{kind=link}

E-mini S&P’s the Ultimate Index?

E-mini S&P's - The Ultimate Index?

The S&P 500 Index is one of the world’s most widely followed financial indicators, and the E-Mini S&P 500 futures contracts represent a significant part of the stock index futures activity. Of the 12 billion futures contracts traded globally in 2013, approximately 25% were stock index futures. The E-Mini S&P 500 futures was by far the most actively traded stock index futures contract in the world, with almost twice the activity of the second most active.

{kind=link}

Data Source:CME Group Data

The S&P 500 companies represent approximately 80% of the US economy, and the S&P 500 Index has become the primary barometer of global economic sentiment. Other regional stock indices periodically capture the market’s attention, but the action in the S&P 500 and E-Mini S&P 500 futures is almost always the starting point for any description of a given day’s events. Not only is the S&P 500 Index a top-line economic indicator, it is also used as a benchmark to more than $5.74 trillion in assets.

The S&P 500 Index consists of large capitalized stocks, and it is comprised of 10 distinct sectors, of which information technology currently accounts for nearly 19%, financials 16% and health care, a little over 13%. Individual companies’ earnings periodically have an impact on the direction of the futures, but expectations for the US and world economies are probably the most persistent daily influences. The S&P Index has, in the past, also reacted sharply to oil prices, geopolitical angst, monetary policy changes, inflation, deflation, recessionary concerns, terrorism, natural disasters and even holidays.

Since the 2008 financial crisis, US monetary policy and the Federal Reserve Bank have played a dominant role in supporting the economy. Owing to the loose monetary policy, stock index futures were able to sense the beginning of a recovery well in advance of the actual one in 2009. Three rounds of quantitative easing totaling more than 3 trillion dollars has helped the S&P 500 rally 194% off of its spring 2009 low to its recent new all-time highs in June 2014.

Expectations over the future course of monetary policy and debates over when US interest rates might begin to rise have become very important to daily trading opinions. Recent disappointments in US economic data have sparked concerns that the index has factored in too much growth. Ideas that valuations were running too high for the performance of the economy have sparked sharp corrections in the Index.

Current Advantages of Using E-Mini S&P 500 over Other Indices

Energy Influences Favor S&P 500 Index

Soaring oil prices have historically hindered the S&P 500 Index, but the United States has become more self-sufficient in energy to the point where the government has recently cleared the way for the export of crude oil. The fact that large oil companies are well represented in the S&P 500 Index suggests that the regular and E-Mini S&P 500 futures contracts could see less of a negative impact from surging oil prices and Middle East Geopolitical angst than other non-U.S. based stock index contracts.

Central Bank Edge Favors US-Based Indices

In a struggling global recovery, one of the primary bullish themes for stock index futures is the perception of a proactive central bank. Needless to say, the US central bank remains one the most proactive of any central bank, with the ECB and PBOC central banks thought to be among the most reticent to implement change. With the new US Fed Chairman Janet Yellen firmly touting sustained low interest rates far into the future and introducing new policy initiatives on wages and inflation that could allow for more tolerance of the initial signs of inflation, it is possible that US stock index measures will be able to benefit deeper into the global recovery than other foreign stock index measures. As of this writing, the FTSE Index was already dealing with the prospect of rising UK interest rates in anticipation of actions by the BOE, and that in turn forced the BOE to soothe fears by promising to be very careful with the eventual raising of interest rates.

Historical Performance

From October 1997 to June 2014, the E-mini S&P 500 has seen four large rallies and three declines. The rallies saw an average gain of 91% and have lasted just over five years on average. During the declines the market fell 43% on average and did so in about half the time it took to rally.

When the stock market reaches a turning point and is about to switch direction, the S&P 500 Index has usually been the first to confirm so, and has tended to produce a cleaner buy or sell signal. Perhaps this is because of the broader nature of the Index compared to the Dow and NASDAQ 100. However, the ensuing advance has generally been greater for the NASDAQ 100, perhaps because of its heavy concentration in technology and the general perception that it is comprised of higher-growth stocks. Still, the S&P 500 represents a good balance of technology-related shares as well as a broader range of companies that better reflect the entire the US economy.

| Stock Index Futures: Comparative Performances During Major Moves | ||||||

| S&P 500 | Dow Jones Index | NASDAQ-100 | ||||

| Time Frame | % Change | Duration* | % Change | Duration* | % Change | Duration* |

| March 2000 - October 2002 Tech Bubble Break |

-51% | 944 | -39% | 1004 | -84% | 944 |

| October 2002 - October 2007 Greenspan Expansion |

107% | 1826 | 99% | 1826 | 183% | 1826 |

| October 2007 - March 2009 Financial Collapse |

-58% | 517 | -55% | 517 | -55% | 397 |

| March 2009 - April 2011 Initial Recovery |

109% | 761 | 99% | 791 | 140% | 972 |

| April 2011 - October 2011 2011 Pause |

-21% | 183 | -19% | 153 | -16% | 92 |

| October 2011 - Current Second Recovery |

83% | 974 | 64% | 974 | 87% | 974 |

*Number of Days

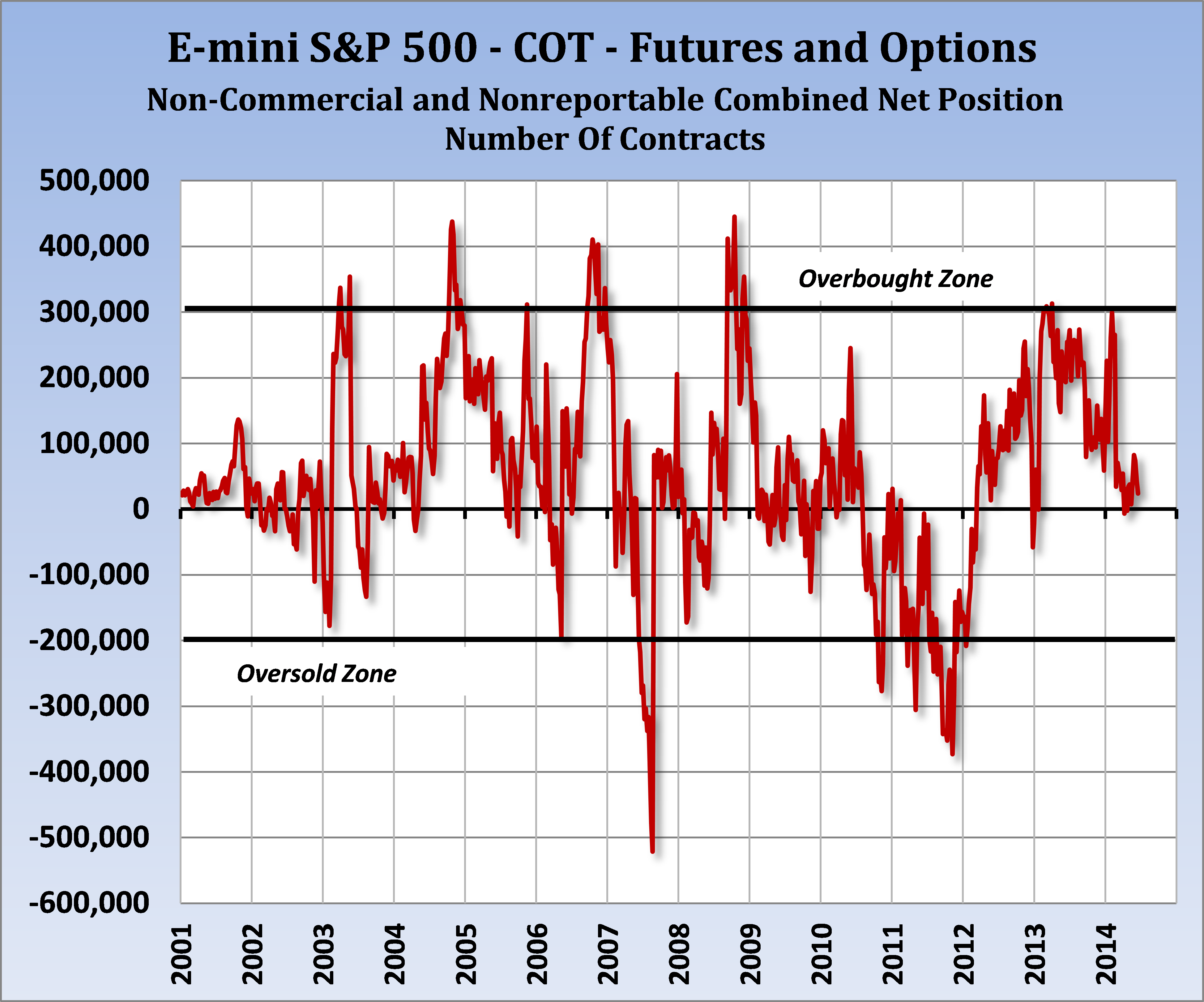

COT Positioning Report Touchstones

The weekly Commitments of Traders reports offer a window to the composition of the futures and options market. For the E-Mini &P 500 futures and options contract, the historical extremes of the combined large and small speculator net position provides a general idea of what constitutes an overbought or oversold market. The combined spec position refers to the net of both long and short positions in options and futures held by the non-commercial and non-reportable traders. By combining only these traders, who have a choice of being long or short, we can determine some rough form of sentiment. Commercials and hedgers typically have their market positioning dictated by their businesses and are therefore excluded from sentiment or overbought/oversold measurements.

A look at the frequently recurring extremes on the chart of the weekly COT positioning for the E-Mini S&P 500 (futures & options combined) indicates that a spec net long in excess of 300,000 contracts could be considered the beginning of the overbought zone. The all-time high reading was 445,459 contracts during the week of November 11, 2008. A frequently occurring net short extreme appears to be around -200,000 contracts, with the extreme weighing in at -521,003 contracts during the week of September 18, 2007.

{kind=link}

Data Source: Committment of Traders Report

The smaller size of the E-Mini S&P contract relative to the S&P 500 futures contract has facilitated an active and liquid trade in both the futures and options markets. This provides an opportunity to trade with lower margining costs