{kind=link}

China's Li Keqiang Index: Headwinds for Commodities?

China’s Li Keqiang Index: Headwinds for Commodities, Currencies?

The official growth rate of China is of intense interest to economists and investors worldwide. The gross domestic product of the world’s second largest economy is also subject to a certain degree of skepticism. Observers ponder over its unusual stability and unfailing ability to fall within the consensus estimate. Among the skeptics is none other than Li Keqiang, the Premier of the People’s Republic of China. His remarks to a U.S. diplomat a decade ago describing the official GDP as “man-made,” inspired The Economist to create an index of his three preferred measures of economic growth in China that now bears his name: the Li Keqiang index.

The index, which comprises the annual growth rate of outstanding bank loans (40%), electricity consumption (40%) and rail freight (20%), shows a significantly more volatile trajectory for China’s growth than the official GDP. By the measure, China’s 2015 slowdown was much worse than the official GDP indicates, and the subsequent rebound much bigger. That the index is volatile should not be surprising as it narrowly focuses on just three sectors, would show more variability than a broader measure such as GDP.

Just as there are skeptics of the official GDP, there are those who doubt the Li Keqiang index. Several times in the past few years, the index has been pronounced dead. However, to loosely paraphrase Mark Twain, rumors of the death of the Li Keqiang index have been premature.

While the debate over the ideal measure of China’s economic performance is an interesting and important topic, this paper aims for a more modest and testable goal. It seeks to answer the question: which index, official GDP or Li Keqiang, is more relevant to investors? The answer, as we demonstrate below, is resounding: the Li Keqiang index dominates China’s official GDP in its importance to commodity and currency investors.

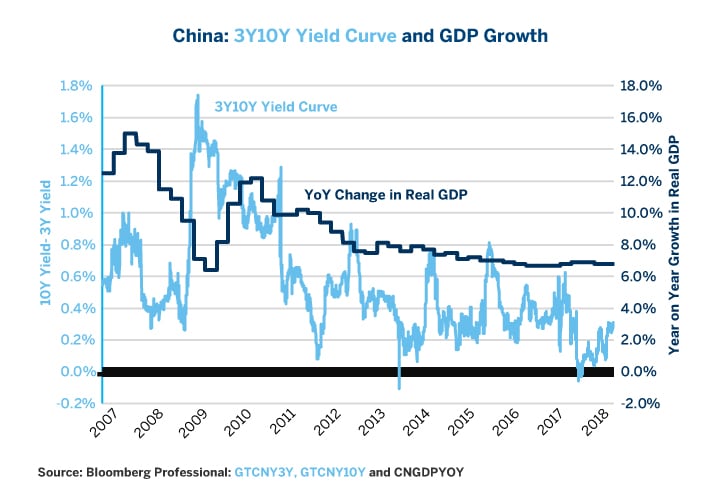

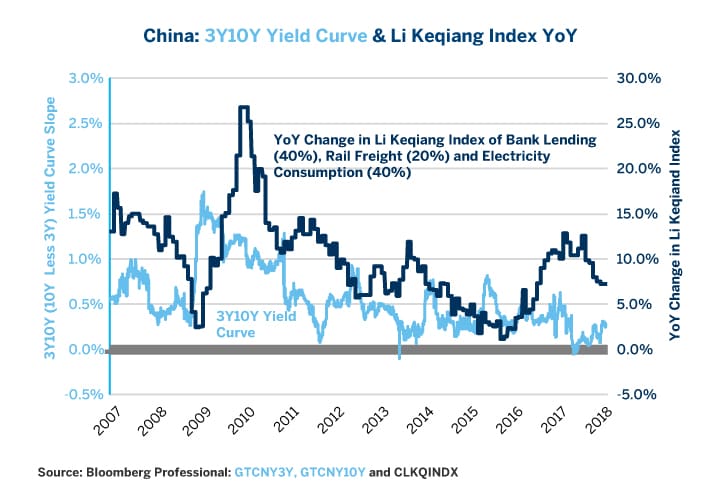

Before we delve into which index has done a better job of forecasting movements in commodities and commodity currencies in the past, let’s begin with which index responds more quickly and accurately to China’s own domestic interest rate market. As we have written in the past, China’s official GDP correlates highly with the slope of the 3Y-10Y bond yield curve (Figure 1). This is even more true of the Li Keqiang index, which responds to changes in the yield curve slope even more quickly (Figure 2).

Figure 1: China’s Official GDP Growth Rates Tend to Accelerate After Yield Curve Steepens.

{kind=link}

Figure 2: The Li Keqiang Index Follows Yield Curve Slope Even More Closely.

{kind=link}

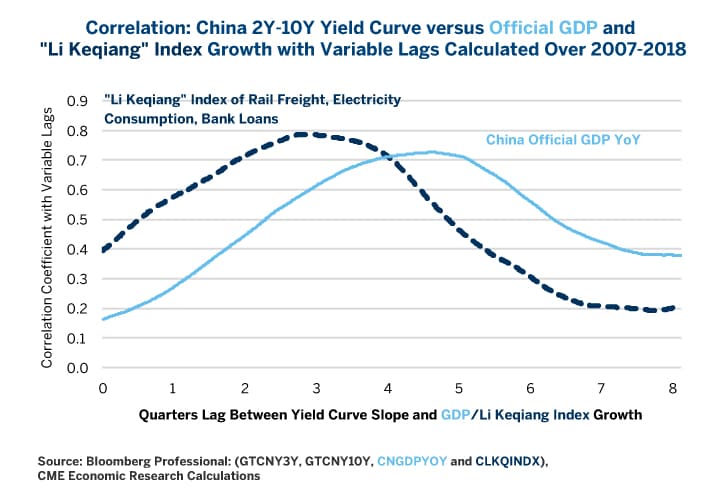

To demonstrate this relationship, we calculate the correlation coefficient of both the official GDP, which is released quarterly, and the monthly Li Keqiang index from 2007 to 2018, with variable lags from zero quarters (comparing the yield curve slope today to current economic growth) to as many as an eight quarters lag (comparing current GDP/Li Keqiang growth estimates to the slope of the yield curve two years, or eight quarters, ago).

Both official GDP and the Li Keqiang index show a tight correlation with the yield curve slope but Li Keqiang’s correlation to the yield curve peaks out both higher and quicker than the official GDP number. Official GDP correlates with the yield curve slope at about 0.7 – a very strong correlation -- four to five quarters in advance. Li Keqiang’s correlation to the slope of the yield curve reaches nearly 0.8 around three quarters in advance (Figure 3).

Figure 3: Li Keqiang Responds to Yield Curve Slopes Stronger and Quicker Than Official GDP.

{kind=link}

To some extent, this in an obvious result. 40% of the Li Keqiang index is annual growth in bank loans. When the People’s Bank of China (PBOC) cuts rates, it both steepens the yield curve and encourages banks to accelerate the extension of credit. When PBOC tightens policy, the opposite occurs. Obvious or not, the fact that China has a) enormous debt levels, and b) a rather flat yield curve, bodes poorly for both growth measures going forward. The flattening of the yield curve that started last spring may also explain why the Li Keqiang index has been on such a sharp slowing trajectory in recent months –something conspicuously absent from the official Q4 2017 Chinese GDP estimate. Slower growth by either measure, but especially the Li Keqiang index, may be sending warning signals to commodity markets. It may be the case that the 2011-2016 commodities bear market that hit as Chinese growth slowed, isn’t over. Rather, we might be in the eye of the storm that is about to unfold.

Industrial Metals

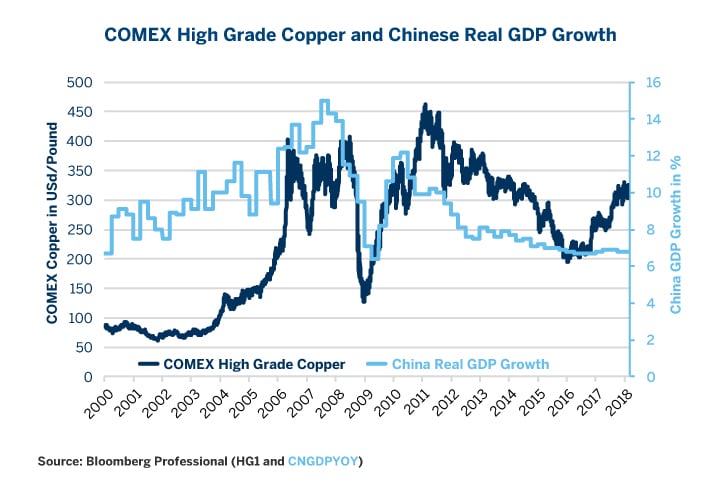

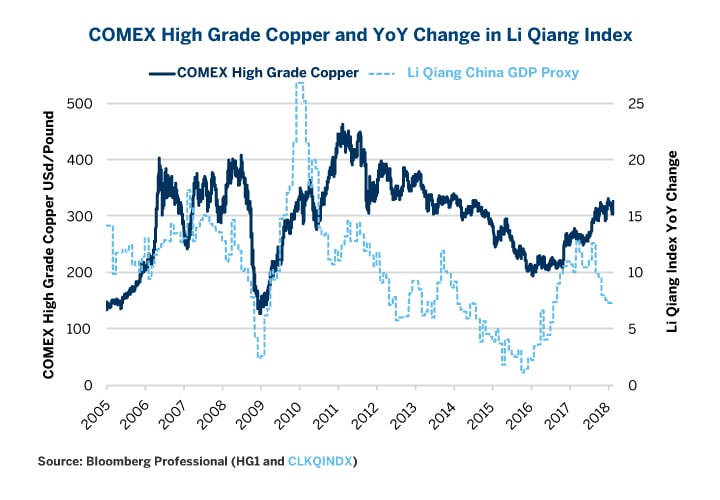

Chinese interest rates are not the only instrument to demonstrate a stronger correlation with the Li Keqiang index than with official GDP. The same can be said of industrial metals such as copper. What’s particularly curious about copper is that rather than lead Chinese GDP like the yield curve slope (by either the official or Li Keqiang measure), it lagged Chinese GDP rather substantially (Figures 4 and 5).

Figure 4: Official GDP Often Led Copper Prices.

{kind=link}

Figure 5: Li Keqiang Correlation with Copper Higher and Its Recent Decline Might be a Signal.

{kind=link}

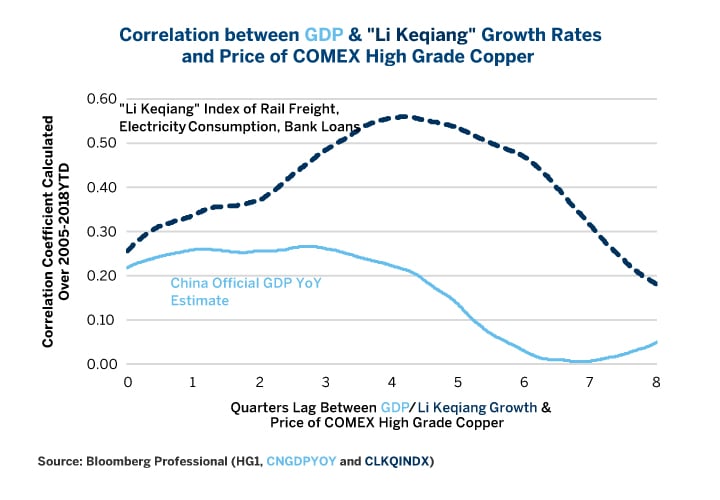

The most important point, however, is that copper prices demonstrate a much higher correlation to the Li Keqiang index (as much as +0.55, four quarters, or one year, later) than it does with China’s official GDP. The latter achieves a peak correlation of only around 0.25, with a lag of 1-3 quarters (Figure 6).

As such, if the past is any guide, – and past performance does not guarantee future results— the recent slowing in the Li Keqiang index from 12.6% growth to 7.3% growth might augur poorly for the price of copper going forward. Further, to the extent that China’s flat yield curve may be signaling a further slowing of activity in coming quarters, this could add further downward pressure to copper prices should the Chinese economy show evidence of further softening.

Figure 6: Li Keqiang Correlated Much More Highly with Future Copper Prices Than Official GDP.

{kind=link}

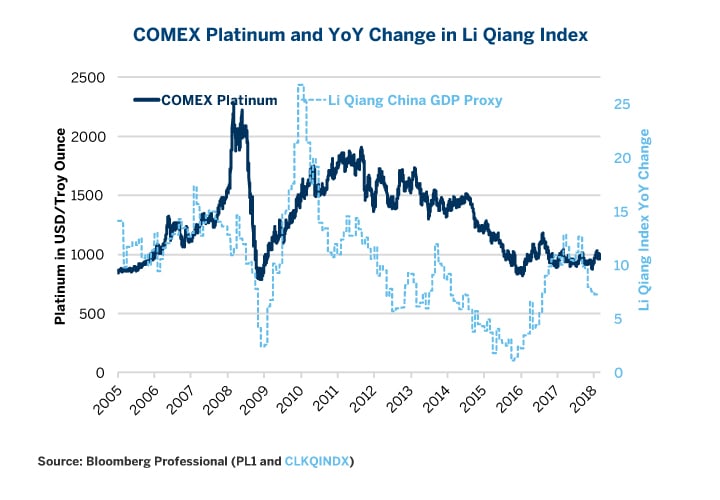

A similar relationship held true for platinum over the same 13-year period. Platinum is usually classified as a precious metal but this distinction has more to do with price than with use. The primary use of platinum is in the automotive industry and, from an economic perspective, the metal is more accurately described as a rare and expensive industrial metal. As with most industrial metals, China is the single largest consumer and its price depends on Chinese demand more than any other single factor. Given China’s appetite for automobiles and other industrial products, it should come as little surprise that platinum closely follows (but does not lead) both measures of China’s growth (Figures 7 and 8).

Figure 7: Chinese Official GDP Often Leads Platinum Prices.

{kind=link}

Figure 8: Li Keqiang Also Leads Platinum Prices.

{kind=link}

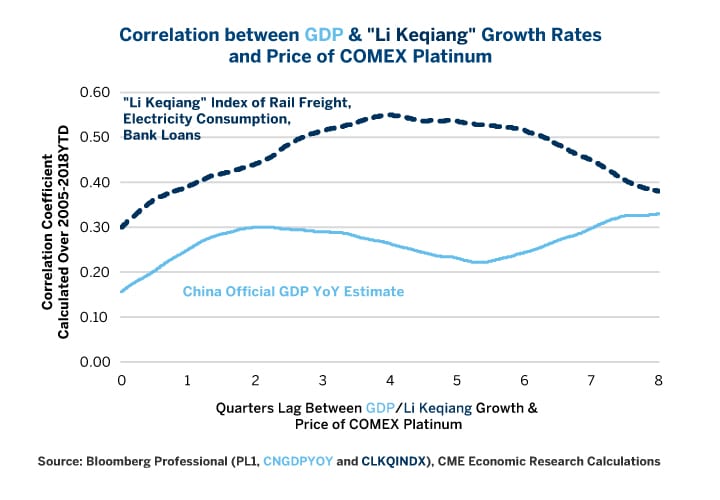

Platinum is much more highly correlated with the Li Keqiang measure of economic growth than it is with the official Chinese GDP (Figure 9). Given China’s flat yield curve and the recent decline in the Li Keqiang index, this might bode poorly for platinum prices in coming months as well.

Figure 9: Of the Two Measures, Li Keqiang did a Better Job of Indicating Future Platinum Prices.

{kind=link}

Energy Markets

Discussion of oil markets is often dominated by talk of supply, namely, the Organization of Petroleum Exporting Countries’ (OPEC) latest moves and the surging supply of oil from the U.S. As such, it is easy to overlook China’s key role as both a direct and indirect driver of demand.

Perhaps not surprisingly, Chinese GDP has a similar relationship to crude oil as it does with industrial metals. Although Chinese demand constitutes only about 7% of the world total, it has been a fast grower and much of the increase in global production has gone to China. By contrast, demand in Europe and North America has been relatively stagnant. Moreover, as China boomed, it lifted raw materials prices, helping to spur economic growth in commodity exporting countries from Africa to Latin America as well as among China’s neighbors in Asia.

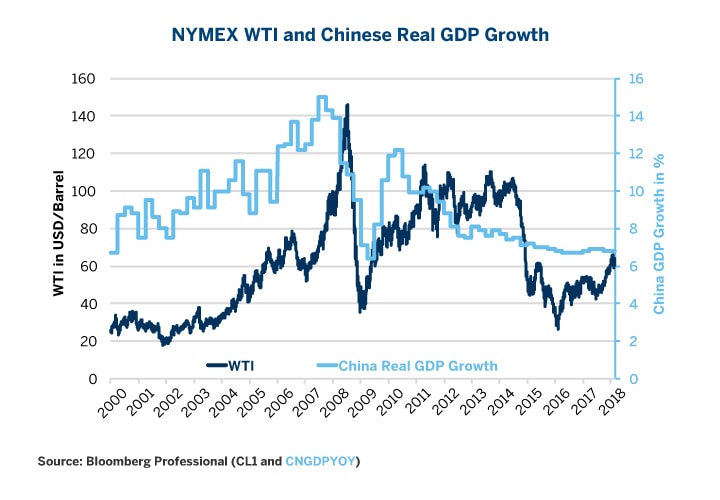

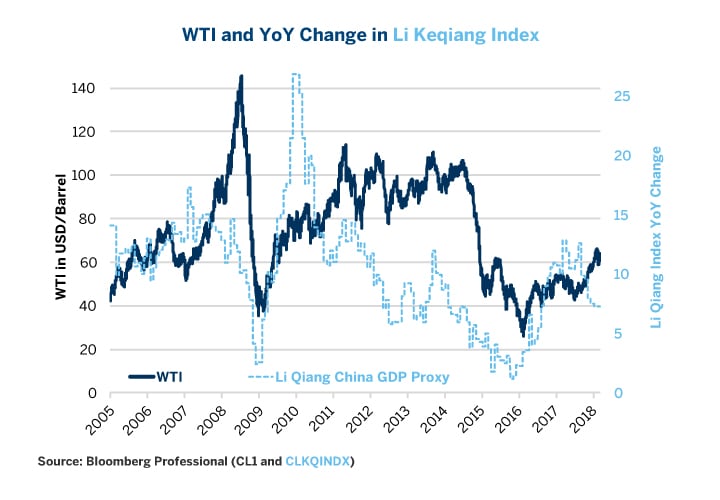

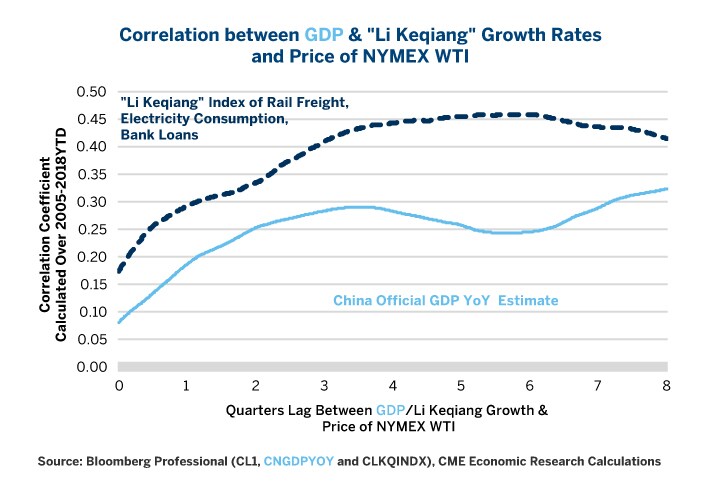

This in turn drove enormous increases in demand for crude oil. Not surprisingly, when China’s growth begins to slow, crude oil often comes under downward pressure about 3-8 quarters later. (Figures 10 and 11). For WTI crude oil, too, the Li Keqiang index dominates the official Chinese GDP (Figure 12).

Figure 10: Official GDP and WTI.

{kind=link}

Figure 11: Li Keqiang GDP Proxy and WTI.

{kind=link}

Figure 12: Li Keqiang Dominated Official GDP for WTI as Well.

{kind=link}

Currency

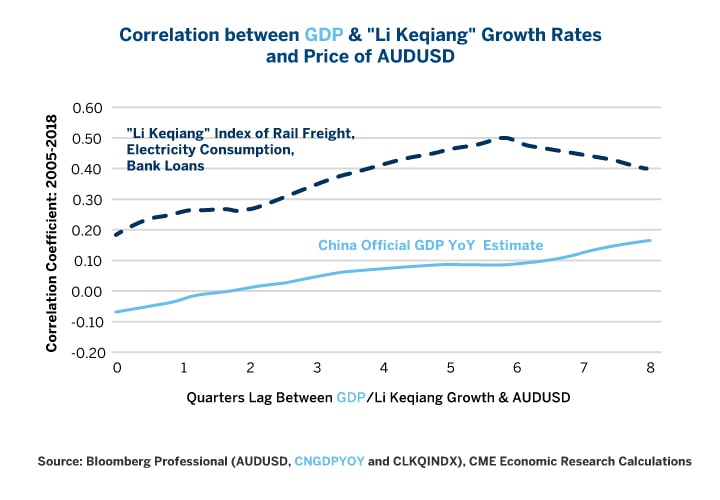

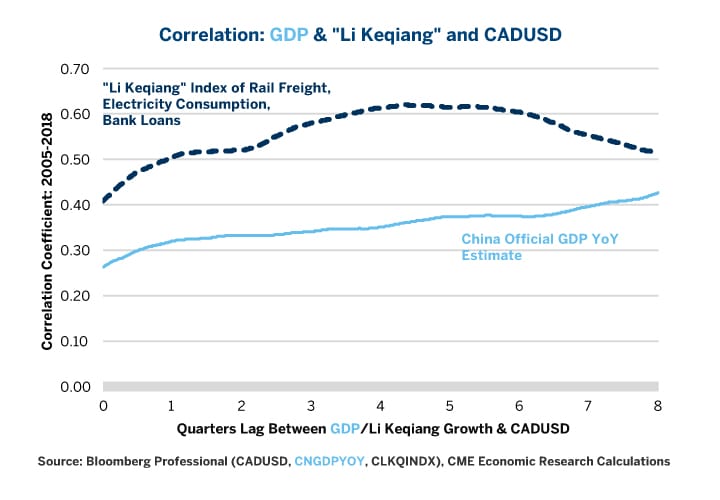

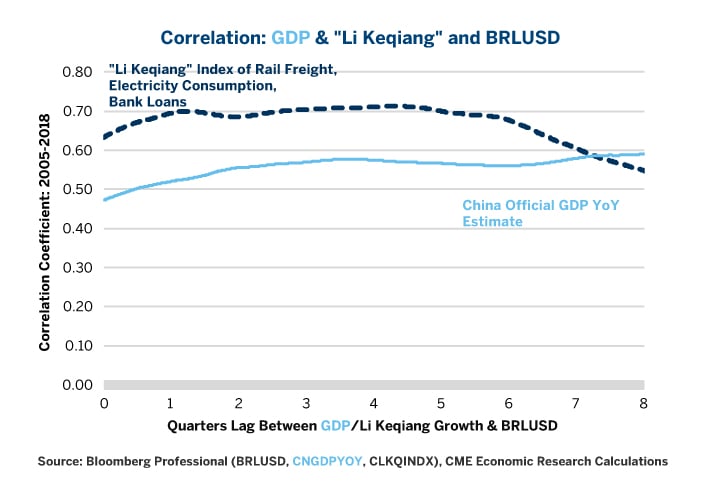

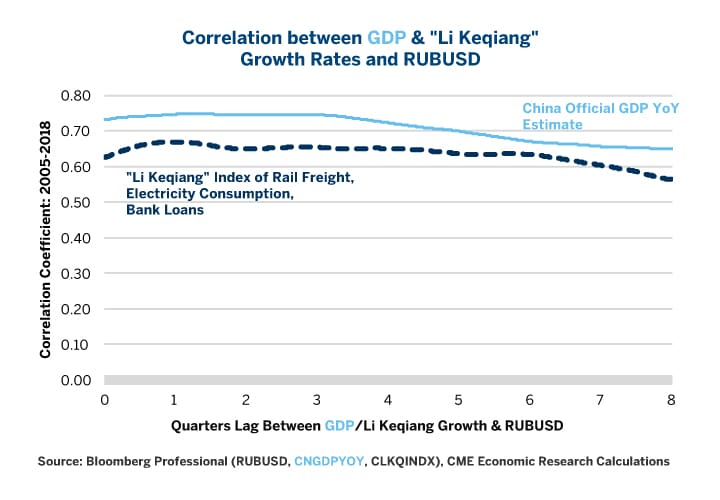

Given the strong impact of economic developments in China on the prices of industrial metals and crude oil, it is not surprising that Chinese growth also strongly impacts the value of currencies of numerous commodity exporting countries. This is true of those tied to oil production, such as the Canadian dollar (CAD) and Russian ruble (RUB). It also applies to currencies tied closely to currencies of metals exporting nations such as the Australian dollar (AUD) and Brazilian real (BRL). For these currencies, except RUB, the Li Keqiang index dominated China’s official GDP as a correlate of future value (Figures 13-16) from 2005 to early 2018. For RUB, however, both measures correlated extremely strongly, indicating the degree to which Russia has come to depend both directly and indirectly on the strength of Chinese demand growth for raw materials.

Figure 13: Li Keqiang Signaled Much of AUDUSD Value Over the Past 13 years.

{kind=link}

Figure 14: Li Keqiang Dominated the Picture for CADUSD as Well.

{kind=link}

Figure 15: Li Keqiang Played a Key Role in BRLUSD as Well.

{kind=link}

Figure 16: GDP had Edge over Li Keqiang in Strong Correlation with RUBUSD.

{kind=link}

If China’s growth continues to slow, it could put downward pressure not only on commodity prices but on the currency value of many resource exporting nations as listed above. This in turn could create renewed competitiveness problems for China if the renminbi (RMB) remains too closely tied to the U.S. dollar (USD). For the moment, a weak USD is great news for China, but if the combination of a weak USD and a tightening Fed causes the PBOC to raise interest rates, this could invert the Chinese yield curve and signal a deeper slowdown to come. Of course, if Chinese growth surprises on the upside, it would likely boost commodity currencies and support RMB as well.

When people say that the Li Keqiang index is dead, what they might mean is that it no longer does a good job of forecasting China’s GDP. This could be because China’s economy is becoming significantly more diversified with a more prominent service sector and reduced reliance on heavy industry. This may be so but, for investors in commodities and commodity currencies, it is the industrial sector that counts. As such, rail freight, credit growth and electricity use may be better proxies for the future value of these goods and currencies than China’s broader GDP measure.

That said, it may also be that commodity and currency markets respond to developments in China more quickly and with less of a lag time than was the case in the past. If the Li Keqiang index becomes less relevant in the future, it may be due to investors with access to alternative data – real time measures of electricity use and rail freight, for example— gain an advantage over those who wait for the official numbers to be published.

Above all, this research highlights China’s essential role as the dominant driver of marginal demand for a wide variety of commodities and hence the currencies connected to them. China’s economy is 5-7x bigger than any of the other BRIC (Brazil, Russia, India, China) economies and its demand will be difficult to replace should the country’s growth slows.

Bottom Line

- The Li Keqiang index is more relevant than official GDP for almost every commodity and currency that we tested.

- The Li Keqiang index showed a much sharper slowdown in 2015 than official GDP.

- And the index showed a much stronger rebound.

- The 2016-17 rebound, however, may be giving way to renewed weakness.

- A flat yield curve could be signaling a deeper slowdown to come.

- High debt levels (257% of GDP) and high debt service ratios (20%+ of GDP) could also weigh on China and generate a slowdown.

- A Chinese slowdown could weigh heavily on industrial metals and energy prices.

- Weaker commodity prices could also hurt commodity currencies.

- Upside surprises to Chinese growth could boost commodities and commodity currencies.

China Growth and Markets

An unofficial index of China's economy might be signaling that the country's growth could slow down, affecting markets for commodities such as crude oil, copper and platinum, and commodity currencies such as the Australian and Canadian dollars, along with the Brazilian real and ruble. Protect your investments with the suite of CME Group products.