Trading Opportunities in Equity Index Futures

{kind=link}

Trading Opportunities

Due to their wide acceptance as benchmarks and deep liquidity, Equity Index and Select Sector futures can be used by risk managers and traders for a variety of purposes. These flexible products can be employed in numerous trading and hedging strategies.

Possible Trading Strategies

Examples of possible trading strategies include:

- Outright bull/bear directional trades

- Beta replication/beta adjustment

- Portable alpha

- Conditional rebalancing

- Spreads

- Sector rotation

Index Spreads

Another possible trading strategy is an index spread. A spread is the simultaneous purchase and sale of two futures contracts. An index spread is a common and effective trading strategy. The strategy is designed to express the relative value between index contracts rather than an outright market direction bias.

How Spreads Are Used

Outright long or short positions in Equity Index futures can be easily established to reflect a trader’s point of view regarding that index’s next directional move or trend. For example, if a trader believes that the S&P 500 Index is over-valued and will trade lower soon he may sell E-mini S&P 500 futures to express that view.

Asset managers that want to use Equity Index futures to replicate exposure to an index may buy futures contracts and use the residual capital for cash management purposes or alpha producing tactical strategies.

Another possible trading strategy is an index spread. Consider an index spread, specifically, spreading the NASDAQ-100 to the S&P 500.

Advantages of Index Spreads

Because spread trades involve both a long and a short position in highly correlated contracts, they are generally viewed as less volatile and therefore less risky than an outright position in a single contract. Additionally, since spread positions generally reflect lower market risk, there are lower margin requirements.

Example of an Index Spread

Let’s look at an example of a possible equity index spread. The NASDAQ-100 Index is heavily weighted to the technology sector. The S&P 500 Index, by contrast, is recognized as having a broad, diversified constituency and represents the broad market. What makes this type of trade possible is both of these indices, while slightly different, have a high degree of price correlation. In other words, they tend to trade directionally in a similar pattern.

{kind=link}

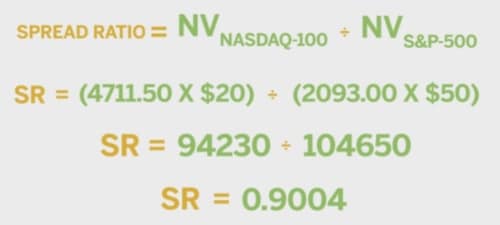

In order to construct this spread, we must first calculate a Spread Ratio. The spread ratio is defined as the notional value of one index future divided by the notional value of another.

In this case, we will divide the notional value of the NASDAQ-100 futures by the notional value of the S&P 500 futures.

How the Trade Might Play Out

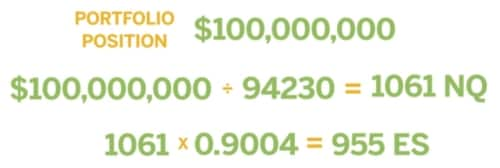

A portfolio manager (PM) believes the tech sector is at risk versus the broad market. He is willing to express this opinion with a $100 million equivalent risk position, leading the PM to take the following actions:

The PM sells the E-mini NASDAQ-100/E- mini S&P 500 spread. First calculating the spread ratio, the notional value of the NASDAQ Index equal to 4711.50 x $20 dollars, or $94,230 per contract divided by a notional value of E-mini S&P of 2093.00 x $50 or one $104,650 per contract. Our spread ratio, then, is equal to $94,230 ÷ $104,650 per contract. This comes to 0.9004 E-mini S&P 500 futures for every one E-mini NASDAQ-100 futures.

{kind=link}

Divide the notional value of the E-mini NASDAQ-100 futures into the $100 million dollar risk assumption, and you get 1061 NASDAQ-100 futures contracts. Applying the spread ratio of 0.9004 to 1061 results in an equivalent E-mini S&P 500 futures position of 955 contracts. Since the trader believes the tech sector is overvalued versus the broad market, he will sell 1061 E-mini NASDAQ futures and simultaneously buy 955 E-mini S&P 500 futures.

{kind=link}

At this point, the trader believes the valuations have normalized. Now, he simply unwinds the spread by executing orders opposite to the original trade. He would do this by purchasing E-mini NASDAQ futures and selling the E-mini S&P 500 futures.

Summary

Many trading and hedging strategies can be employed using Equity Index products offered by CME Group.