{kind=link}

Understanding Crack Spreads

Refining 101 - Understanding Crack Spreads

Relationships between Crude Oil, Heating Oil and Gasoline

Even though the US economy is still a gasoline driven economy, the HO crack spread has become more and more interesting from a trading perspective as the US is now a major exporter of distillate fuels - HO and diesel. Like the Brent/WTI spread, the HO crack spread is very liquid as well as volatile and trendy - all positives for the trading community at all levels. In addition this spread is also used by the refiners as a hedge during periods when refinery margins are expected to narrow.

It is also a spread that can be traded on the NYMEX division of CME as part of the regulated futures arena. Volumetric activity for the spread is continuing to grow, as is liquidity.

This is a very fundamentally driven spread (as are most spreads) with the same fundamentals driving the direction of the spread for many years. The main fundamental drivers of the spread are:

- Winter month demand for heating oil in the US and in Europe.

- Inventory levels of heating oil and diesel.

- Throughout the year the growing demand for diesel fuel in many regions of the world that are now exports targets for US refiners.

- The state of the gasoline market in the US.

- Crude oil balances and geopolitics and the impact it has on refiner’s crude oil costs.

- Other weather events like hurricanes.

- Scheduled and unscheduled refinery interruptions.

First let’s quickly discuss what the HO crack spread is and is not. It is not an absolute measure of refinery margins in the US as the HO portion is a wholesale price in New York Harbor as traded on the NYMEX division of CME while the WTI crude oil is price is a spot prices based in Cushing, Oklahoma. It does not include any refinery costs or location adjustments. It is a gross representation of the direction of the distillate component of refinery margins against WTI crude oil - one of the many, many crude oils that the US refiners actually process in their refineries. Simply put, when the HO crack spread is trending higher it means refiners are making more money processing crude oil to make distillate fuel and when the spread is trending lower they are making less money.

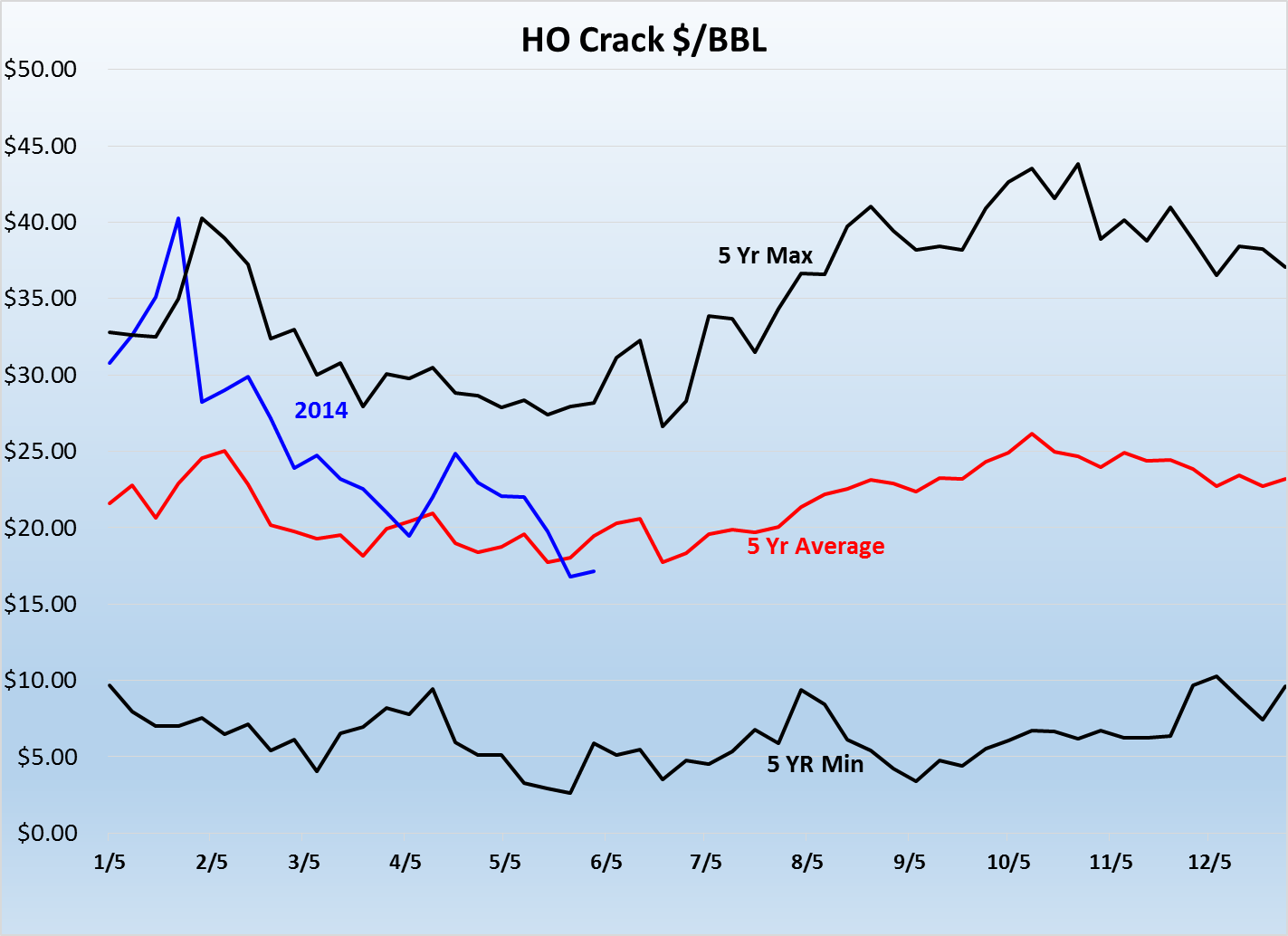

With this in mind, the following chart shows the NYMEX HO crack spread plotted on a seasonal chart along with the latest five year average and the highs and lows that occurred when the calculations for the five year period performed.

{kind=link}

Source: NYMEX ULSD Historical Data

This is what is categorized as an inter-market spread with reduced trading margins compared to trading the flat price for either of these commodities. This weekly chart clearly shows a modest level of volatility as well as the trending nature of this spread. It also shows the seasonality of the spread with the high points generally hit during the so called official winter heating season (October through March) with the lows generally occurring during the summer months or during the gasoline driving season.

Certainly during the heating season the direction of the spread is going to be primarily driven by the winter weather and thus heating demand for heating fuels in both the US and Europe. During the heating season oil will flow between these two regions depending on the weather and demand for heating oil in each of the respective areas.

In the US the majority of the heating oil consumed for space heating is in the Northeast with minimal quantities consumed in other regions of the US. Thus when evaluating the spread during the winter months, the weather along the northeast coast is important. Also keep in mind New York, which represents almost 1/3 of the Northeast heating oil market, now requires ultra-low sulfur fuel (15 PPM) as reported by the U.S. Energy Information.

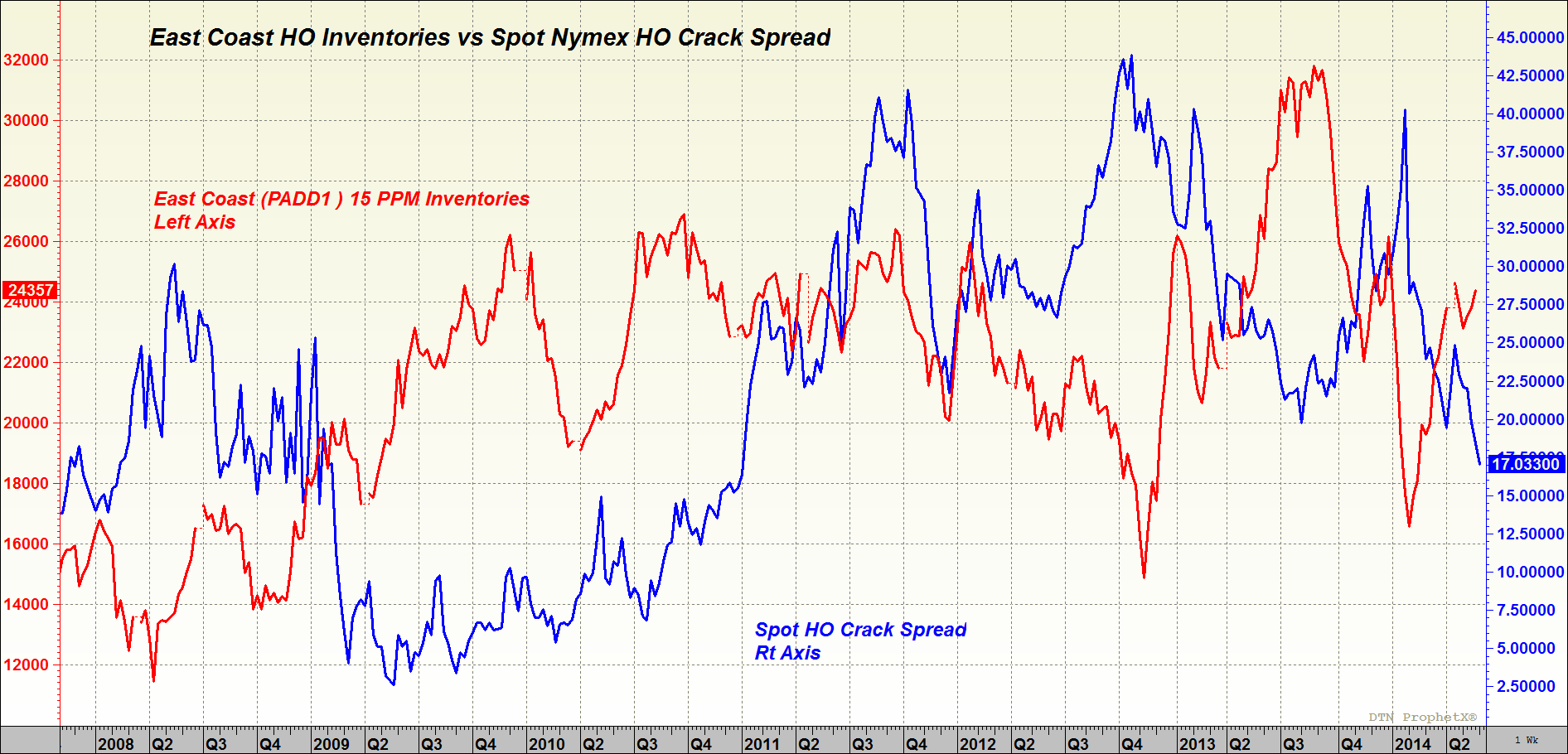

The following chart compares the spot NYMEXHO Crack spread with the weekly HO inventories along the East Coast of the US - the primary HO market in the US.

{kind=link}

Source: Chart provided by DTN

As shown on the chart, there is a relatively strong inverse correlation between HO inventory levels along the east coast with the performance of the HO crack spread. As HO inventories rise the crack narrows and when stocks decline the crack has a tendency to widen. As expected the strongest correlations tend to be during the so called official winter heating season.

In addition the temperatures forecasts for Europe are also very important. These forecasts do impact the short term direction of the spread and add to the volatility of the crack spread in the short to medium term.

Another area that has an impact on the HO crack spread is the supply and demand status of the gasoline market. Refiners have a lot of flexibility to maximize the production of gasoline at the expense of distillate fuel and vice versa. When gasoline demand is strong and/or supply is tight refiners will run in a maximum gasoline mode which will reduce the amount of distillate fuel produced. This could result in distillate fuel inventories declining and thus having a positive or upside impact on the HO crack spread.

In addition during periods of tightness in the crude oil markets caused by rising demand and/or supply issues due to natural events like hurricanes or geopolitical events like seen for many years in the Middle East and in North Africa the price of crude oil (the other half of the spread) could surge higher and have a negative impact on the HO crack spread even during periods when the relationships discussed above comparing inventories and the spread support a widening of the spread.

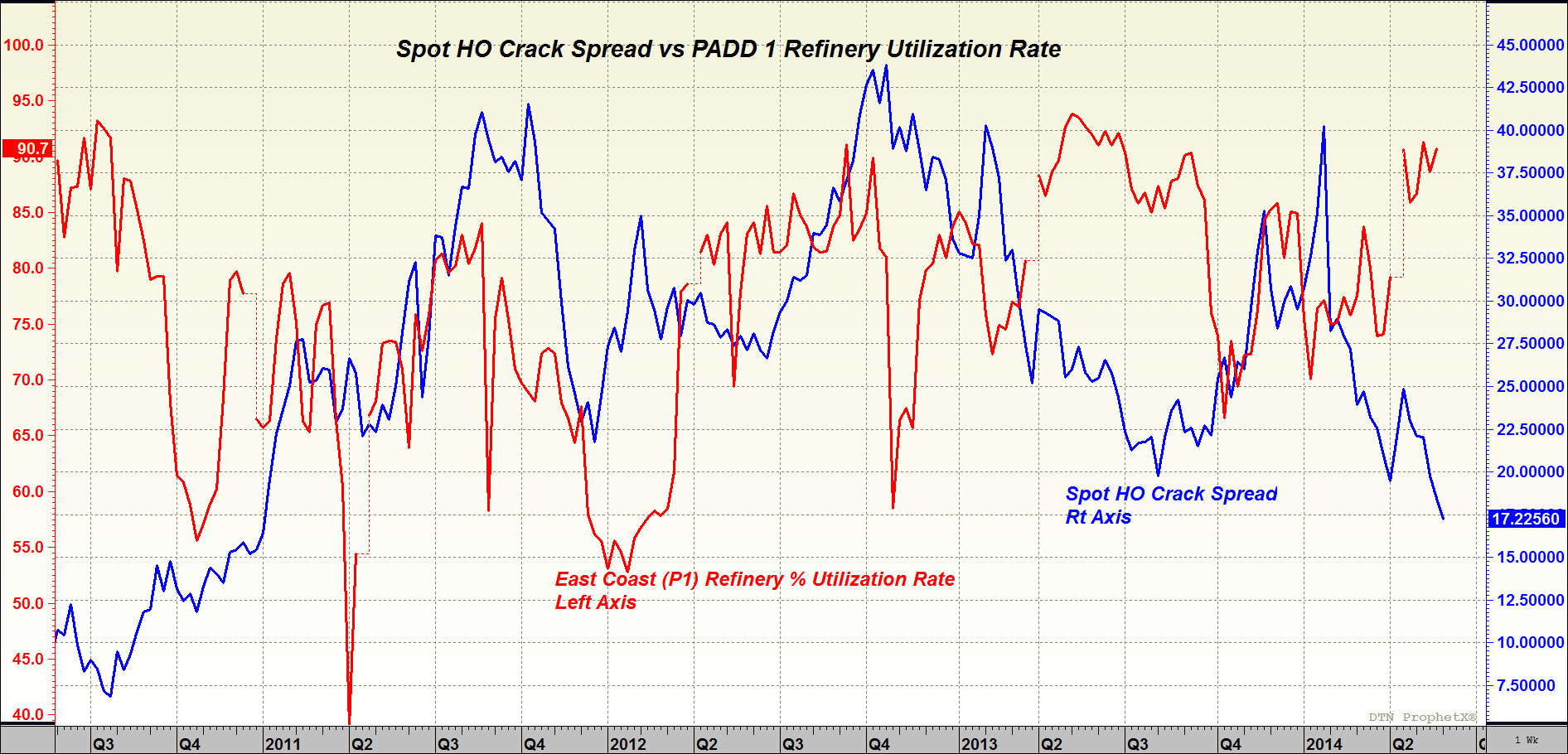

Finally, scheduled and unscheduled refinery events can impact the spread in either direction. When refineries are shut down for whatever reason it has an impact on production of distillate fuel (as well as all refined products) and often times result in a widening of the HO crack spread. On the other hand, when refinery runs are at high levels, more refined product is produced which could ultimately result in a narrowing of the crack spreads.

The following chart of the refinery run rates along the US East Coast (main heating oil market) versus the HO Crack spread demonstrate this relationship.

{kind=link}

Source: Chart provided by DTN

The chart shows an inverse relationship between refinery run rates and the crack spread. Although this is not a perfect correlation it holds most of the time. When the refinery runs rates are increasing it generally has a negative impact on the HO crack spread and vice versa.

The above are the main price drivers of the spread.