- 9 May 2024

- By CME Group

- Topics: Interest Rates

Credit futures are coming June 17.* Prepare with our webinar which features experts from both CME Group and Bloomberg.

Watch now to learn about key index details, benefits of credit futures and more.

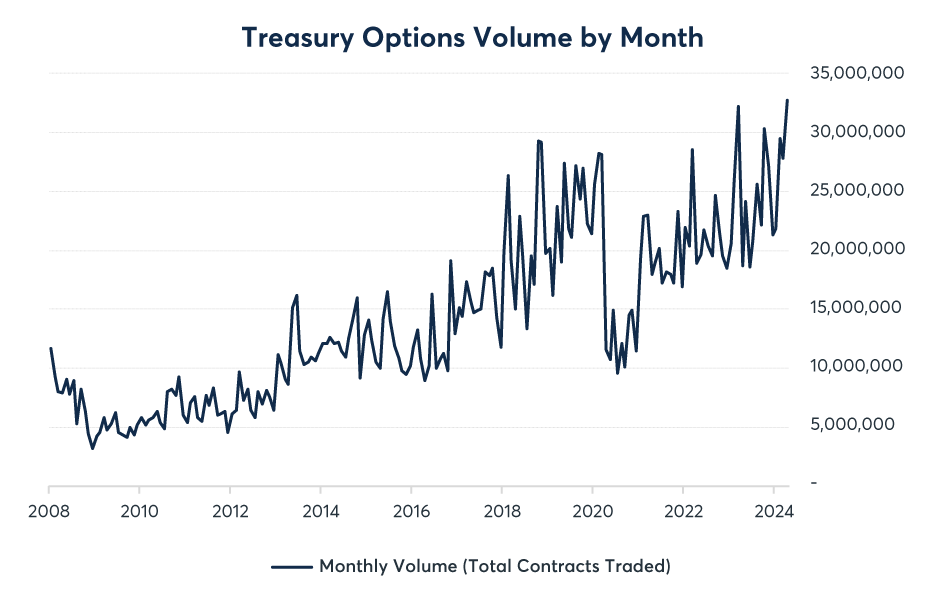

More Treasury options traded in April than any month in history, as a slew of market-moving events sparked renewed volatility and record trading across the weekly expiries:

- Monday weeklies: Highest monthly ADV (65K), including a record 218K contracts traded on April 12 ahead of rising weekend risks

- Wednesday weeklies: Fifth-highest monthly ADV (123K), including 305K contracts traded on April 10 following a hot CPI print

- Friday weeklies: Fourth-highest monthly ADV (354K), including 788K contracts traded on April 5 following a strong nonfarm payroll report

Important milestones are rapidly approaching for a number of benchmark transition and cessation events. Please reach out to the team if you have any questions or concerns, and make sure to note the dates below.

- CAD CDOR conversion date: May 17

- USD BSBY conversion proposal feedback deadline: May 17

- MXN 28D TIIE conversion date: November 22

In their first full month, Micro Treasury futures saw over 200,000 contracts of volume, an excellent start for the nascent contracts. Thanks in part to increased volatility, ADV closed in on 10,000 for the month with OI approaching 2,000 as well.

Yield futures have also seen an uptick in recent weeks, with ADV increasing 66% MoM to just over 9,000 contracts, giving traders cost-effective ways to express their view on the Treasury market in either price or yield.

Source: CME Group

For more insights, read our latest paper on spread trading.

The popular FedWatch Tool now has a new view of rate hike and cut probabilities implied by Fed Funds futures prices.

In addition to the familiar "conditional" view of the path of rate activity, the Tool now has an "aggregated" option which allows users to see the total amount of rate changes priced-in between the current date and the selected FOMC meeting in the future.

Recent FASB changes and the advent of Eris SOFR Swap futures have made hedge accounting more accessible than ever. Learn about the key developments in this market and why now might be the time to give this hedging technique a closer look.

Source: CME Group

Over 1.25M CME Group €STR contracts have traded so far in 2024 and recent changes have only helped to improve liquidity. Highlights include:

- Bid/ask spreads tightened on average 13% since reducing the MPI to ¼ bp

- New one-day high of 56,728 contracts traded (April 9)

Additional enhancements are coming, including the launch of options on €STR futures on May 20.*

A key factor in swap agreements is that the payouts are non-linear: they exhibit convexity. Grasping how this works is crucial for knowing how payout differences between swap and futures contracts will influence hedging needs and strategies.

- TBA futures saw OI breach 10K contracts ($1B notional) for the first time ever in April, alongside record monthly volume of 19K contracts ($1.9B notional).

- 3-Year Note futures had OI double since early March, surpassing 21K contracts ($4.2B notional) on May 2.

- LatAm IRS set a new record, surpassing $70B/day in activity.

Data as of May 1, 2024

*pending regulatory review

View an archive of the Rates Recap online at cmegroup.com/ratesrecap.

© 2024 CME Group Inc. All rights reserved.