{kind=link}

Reconciling FX Spot Futures Price

Reconciling FX Spot Futures Prices

Traders are sometimes confused when comparing spot currency or FX exchange rates with FX futures prices. There are two sources of divergence between the quoted prices of spot and futures – (1) the quote convention; and (2) cost of carry. This article explains these differences in order reconcile the apparent price divergence.

Quote Convention

A spot FX transaction represents the exchange of one currency for another currency. E.g., one may buy Euros (“EUR”), making payment with U.S. dollars (“USD”). Or, buy Japanese yen (“JPY”), making payment in U.S. dollars. Likewise, one may trade buy a futures contract that call for the delivery of Euros vs. payment in U.S. dollars. Or delivery of Japanese yen vs. payment in U.S. dollars.

But FX transactions may be quoted in either “American terms” or “European terms.”

E.g., it cost $1.6756 USD to buy 1 British pound (“GBP”) as of May 30, 2014 in the spot markets - or $1.1167 USD to buy 1 Swiss franc (“CHF”) – or $0.0778 USD to buy 1 Mexican peso (“MXN”).

| CME Quotes | American Terms | European Terms |

|---|---|---|

| American vs. European Term Quotes (As of May 30, 2014) |

||

| USD vs. EUR | 1.3632 | 0.7336 |

| USD vs. JPY | 101.78 | 0.00928 |

| USD vs. GBP | 1.6756 | 0.5968 |

| USD vs. CHF | 1.1167 | 0.8955 |

| USD vs. MXN | 0.0778 | 12.8576 |

Quotation in European terms means that you are quoting tjhe amount of the "other currency" required to buy 1 U.S. dollar.

E.g., it cost 0.5968 British pounds to buy 1 U.S. dollar – or 0.8955 Swiss francs to buy 1 U.S. dollar – or 12.8576 Mexican pesos to buy 1 U.S. dollar.

Typically you will see spot currencies quoted in European terms – in the “other currency” per 1 U.S. dollar. But there are some exceptions to this rule including the EUR, the GBP and other British Commonwealth currencies such as the Australian dollar (“AUD”) and New Zealand dollar (“NZD”) which are quoted in American terms.

But CME FX futures are typically quoted in American terms. This practice facilitates ready calculation of profits and losses in U.S. dollars – a convenience for U.S. based customers. 1

Thus, FX spot and FX futures quotes - apart from the Euro and British Commonwealth currencies - may appear to be different. But it is easy to reconcile American and European quotes – one is simply the reciprocal of the other. The American terms quote is the reciprocal of the European terms.

{kind=link}

Or the European terms quote is the reciprocal of the American terms quote.

{kind=link}

E.g., you may see a spot quote for the Swiss franc vs. U.S. dollar as 0.8955 in European terms. This translates into 1.1167 in American terms as used in CME futures markets.

{kind=link}

Cost of Carry

Unlike spot transactions that call for (near) immediate delivery, FX futures contracts generally require delivery on a specified future delivery date such as the 3rd Wednesday of the contract months of March, June, September or December. 2 But the value of an item delivered today (on a spot basis) may be different than the value of an item delivered in the future (on a future or forward basis).

The difference between spot and futures prices is said to be driven by “cost of carry.” And cost of carry is essentially a function of short-term interest rates prevailing in the two countries whose currencies are being exchanged.

Think of it this way – if you buy a foreign currency with U.S. dollars, you get the opportunity to invest that currency at short-term rates prevailing in that country. But by paying for that currency in U.S. dollars, you forego the opportunity to invest that USD at prevailing U.S. short-term rates.

The futures price should reflect the spot price of the currency adjusted upward by the implicit cost of financing the purchase of the foreign currency with USD – but further adjusted downward by the opportunity to earn interest by investing the foreign currency at foreign interest rates.

Futures Price = Spot Price + U.S. Interest - Foreign Interest

These “cost of carry” considerations, i.e., the cost of buying and holding the foreign currency, are reflected in the difference (or “basis”) between the futures price and spot prices.

{kind=link}

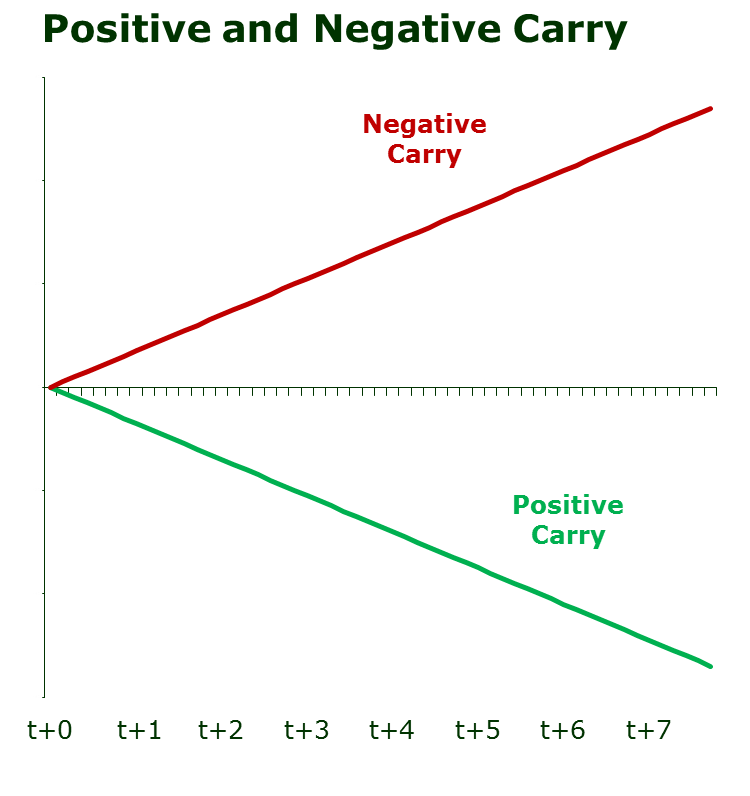

Where foreign rates are less than U.S. rates, futures prices run to higher and higher levels in successively deferred contract months in the future. This is a condition known as “negative carry” in the futures markets. Carry is “negative” because it costs more to finance the purchase of the foreign currency by paying in USD than one may earn by investing the foreign currency at foreign interest rates.

Where foreign rates are greater than U.S. rates, futures prices run to lower and lower levels in successively deferred contract months. This is “positive carry” because one may earn more by investing at the foreign rate than the implicit cost of financing reflected in U.S. rates.

| Item | Price |

|---|---|

| Euro vs. U.S. Dollar Spot & Futures Prices (As of May 30, 2014) |

|

| Spot Exchange Rate | 1.3632 |

| June 2014 | 1.3634 |

| September 2014 | 1.3635 |

| December 2014 | 1.3637 |

| March 2015 | 1.3642 |

The relationship between U.S. and foreign interest rates fluctuates. But as of this writing, Euro interest rates were a little less than U.S. rates. Thus, EUR/USD futures priced at higher and higher levels in successively deferred contract months, i.e., negative carry.

| Item | Price |

|---|---|

| Mexican Peso vs. U.S. Dollar Spot & Futures Prices (As of May 30, 2014) |

|

| Spot Exchange Rate | 0.07780 |

| June 2014 | 0.07767 |

| September 2014 | 0.07712 |

| December 2014 | 0.07657 |

| March 2015 | 0.07600 |

But Mexican short-term rates exceeded U.S. rates. Thus, MXN/USD futures priced at lower and lower levels into the future, i.e., positive carry.

As the relative level of U.S. and foreign interest rates fluctuate, these relationships are altered. It was only a couple years ago that European rates exceeded U.S. rates and the EUR/USD futures contract exhibited positive carry. But even a relatively small change in the difference between foreign and U.S. rates can affect the level of the basis.

Further, one finds that the basis (futures – spot prices) will generally tend to “converge” or approach zero as time moves forward and delivery approaches. At some point, spot and futures prices will fully converge when futures delivery is imminent and to the extent that buying or selling futures becomes tantamount to buy or selling spot currency.

- Some CME Group currency futures are quoted in European terms. For example, we list a South African rand (“ZAR”) contract quoted in rand per USD. Further, many currencies listed on the CME Europe platform, launched in May 2014, are quoted in European terms as well. But most of our most popularly traded FX futures are quoted in American terms.

- Actually, most commercial scale FX transactions in the “interbank” markets call for delivery two days after the transaction is consummated – on a “t+2” basis.