Learn about Convexity

{kind=link}

Implied volatilities are not necessarily the same at every strike. The collection of these different volatility levels is known as the volatility curve. When the implied volatilities of put options are higher than the implied volatilities of call options – this is referred to as negative skew.

Conversely, when the implied volatilities of calls are higher than the implied volatilities of puts – this is referred to as positive skew.

But what if the out-of-the-money puts and out-of-the-money calls are more symmetrical, and have the same implied volatility levels? This is referred to as “the smile” and is said to have positive convexity.

Just as the skew provides market information concerning the expectation of volatile moves, so can convexity. When the curve is “smiley” or has large convexity, the market is indicating potential acceleration of implied volatility levels if the underlying futures price moves up or down.

If the curve flattens, the market is expecting less implied volatility change with a movement in the underlying. If the curve flattens to a straight line, this indicates that the Black-Scholes implied volatility levels are equal at every strike. This is zero convexity.

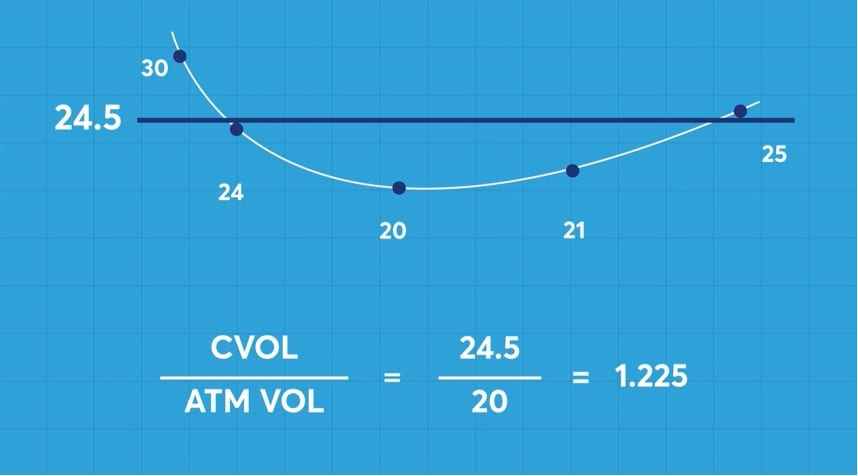

Historically, convexity is a comparison of at-the-money and out-of-the-money options – calculated either as a ratio or by subtraction. The convexity indicator is calculated by taking the ratio of the CVOL index to the at-the-money implied volatility.

https://www.cmegroup.com/content/dam/cmegroup/education/images/2021/learn-about-convexity-fig01.jpg

{kind=link}

If the volatility curve consisted of strikes with volatilities of 30, 24, 20, 21, and 25; assume the CVOL calculation is 24.5, and the at-the-money implied volatility is exactly 20. The CVOL convexity is calculated by dividing 24.5/20, which is 1.225

Calculating convexity as a ratio allows us to compare convexity levels across different products.

In this example, the difference of 4.5 volatility points produces 22.5 percent in one product versus 5% in the other.

This means the options on product A are estimating more acceleration of implied volatility levels given movements of the underlying futures than for product B.

CVOL convexity is part of the complete CVOL offering, available on all products with a CVOL index. For more information on CVOL, click here.