- 10 Jul 2017

- By CME Group

Futures contracts are legally binding agreements to buy or sell a particular commodity or financial instrument at a later date. This commodity may be bushels of wheat or corn, or U.S. Treasury bonds. Buyers with long contracts are obligated to buy, and sellers with short contracts are obligated to sell, a specified amount of this commodity or instrument if they hold open futures positions on the delivery date.

Options on futures are contracts that represent the right, not the obligation, to either buy (go long) or sell (go short) a particular underlying futures contract at a specified price on or before a specified date, the expiration date.

Note the difference, on the futures delivery date a physical commodity (e.g. wheat or corn) or financial instrument will change hands. On an option’s expiration date it is a futures contract that may change hands.

There are two types of option contracts, calls and puts.

Calls and Puts: Rights for Buyers

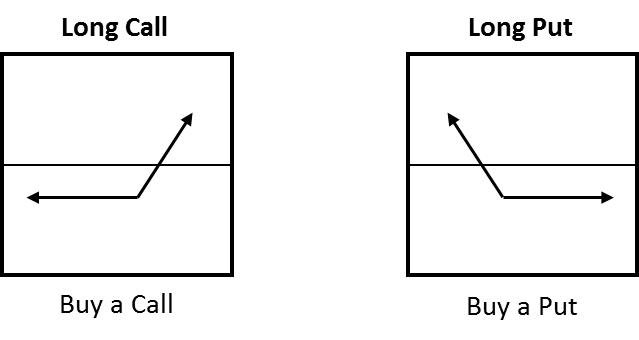

Call and/or put buyers are long option contracts, and hold (or own) these long positions in a brokerage account. Buyers with long options are sometimes referred to as “holders” or “owners.”

- A call option conveys to its buyer the right to buy (go long) a particular underlying futures contract, at a stated price, on or before a specified date in the future.

- A put option conveys to its buyer the right to sell (go short) a particular underlying futures contract, at a stated price, on or before a specified date in the future.

Only Option Buyers Exercise

When or if option holders decide to actually buy (go long) the underlying futures contract, in the case of a call option, or sell (go short) the underlying futures, in the case of a put option, the right to do so must be exercised. This requires instructing their brokerage firm of their intention to exercise their long option contracts. This decision is totally up to the option holder.

Calls and Puts: Obligations for Sellers

From whom do option buyers purchase these contracts and their inherent rights? It is not from a corporation or an exchange. Instead it is from option “sellers” who are selling contracts not currently owned. In a sense option sellers are creating, or “writing,” option contracts. By doing so they are taking short positions that convey a potential obligation to take the opposite position of an option buyer.

- A call option conveys to its seller the obligation to sell (go short) a particular underlying futures contract, at a stated price, on or before a specified date in the future if called upon to do so.

- A put option conveys to its seller the obligation to buy (go long) a particular underlying futures contract, at a stated price, on or before a specified date in the future if called upon to do so.

Only Option Sellers Are Assigned

When an option holder decides to exercise a long call or put, an option seller is assigned the obligation actually sell (go short) the underlying futures contract, in the case of a short call option, or buy (go long) the underlying futures, in the case of a short put option. Assignment is made on a random basis, and notice of assignment is made to option sellers by their brokerage firms. Option sellers do not determine whether or not they are assigned, nor do option buyers choose who is assigned when they exercise.

American-Style vs. European-Style

All options have an expiration date, after which the options cease to exist: option buyers no longer have rights and sellers no longer have obligations. The last day to exercise, and therefore the last day on which assignment may be made, depends on an option’s exercise style. There are two styles: American and European.

American-style contracts may be exercised/assigned on any trading day up to and including the expiration date. European-style contracts may be exercised/assigned only on the expiration date. Whether an option is American- or European-style depends on its contract specifications which are set by the exchange.

Option Premium

For calls and puts, the actual cash paid by an option buyer to the option seller is called the premium. It is an amount measured in U.S. dollars and cents, and its calculation is based on size of the underlying futures contract.

| Option | Quote | Contract size | Total Premium/Call |

|---|---|---|---|

| July 2014 Soybeans 1400 Call | $0.45/bushel | 5,000 bushels | $2,250.00 |

| July 2014 E-mini S&P 500 1870 Call | $33.00 | $50.00 x index | $1,650.00 |

| July 2014 Euro FX 1.3900 Call | $.01350 | 125,000 euros | $1,687.50 |

For an option buyer, call or put, the premium paid is nonrefundable. To recover any or all of the premium amount the option may be sold in the marketplace if it has value. An option seller keeps the premium amount initially received whether or not the short contract is assigned.

Strike (Exercise) Price

The specified price at which an underlying futures contract will change hands after an exercise or assignment is called the strike price, also referred to as the exercise price.

When a call is exercised, the buyer will buy (go long) the underlying future from the assigned call seller at the strike price, no matter how high its current market price may be.

When a put is exercised, the buyer will sell (go short) the underlying future to the assigned put seller at the strike price, no matter how low its current market price may be.

A call or put’s strike price is a standardized specification of the option contract, and is set by the exchange. It does not change during the option’s lifetime. In the marketplace the range of available strike prices, and the intervals between them, vary depending on the underlying futures contract. There will be strike prices set above and below an existing futures price. Additional strikes are added by the exchange if needed as the market value of a futures contract moves up or down.

September Japanese Yen futures are trading at 125. Available call strike prices might be 123, 124, 125, and 126. If the futures price rises to 126 you might find higher strike prices of 127 and 128 made available.

| Call Strikes | |

|---|---|

| 123 | |

| 124 | |

| Yen Futures Prices ► | 125 |

| 126 | |

| 127 | |

| 128 | |

| Calls | |

|---|---|

| Call Buyer/Holder | Call Seller/Writer |

| long call contract | short call contract |

| pays premium to seller/writer | collects premium from option buyer/holder & kept |

| right to buy (go long) particular futures contract at stated (exercise or strike) price | obligation to sell (go short) particular futures contract |

| if exercises that right | if assigned that obligation |

| on (or before) call expiration date/last trading day | on (or before) call expiration date/last trading day |

| Puts | |

|---|---|

| Put Buyer/Holder | Put Seller/Writer |

| long put contract | short put contract |

| pays premium to seller/writer | collects premium from option buyer/holder & kept |

| right to buy (go long) particular futures contract at stated (exercise or strike) price | obligation to sell (go short) particular futures contract |

| if exercises that right | if assigned that obligation |

| on (or before) call expiration date/last trading day | on (or before) call expiration date/last trading day |

September Japanese Yen futures are trading at 124. Available call strike prices might be 123, 124, 125, and 126.

If the futures price drops to 123 you might find lower strike prices of 122 and 121 made available.

| Put Strikes | |

|---|---|

| 121 | |

| 122 | |

| 123 | |

| Yen Futures Prices ► | 124 |

| 125 | |

| 126 | |

Example CALL Option on Futures Contract

| September 2014 Japanese Yen 126 Call | ||

|---|---|---|

| September 2014 | = | Expiration Month |

| Japanese Yen | = | Underlying Futures Contract |

| 126 | = | Strike Price ($.0126/Yen) |

| CALL | = | Type of Option |

What does this mean?

- Gives call buyer right to buy/go long, or call seller the obligation to sell/go short, one Yen futures contract

- At the price of $0.126/Yen

- At any time on or before September option expiration

- No matter how high the value of the Yen contract has risen

Example PUT Option on Futures Contract

| July 2014 E-mini S&P 500 1870 Put | ||

|---|---|---|

| July 2014 | = | Expiration Month |

| E-mini S&P 500 | = | Underlying Future Contract |

| 1870 | = | Strike Price (1870 index points) |

| PUT | = | Type of Option |

What does this mean?

- Gives put buyer right to sell/go short, or put seller the obligation to buy/go long, one E-mini S&P futures contract

- At the price of 1870 index points

- At any time on or before July option expiration

- No matter how low the value of the E-mini S&P contract has declined

In-the-money, at-the-money, out-of-the-money

An option’s strike price in relation to the current price of the underlying future determines whether it is in-the-money (ITM), at-the-money (ATM) or out-of-the-money (OTM).

| Call | Put | |

|---|---|---|

| In-the-money | Strike less than futures price | Strike greater than futures price |

| At-the-money | Strike same as futures price | Strike same as futures price |

| Out-of-the-money | Strike greater than futures price | Strike less than futures price |

A call or put is at any given time either in-the-money, at-the-money or out-of-the-money, and as the market price of an underlying futures contract changes this condition is dynamic. One way to look at this is to consider whether at any moment an option might be worth exercising.

Take an E-mini S&P 500 1870 Call for example. If the underlying E-mini future is trading at 1890, the call holder has the right to go long the future 20 points less than its current value. Is it worth exercising or not? Based on just the strike’s relationship to future price at that moment it would be. It’s “in-the-money.”

If the underlying E-mini future is trading at 1850, the call holder has the right to go long the future 20 points more than its current value. Is it worth exercising or not? Based on just the strike’s relationship to future price at that moment it would not be. It’s “out-of-the-money.”

Option Value vs. Underlying Futures Value

Changing value of a call or put’s underlying futures contract is the most influential factor affecting the option’s market price.

A call guarantees its buyer a fixed purchase price, the strike price, for the underlying futures contract, if the call is exercised. As the futures price rises that purchase price is worth more to a buyer so the call option increases in value. The opposite is true for a call if the futures price declines

A put guarantees its buyer a fixed selling price, the strike price, for the underlying futures contract, if the put is exercised. As the futures price declines that sale price is worth more to a buyer so the put option increases in value. The opposite is true for a put if the futures price increases.

| Underlying Futures Price | Call Prices | Put Prices |

|---|---|---|

| Increase | Increase | Decrease |

| Decrease | Decrease | Increase |

Intrinsic vs time value

- Option premium = intrinsic value (if any) + time value

- Intrinsic value = an option’s in-the-money amount, if any

- Time value = any premium in excess of intrinsic value

| Calls or Puts | ||

|---|---|---|

| In-the-money | ► | Intrinsic value + time value (if any) |

| At-the-money | ► | All time value |

| Out-of-the-money | ► | All time value |

Pricing Factor – Strike Price

Calls and puts on the same underling futures contract with the same expiration month will have a range of available strike prices. Again, standardized strike prices are set and specified by the option contract.

| Call Price | Put Price | |

|---|---|---|

| Higher Strike | Decrease | Increase |

| Lower Strike | Increase | Decrease |

Pricing Factor – Time until Expiration

Briefly put, more time until option expiration → more time for a favorable move in underlying future price → greater an option’s market price.

| Calls and Puts | |

|---|---|

| Time until Expiration Increases | Call and Put Prices Increase |

| Time until Expiration Decreases | Call and Put Prices Decrease |

| Effect of time on time value only | |

| CALL prices greater with more time | ||||

|---|---|---|---|---|

| CALL prices decrease with higher strikes | Sep Yen 126 Call | $4.00 | Oct Yen 126 Call | $5.00 |

| Sep Yen 127 Call | $3.00 | Oct Yen 126 Call | $4.00 | |

| Sep Yen 128 Call | $2.00 | Oct Yen 126 Call | $3.00 | |

| Sep Yen 129 Call | $1.00 | Oct Yen 126 Call | $2.00 | |

| PUT prices greater with more time | ||||

|---|---|---|---|---|

| PUT prices increase with higher strikes | Sep Yen 126 Put | $1.00 | Oct Yen 126 Put | $2.00 |

| Sep Yen 127 Put | $2.00 | Oct Yen 126 Put | $3.00 | |

| Sep Yen 128 Put | $3.00 | Oct Yen 126 Put | $4.00 | |

| Sep Yen 129 Put | $4.00 | Oct Yen 126 Put | $5.00 | |

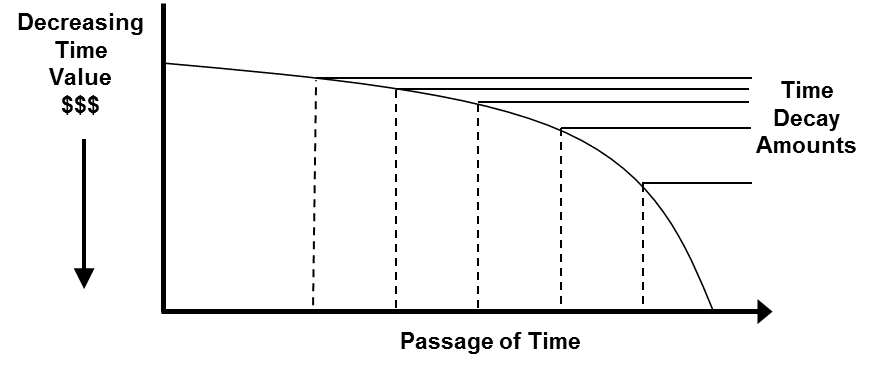

Pricing Factor – Time Decay

The time value portion of call and put premiums decreases over time. This is referred to as time decay. The rate of decay is not linear, it increases as expiration approaches.

Pricing Factor - Volatility

Volatility is a function of price movement of an underlying futures contract. Precisely, it is a measurement of price fluctuation up or down, not a sustained upward or downward price trend. It reflects the risk futures price may move through one or more strike prices during an option’s lifetime.

Call and put buyers want more volatility and are willing to pay more premium for it. Call and put sellers want lower volatility, i.e., more stability in prices of an underlying futures contract. They require more premium for the inherent risk of higher volatility levels.

| Calls and Puts | |

|---|---|

| Volatility Increases | Call and Put Prices Increase |

| Volatility Decreases | Call and Put Prices Decrease |

| Effect of volatility on time value only | |

Option Buyers Risk/Reward

- No margin upon purchase

- Must pay for long calls & long puts in full

- Maximum loss = limited to premium paid on purchase (no matter how/low underlying moves)

- Maximum profit = unlimited

Option Sellers Risk/Reward

- Margin required upon purchase

- Maximum loss = unlimited

- Maximum profit = limited to premium received at sale (no matter how/low underlying moves)

After Initial Purchase or Sale

Many investors buy calls or puts with no intention of exercising into a long or short underlying futures position. Instead they make an offsetting transaction to take a profit or cut a loss. Offsetting a call position in no way involves a put transaction, and vice versa.

| Initial (Opening) Transaction | Offsetting (Closing) Transaction |

|---|---|

| Buy call (long position) | Sell Call |

| Buy put (long position) | Sell Put |

| Sell/write call (short position) | Buy Call |

| Sell/write put (short position) | Buy Put |

Once a long position is offset a call or put buyer is out-of-the-market and no longer has rights to exercise and buy (for a call) or sell (for a put) the underlying futures contract.

Once a short position is offset a call or put seller is out-of-the-market and assignment is avoided. The seller no longer has the obligation to buy (for a call) or sell (for a put) the underlying futures contract.

Disclaimer

The information herein has been compiled by CME Group for general informational and educational purposes only and does not constitute trading advice or the solicitation of purchases or sale of any futures, options or swaps. All examples discussed are hypothetical situations, used for explanation purposes only, and should not be considered investment advice or the results of actual market experience. The opinions expressed herein are the opinions of the individual authors and may not reflect the opinion of CME Group or its affiliates. All matters pertaining to rules and specifications herein are made subject to and are superseded by official CME, CBOT and NYMEX rules. Current rules should be consulted in all cases concerning contract specifications.

Although every attempt has been made to ensure the accuracy of the information herein, CME Group and its affiliates assume no responsibility for any errors or omissions. All data is sourced by CME Group unless otherwise stated.

CME Group is a trademark of CME Group Inc. The Globe Logo, CME, CME Direct and Chicago Mercantile Exchange are trademarks of Chicago Mercantile Exchange Inc. CBOT and the Chicago Board of Trade are trademarks of the Board of Trade of the City of Chicago, Inc. NYMEX and ClearPort are trademarks of New York Mercantile Exchange, Inc. All other trademarks are the property of their respective owners.

Neither futures trading nor swaps trading are suitable for all investors, and each involves the risk of loss. Swaps trading should only be undertaken by investors who are Eligible Contract Participants (ECPs) within the meaning of Section 1a(18) of the Commodity Exchange Act. Futures and swaps each are leveraged investments and, because only a percentage of a contract's value is required to trade, it is possible to lose more than the amount of money deposited for either a futures or swaps position. Therefore, traders should only use funds that they can afford to lose without affecting their lifestyles and only a portion of those funds should be devoted to any one trade because traders cannot expect to profit on every trade.

Copyright © 2025 CME Group. All rights reserved.

About CME Group

As the world’s leading derivatives marketplace, CME Group is where the world comes to manage risk. Comprised of four exchanges - CME, CBOT, NYMEX and COMEX - we offer the widest range of global benchmark products across all major asset classes, helping businesses everywhere mitigate the myriad of risks they face in today's uncertain global economy.

Follow us for global economic and financial news.

© 2025 CME Group Inc. All rights reserved.