{kind=link}

Veg Oil vs. Crude Oil: Tail Wagging the Dog

Crude oil lies at the heart of our economic universe. Its byproducts gasoline, diesel and jet kerosene essentially serve as humanity’s only viable transportation fuels. From cosmetics to medicines to the ubiquitous plastic bottle, crude oil touches our lives in a myriad of ways, at times even without us knowing of it. Its presence is also felt strongly in the daily trading cycles of the various markets across the world, and we have written copiously this year on how changes in crude oil prices tend to move equity markets, and can cause certain equity sectors to outperform or underperform against major indices. Trading volume in crude oil and its products typically run into the tens of billions of dollars per day. However, despite its strategic heft, West Texas Intermediate (WTI) crude oil prices have, over the past 15 years, consistently followed in the footsteps of a modestly traded product: vegetable oils. More specifically, soybean oil and palm oil can be said to be the tail that wags the dog (Figures 1 and 2).

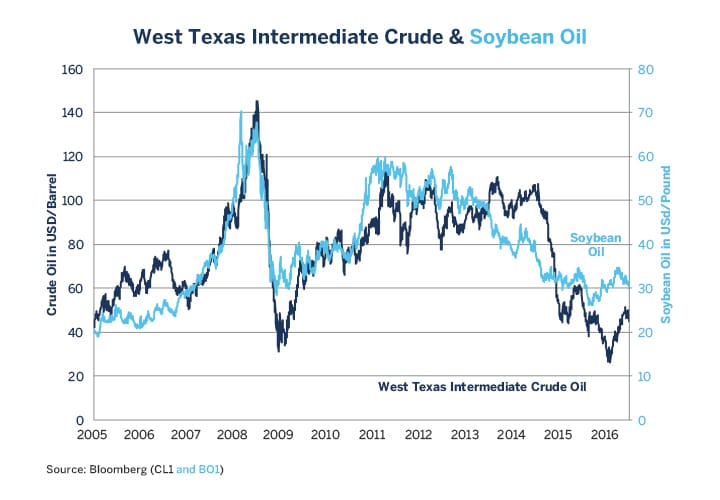

Figure 1: Soybean Oil: A Leading Indicator of Crude Oil?

https://www.cmegroup.com/content/dam/cmegroup/education/images/articles/veg-oil-vs-crude-oil-01.jpg

{kind=link}

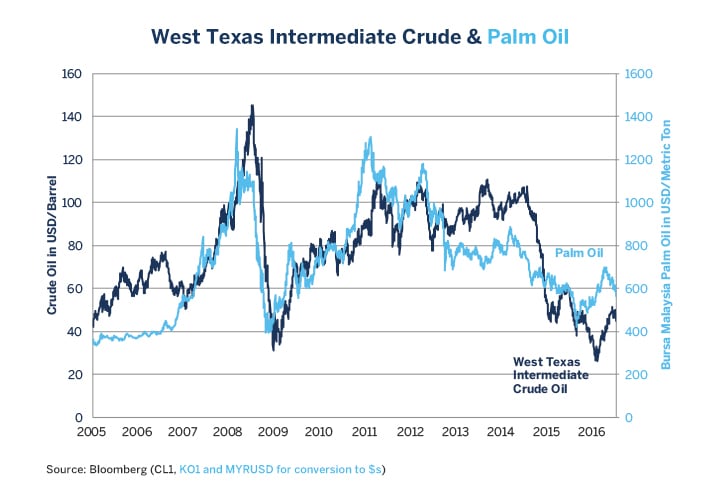

Figure 2: Palm Oil (in USD) has also Tended to Lead Crude Prices.

https://www.cmegroup.com/content/dam/cmegroup/education/images/articles/veg-oil-vs-crude-oil-02.jpg

{kind=link}

Vegetable oils leading price movements in crude oil began to be noticeable exactly 10 years ago. In the summer of 2006, WTI oil prices peaked at a then-record high of $77 per barrel, and by January 2007 had crashed to $51. Vegetable oils were unmoved by the crude oil correction and continued to rally, foreshadowing the powerful resumption of the crude oil bull market that took prices to over $140 by July 2008. Since then, vegetable oil markets have tended to lead crude oil on a number of bull and bear moves, including:

- Vegetable oil prices peaked in March 2008, four months before crude oil prices reached their all- time highs in July of that same year.

- Palm and soybean oil prices hit bottom in November and December 2008, two to four weeks before the bottoming of crude oil prices. By the time crude oil prices had regained their footing in February and March 2009, soy and palm oil were well into a rally.

- Vegetable oil prices reached their post-crisis peak in February 2011, almost three months before crude prices peaked out at the end of April 2011.

- While crude oil prices range-traded between $80 and $115 per barrel from 2011 through mid-2014, vegetable oil prices began a long bear market that foreshadowed the abrupt collapse of crude oil in late 2014.

- Soy and palm oil prices bottomed in August and September 2015, almost six months before crude oil prices hit bottom in January and February 2016.

- Vegetable oils peaked out in April 2016 and have since begun to correct, possibly indicating a slide in crude prices that might have begun this month.

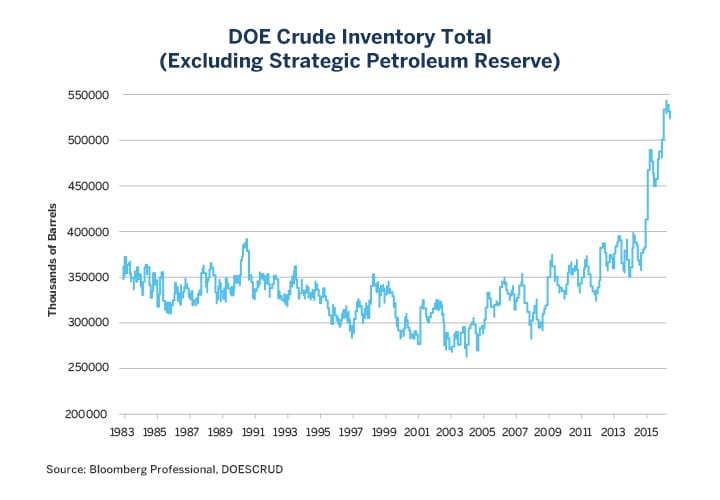

Figure 3: High Levels of Inventories Might Bode Ill for Crude Oil Prices This Summer.

https://www.cmegroup.com/content/dam/cmegroup/education/images/articles/veg-oil-vs-crude-oil-03.jpg

{kind=link}

We are not certain why vegetable oils appear to lead crude prices, but one possibility is that when there is too much crude oil, vegetable oils get squeezed out of fuel blends or at least have their use reduced. By contrast, when there is a shortage of crude oil, vegetable oils might find themselves suddenly in higher demand. Producers may also not be as willing or able to store vegetable oils as they might for crude oil, which has seen massive fluctuations in storage levels (Figure 3).

Bottom line: Vegetable oil traders often look to crude oil markets for guidance on pricing, but crude oil traders might be well advised to look at the behavior of soybean oil and palm oil as a possible leading indicator of movements in crude prices.

Recommended For You

View this article in PDF format.