- 6 Aug 2024

- By CME Group

- Topics: Interest Rates

In their first full month, Credit futures on Bloomberg Indices have seen strong ADV growth and a deepening market. In just over 30 trading days:

- 14,400 contracts were traded

- Quotes and daily activity observed across the suite

- Tight spreads as low as .03% of the Index Price

- Strong market maker participation both electronically and via block trading

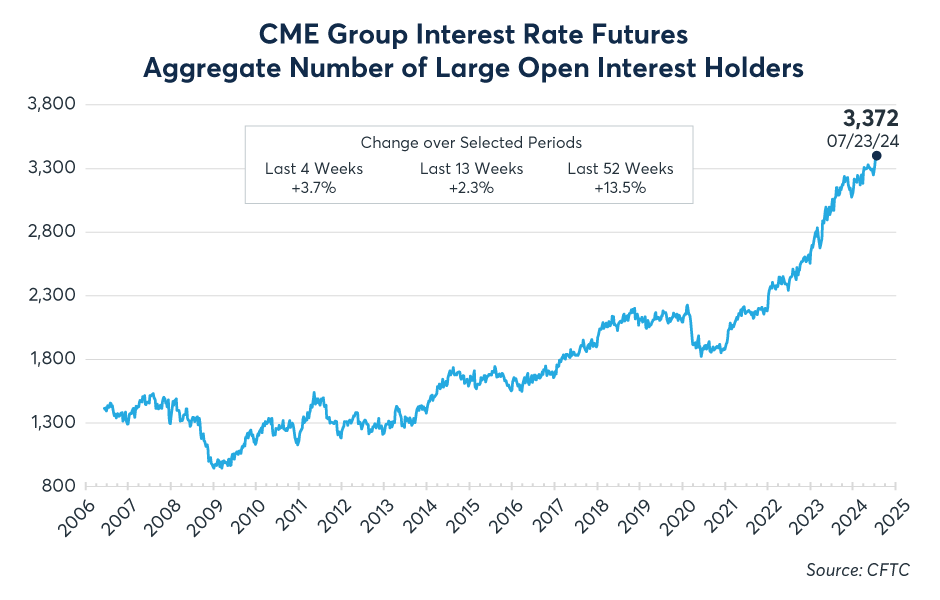

The number of Large Open Interest Holders (LOIH) in Interest Rate futures continues to climb, reaching a record of 3,372 in July, according to the CFTC.

This proxy for market participation among firms holding significant positions is up 10% YTD, with new highs observed in SOFR, Fed Funds, €STR, 2-Yr, 5-Yr, Ultra 10-Yr, T-Bond and Ultra T-Bond futures.

Source: CFTC and CME Group

Looking for new ways to manage SOFR risks? Monthly SOFR options allow for additional short-term precision via one- or two-month options on any One-Year or Two-Year quarterly futures underlying not covered by our current offering.

Since launch on June 17, these short-dated options have traded over 47K contracts (23K in current OI) on Dec 24, Mar 25 and Dec 25 underlying futures. This includes trades in both U.S. and non-U.S. hours.

Participants are rediscovering the risk management capabilities of T-Bill futures, due in part to recent volatility both in short-end rates as well as the SOFR-Bill basis.

3M SOFR vs. T-Bill futures spread

Source: CME Group

These contracts, based on 13-week T-Bill auction yields, have seen ADV nearly quadruple MoM and just hit a new high of 8,153 in OI on July 29. Refresh your knowledge about this market with our guide.

Our recently launched "give-get" service increases pricing visibility for market participants, providing a basis curve that is updated weekly.

Contact a member of the Interest Rates team to learn more about participating in this service.

The Two-Year vs. Ten-Year Treasury recently celebrated its two-year inversion anniversary, however, recent activity could normalize the curve. Jim Iuorio explores trades around this spread and key factors to monitor in his latest video.

Our latest Index innovation utilizes 4:00pm London Markers in nearby quarterly-IMM contracts in:

Three-Month SOFR futures

Three-Month €STR futures

EUR/USD FX futures

These are used to calculate the implied forward starting Three-Month cross currency basis EUR/USD.

Cash is king for REITs, underscoring the importance of capital-efficient hedging. That's why some top REITs are making the switch from bilateral swaps to Eris Swap futures.

Read our latest report to learn more about this trend, which by our estimates, could save top REITs $1.5B in posted margin.

In less than four months, the primary conversion of 28-Day TIIE to F-TIIE for CME Group cleared MXN swaps will take place. Prepare for this fast-approaching event with our resources page, including our new conversion guide complete with a timeline of key events.

Data as of August 01, 2024, unless otherwise specified.

* Pending regulatory approval

View an archive of the Rates Recap online at cmegroup.com/ratesrecap.

© 2024 CME Group Inc. All rights reserved.