{kind=link}

Why are Bonds Calm About Inflation?

Bonds: What’s Behind the Calm on Inflation

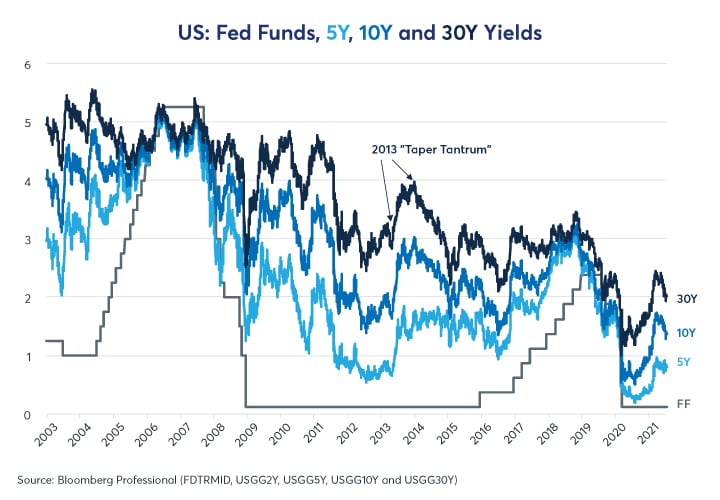

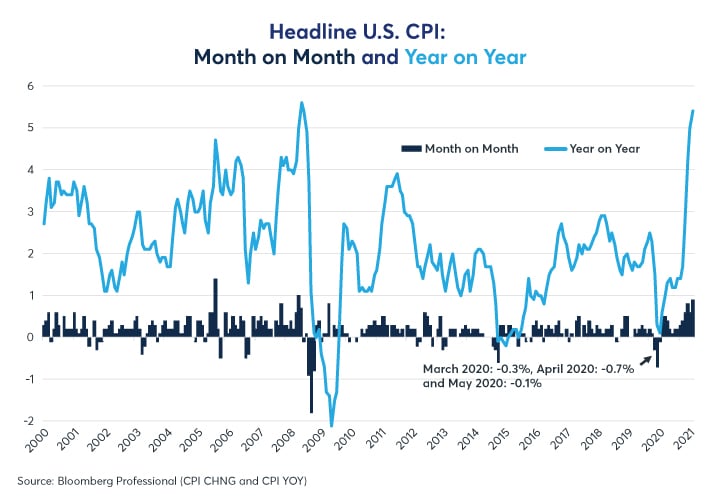

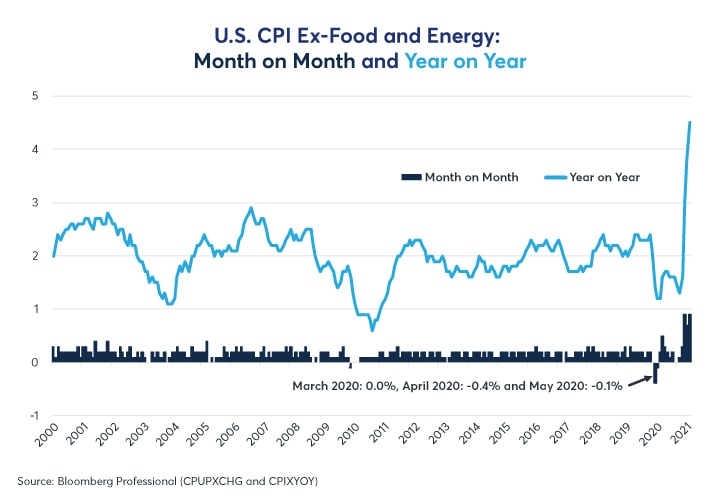

In the 24 hours after the release of the June consumer price index (CPI) report, the U.S. bond markets barely budged. Yields rose about four basis points (bps) on the day of the report only to fall back a similar amount the day after. More broadly, bond yields have fallen sharply at the long end of the curve over the second quarter of 2021 (Figure 1) even as headline and core inflation advanced at a 9-10% annualized pace in that period, and at a 5.4% in June and 4.5% (excluding food and energy) on a year-over-year basis, their highest in decades (Figures 2 and 3).

Figure 1: 10Y and 30Y Treasury Yields Fell in Q2 2021 Even as Inflation Surged

{kind=link}

Figure 2: Headline CPI Rose at an Annualized Pace of 9.3% in Q2 and 5.4% YoY, Highest Since 2008

{kind=link}

Figure 3: Core CPI Rose at 9.9% Annualized Pace in Q2 2021 and 4.5% YoY, the Highest since 1991

{kind=link}

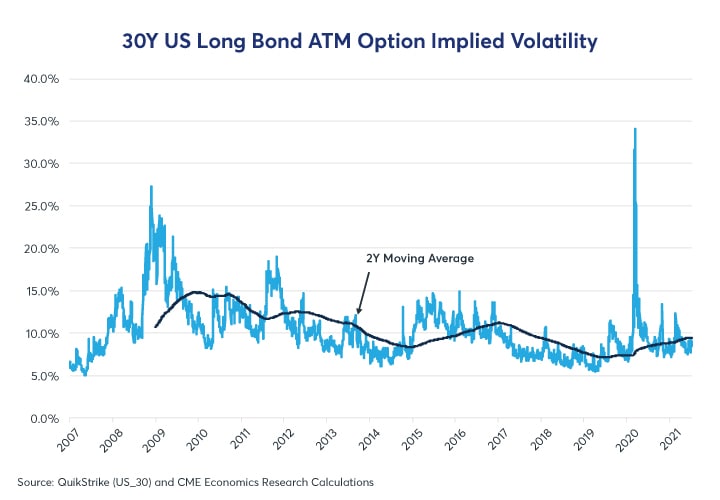

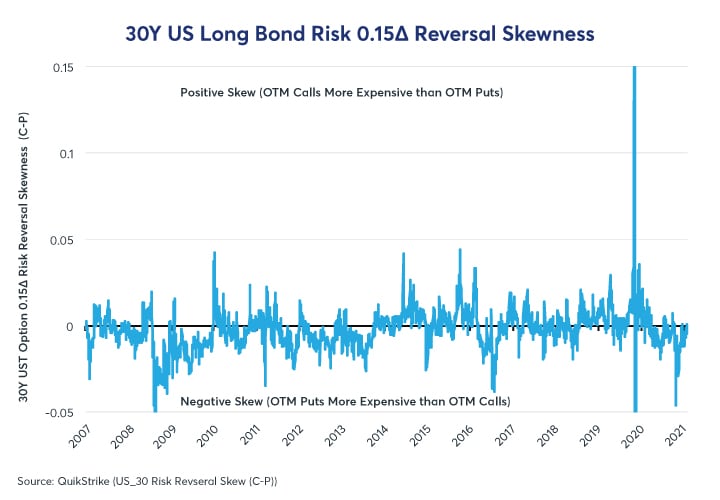

Bond options, too, don’t seem particularly concerned by the recent rise in inflation. Implied volatility on 30Y U.S. Long Bond options are trading at fairly average levels by historical standards (Figure 4), and the skewness of those options shows that investors price roughly equal upside and downside risks (Figure 5).

Figure 4: Implied Volatility on Treasury Long Bond Options is Close to Post-2007 Median Level

{kind=link}

Figure 5: Out-Of-The Money Put and Call Prices Suggest Investors See Balanced Risks

{kind=link}

On thing is certain: bond investors and central bankers are on the same page when it comes to inflation -- both appear to believe that the recent surge in prices is “transitory” and will not become a permanent feature. Bond market prices don’t really come close to pricing an alternative scenario. So, what are the arguments against a sustained rise in inflation? There are several possibilities:

- Supply chain disruptions won’t last: each supply chain disruption is an opportunity for a firm to make exceptional profits by providing the goods or services in short supply. With corporate tax rates still at 21% and personal income and capital gains tax rates not rising, there has been no change to the incentives to work or invest. The argument is that the invisible hand will guide market participants to resolve the supply chain issues.

- Labor shortages may come to an end quickly. Enhanced unemployment benefits, which have changed incentives for lower wage workers, have already been curbed in over 20 states and will be curtailed across the U.S. by the end of September. This could create a surge in job seekers in Q4 2021; their entrance into the labor market could hold down wage growth.

- Higher current commodity prices could encourage increased commodity production in the future: the cliché that high prices are the cure of high prices often proves true over the long term.

- Recent upside drivers of CPI, like used cars and rent, are temporary distortions that will fade over time.

- Markets price Fed tightening in late 2022 and early 2023, and apparently see the central bank as being proactive about raising interest rates and not being behind the curve.

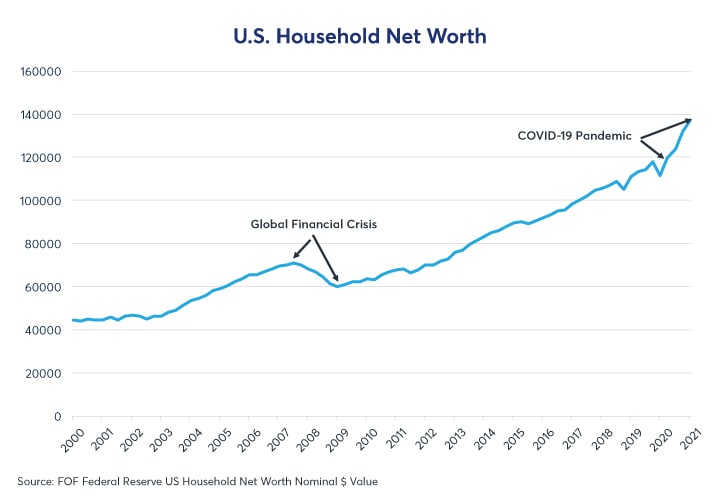

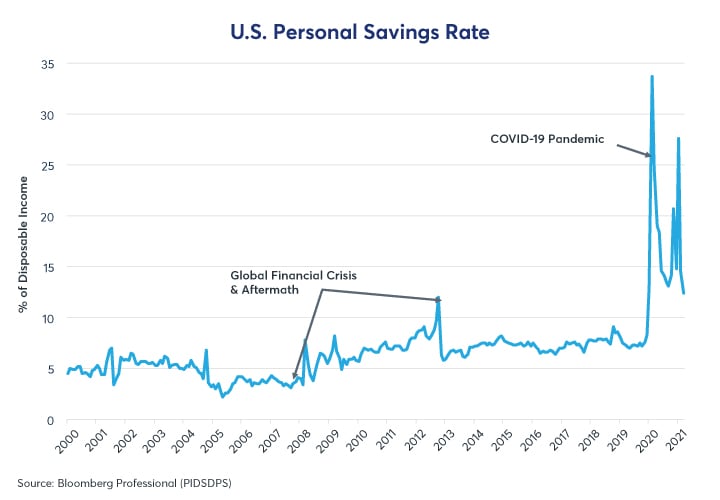

Those arguments are all well and good, but what if they don’t pan out? What if the high savings and soaring personal net worth fuel an economic boom even after the fiscal stimulus ends? In the aftermath of the global financial crisis, household net worth plunged 15%; since the end of 2019, it has risen 16% (Figure 6). And savings rates remain high: U.S. households saved 12.4% in May, compared to 7.3% on average in the nine months before the pandemic began (Figure 7).

Figure 6: Falling Household Wealth Hobbled the Last Recovery, but Rising Wealth is Fuelling the Current Expansion

{kind=link}

Figure 7: Savings Rates are Falling but Still Remain Well Above Pre-COVID Levels

{kind=link}

What if Congress passes an additional $600 billion or so for infrastructure on top of an expanded Federal budget? What if consumers and businesses come to expect higher inflation in the future and rush to spend and invest their cash before prices rise further? What if the Fed is behind the curve and acts too slowly to reign in economic growth and inflation?

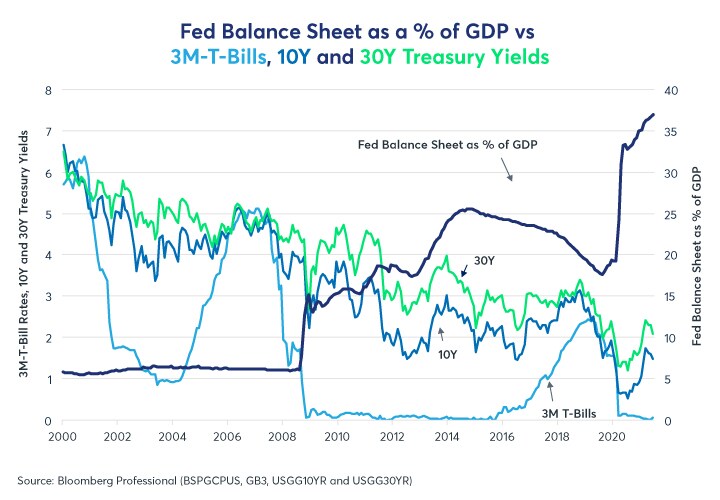

Clearly, some market commentators are worried about these possibilities. The bond market doesn’t seem to price these risks at all. For an economy that is surging, the U.S. yield curve is remarkably flat – a spread of just 190bps separates 3M T-Bills and 30Y Treasury Long Bond yields. In the early stages of previous expansions, the spread was usually closer to 400-500bps. But this opens up one final possibility: bond investors are, in fact, worried about overheating and inflation but four rounds of quantitative easing (QE) over the past dozen years have distorted the Treasury market to such an extent that market prices no longer reflect investor beliefs about future economic growth or inflation; rather, they primarily reflect an expectation for continued Fed asset purchases (Figure 8).

Figure 8: Did QE 1 to Q4 Distort the Bond Market Beyond Recognition?

{kind=link}

This latter possibility is particularly worrisome because with the short-end of the yield curve pricing Fed rate hikes as early as a year from now, the long-end of the yield curve may be woefully ill-prepared for the tapering of QE that might precede a series of rate hikes. In May 2013, when the Fed announced a tapering of QE, bond yields began to rise sharply. Within seven months the 10Y Treasury yield rose from 1.36% to 3.05%, dealing long positions an 18% capital loss in the process. More broadly, many other markets from real estate to technology appear to be predicated on the assumptions of long-term bond yields staying low for a long time. As such, if and when a bond reckoning comes, bond investors are unlikely to suffer the consequences alone.

Bottom Line

- Bonds price the Fed scenario of stable long-run inflation.

- Bond options implied volatility don’t reflect any usual degree of concern about inflation risks.

- QE may have distorted the bond market such that its prices no longer reflect investor views about growth and inflation.

- Increased household wealth and high savings rates might fuel continued strong growth.

- Current bond market pricing leaves markets vulnerable to a 2013-style taper tantrum.

Treasury Products

U.S. Treasuries are standardized contracts on U.S. government notes or bonds that offer a wide variety of strategies for customers to hedge or assume risk based on interest rate market exposure.