- 9 Jan 2024

- By CME Group

- Topics: Interest Rates

Driven by deep and consistent liquidity, efficiency and meeting the market's risk management needs, Rates trading at CME Group hit new records in 2023, including:

- U.S. Treasury futures – ADV of 5.6M was up 16% over the previous high.

- U.S. Treasury futures – OI peaked 25% above prior peak (reaching 21M contracts).

- SOFR futures and options (F&O) – ADV (reaching 5.1M) was more than double that of 2022.

- SOFR F&O – ADV beat the best year in the four-decade history of Eurodollars.

- SOFR F&O – OI reached a new peak of 60M contracts.

- Fed Funds – Record ADV fueled by Fed. uncertainty (reaching ~442,000 contracts)

- 10-Year Yield futures – Record ADV and OI in 2023 was driven by retail activity.

- Swaps – Portfolio margining of cleared swaps vs. listed futures and options set new high-water mark with an average daily savings of $8B.

- Options – Record ADV of just over 2.9 million contracts, up 27% YoY as precise risk management became even more vital for participants.

- U.S. Treasury options – Record ADV, up 13% YoY driven by deep liquidity and new, precise ways to hedge risks.

Source: CME Group

TBA and €STR futures had their debuts in late 2022 and made great progress in building towards critical mass last year. Both have become go-to choices for participants seeking to manage risks as volume levels continue to rise.

TBAs:

- Total contracts traded exceeds 100K

- OI grew 70% in December to close the year at a record 4,300 contracts

- ADV exceeded 750 contracts in both November and December

€STR:

- Over 1.6 million contracts traded on the year

- OI reached a record of 38,168 on December 14, up from ~1,000 at the start of 2023

- Q4 ADV exceeded 12.7K

Two key Interest Rate products made their debut in 2023 to offer additional ways to manage risk, including:

T-Bill futures – With an increased focus on T-bills to fund Treasury obligations, 13-Week U.S. Treasury Bill futures are now here to meet clients' need for a direct and effective hedging instrument at the short end of the curve.

Monday weekly Treasury options – New Monday Treasury options provide participants with more expirations for precise risk management. In just two months of trading, ADV has reached 18K.

The analytical landscape on CMEGroup.com expanded again in 2023 with the launch of several new tools and significant improvements to others. Check out the key highlights to hone your strategies this year.

- CME Cross-Currency Basis Watch – Monitor the magnitude of the euro/dollar basis to see what the market is pricing in.

- CME SOFRWatch – Plot the impact of potential Fed action to see how it would influence SOFR fixings.

- CurveWatch upgrade – This enhancement to the Treasury Analytics suite allows participants to unlock trading opportunities with Yield futures and discover yield curve insights.

By Erik Norland

In 2023, the world's central banks completed the largest tightening cycle since 1981. Typically, it takes one to two years for the impact of monetary policy changes to be fully reflected in the economy. As such, the consequences of the 2022-2023 rate hike cycle could begin to impact global growth this year.

Bond yields are reflecting this concern. Following the Fed's 525 basis points (bps) of rate hikes, the U.S. yield curve has become the most steeply inverted in 42 years. Previous yield curve inversions in 1989, 1999-2000, and 2006-2007 were followed by economic downturns that typically began one to two years later. Higher short-term rates are driving up financing costs for households, businesses, and governments alike.

If the U.S. were to experience a downturn in 2024, it would likely look much different than that after the global financial crisis (GFC). That downturn was concentrated in residential real estate and large financial institutions. This time around, housing vacancy rates are low for both owner-occupied and rental real estate. Instead, the U.S. economy could experience a downturn focused on commercial real estate and smaller financial institutions with exposure to the sector.

Inflation in the U.S. has declined sharply. Outside of owners' equivalent rent, prices are rising at just 2% year over year. Lower U.S. inflation and falling inflation elsewhere should allow central banks to cut interest rates, especially if economic weakness materializes over the course of 2024. Finally, China's economy is experiencing near-zero inflation as the Chinese economy reels from a decline in the real estate sector.

Both the €STR and SOFR curves are pricing in rate cuts of roughly 150bps by mid-2025. However, there are some key differences between European and American economic trajectories as of late.

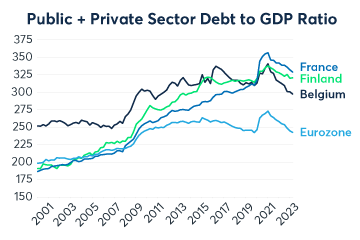

The U.S. has seen sharply declining inflation relative to Europe but the real difference may be in debt-to-GDP ratios. This is particularly the case in certain euro zone nations such as Belgium, Finland and France which have debt-to-GDP ratios in excess of 290%.

Learn how this could impact the rate cut discussion in 2024 and beyond:

Source: CME Group

Data as of January 09, 2024, unless otherwise specified

View an archive of the Rates Recap online at cmegroup.com/ratesrecap.

© 2024 CME Group Inc. All rights reserved.