FX Options Vol Converter

{kind=link}

OTC FX options market participants have a growing awareness of the benefits of central clearing, and of the extensive electronic pricing and transparent volatility surfaces available at CME Group – but how does this liquidity compare with pricing of OTC FX options?

With their standardized strikes and maturities, price quoting - and in some pairs their flipped quotation, and delivery into futures, listed options are difficult to compare with their OTC counterparts.

{kind=link}

However, fundamentally CME Group and OTC volatilities are essentially the same. Similarities in the underlying convergence, European style expiration, 10 am New York expiration time, and a T+1 valuation date provide a strong non-arbitrage relationship between the OTC and futures markets.

About the tool

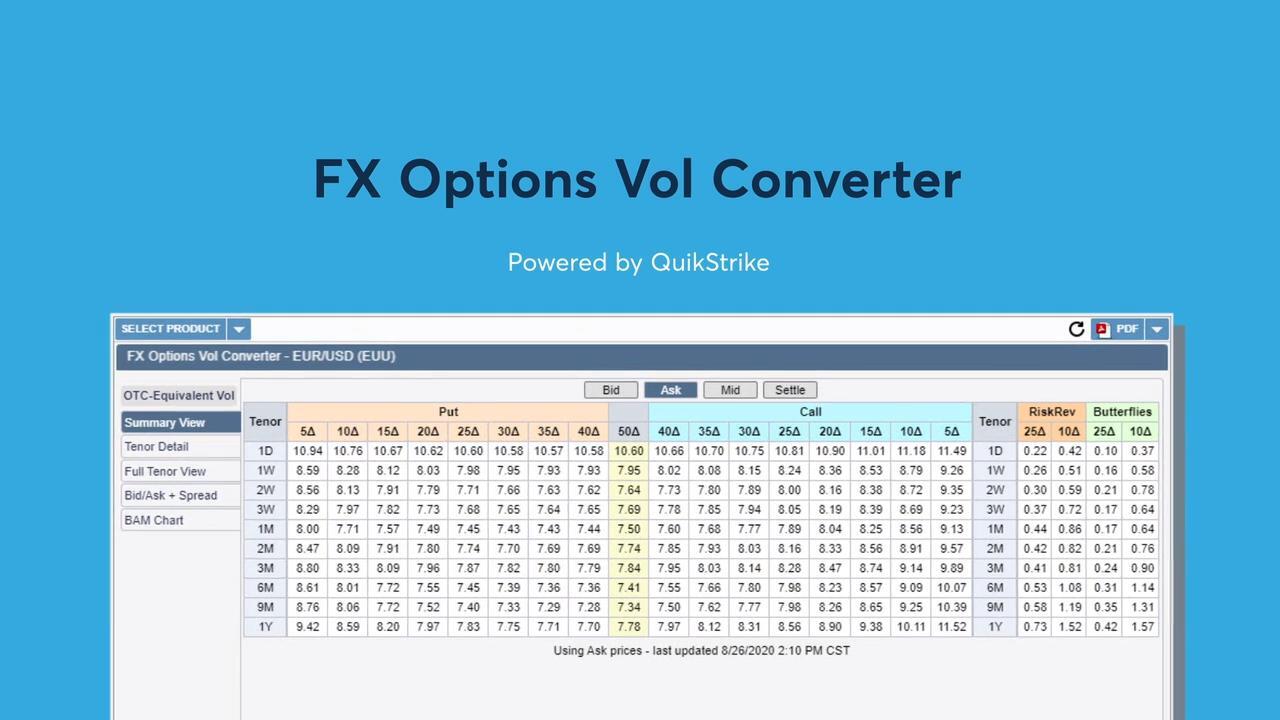

The FX Options Vol Converter, powered by QuikStrike, calculates listed options pricing available on CME options into an OTC-equivalent volatility surface, allowing OTC users to easily compare pricing and monitor price relationships between both options markets.

In the conversion process, the CME premium price for all strikes and maturities are adjusted, converted, and interpolated based on well-studied, quantitative option models and methodologies, resulting in a precise, continuous OTC-equivalent volatility surface for each currency pair. The FX Options Vol Converter summarizes thousands of datapoints into one succinct volatility surface for easy viewing, and the drilldown functionality allows users to quickly pinpoint the most relevant instruments for their strategy.

Example

Assume a trader receives offer quotes of 7.85% and 7.9% from two OTC pricing sources for a two-week, 35-delta put on Euro/USD. They are also interested in checking the option pricing available through CME Group as they would like to work their order on the central limit orderbook, and subsequently, clear the trade through CME Clearing.

Referring to the FX Options Vol Converter, the trader can access the main Summary View page and select the ASK market side to view the theoretical value of a similar two-week, 35-delta put implied by streaming offer prices on CME Group contracts. The implied volatility is shown as 7.63%, which is a better price than was quoted by their OTC pricing sources.

By clicking on the displayed volatility, the trader can view a dropdown of the CME Group options instruments that are most responsible for generating the data point. The contracts are displayed along with their symbol, strike, and price inputs – allowing the trader to quickly select the contract on their CME trading system, evaluate against live quotes, and execute the trade ‒ if desired.

The FX Options Vol Converter tool is available for these currency pairs: EUR/USD, GBP/USD, AUD/USD, JPY/USD, and CAD/USD.

Live data updates are made every weekday with settlement views available both during and outside the live update periods. Multiple views are available, including Summary, Full Tenor , and Bid-Ask-Mid ‒ allowing users to select the view that best fits their trading style.

The FX Options Vol Converter calculates and converts listed CME Group FX options data into an OTC-equivalent volatility surface, providing price transparency between the two markets and allowing for more informed trading decisions.

Try the FX Options Vol Converter