalf of his accounts under management.

Immediately thereafter the CTA decides to convert the OTC exposure to futures.

The CTA and the counterparty decide to negotiate and execute an EFP, whereby the quantity of the $50 million AUS/USD OTC forward, originally executed, would cancel out with the $50 million AUS/USD OTC forward of the EFP.

The accounts under management would be left with AUS/USD futures.

In this scenario, because it is an immediately offsetting FX EFP executed by a CTA, the initiating and offsetting cash legs are not required to be passed through to the customer who received the exchange contract as part of the EFP. However, in a circumstance where the futures leg of the transaction fails to clear, the underlying accounts under management must receive the profit or loss of the offsetting cash leg.