{kind=link}

Trading China Exposure

Trading China Exposure: Index Arbitrage and Futures Bases

As volatility returned to the global equity market amid major turbulence in China’s stock market in late 2015, CME Group launched E-mini FTSE China 50 Index futures to help market participants capitalize on market dislocations and better manage their risks during volatile periods. The FTSE China 50 Index measures the performance of Chinese companies listed in Hong Kong. It is constituted by including 50 of the largest and most liquid stocks. Approximately four months into its debut, the product has achieved good initial liquidity, especially during Hong Kong and U.S. trading hours.

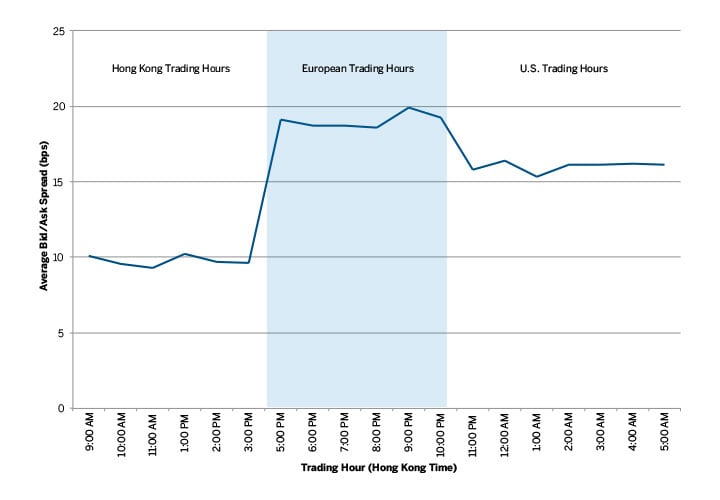

Figure 1 shows the average bid/ask spread in the front month of the E-mini FTSE China 50 Index futures by trading hour, sampled from January 4 to February 18, 2016. During the Hong Kong trading hours, the bid/ask spread hovered around 10 basis points; after the Hong Kong market closes, the spread widened to approximately 19 basis points. When the market in the U.S. opened, the spread tightened again to 15-16 basis points. The bid/ask spread phenomenon in Figure 1 is very mu ch expected considering index arbitrage and fair value.1

Figure 1. Bid/Ask spread of E-mini FTSE China 50 Index futures by trading hour

{kind=link}

DYNAMICS OF RICHNESS AND CHEAPNESS IN ADJACENT MARKETS

At its nascent stage, it is premature to describe with much certainty the richness or cheapness of the E-mini FTSE China 50 index futures market. However, adjacent futures markets exist in the Hang Seng Index futures as well as Hang Seng China Enterprise Index futures. They are both trading at the Hong Kong Exchange and Clearing. As illustrated in Table 1, these indices have many common constituents, both in terms of the count as well as the index weights.

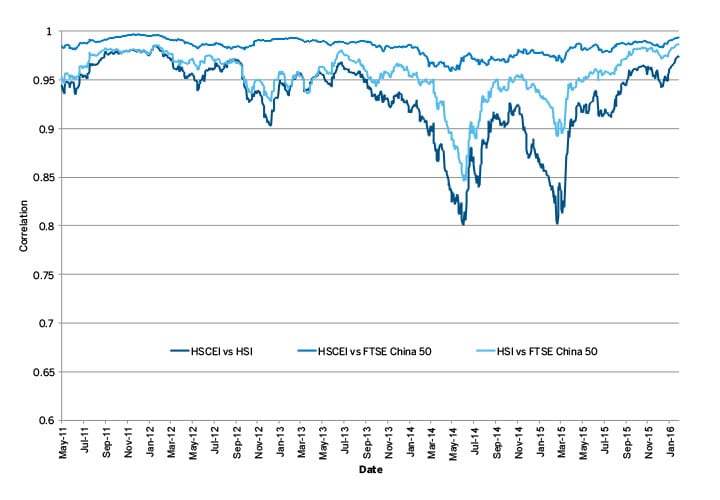

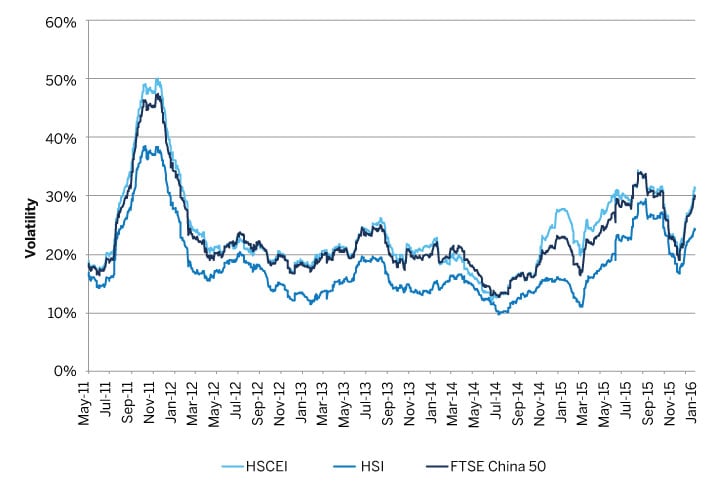

Beyond having large overlaps in constituents, the price movements for the indices are highly correlated, as illustrated in Figure 2, especially between the FTSE China 50 and HSCEI indices. Their volatility profiles track one another closely as well, as illustrated in Figure 3.

Table 1. Common index constituents among indices, by count and index weights, as of February 19, 2016.

| Index Pair | Common Constituents Index Pair and Index Weights |

| Hang Seng vs. FTSE China 50 | 17 stocks (51% of HSI / 70% of FTSE China 50) |

| HSCEI vs. FTSE China 50 |

34 stocks (95% of HSCEI / 64% of FTSE China 50) |

| Hang Seng vs. HSCEI | 9 stocks (58% of HSCEI / 24% of HSI) |

Figure 2. Rolling 60-day correlation between indexes

{kind=link}

Figure 3. 60-day historical volatility

{kind=link}

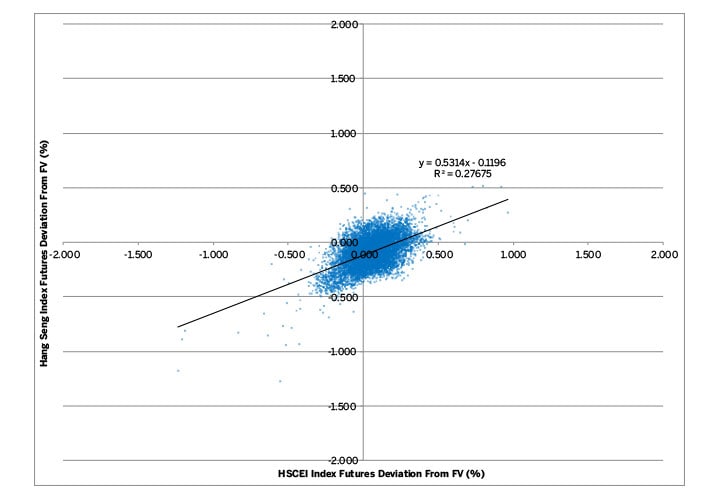

While the indices are similar and track similar portfolios, relative supply and demand can often drive the futures prices in different directions. Figure 4 illustrates this phenomenon.

Data in Figure 4 was sampled from August 5, 2015 to February 18, 2016. The front month of the Hang Seng and HSCEI index futures, as well as their underlying indices, are sampled every fi e minutes during the Hong Kong trading hours, and are represented as a blue dot on the graph.

Figure 4. Richness/Cheapness of front month HSI/ HSCEI Index futures, August 5, 2015 – February 18, 2016

{kind=link}

For each data point, the futures “arbitrage-free” prices were calculated.2 The futures prices were then compared to these theoretical arbitrage-free prices. The horizontal and vertical axes represent the deviation of HSCEI and HSI index futures from their respective theoretical prices. For example, at a particular point in time, if the HSI futures are 0.5% above theoretical value and the HSCEI futures are 0.5% below theoretical value, it will be represented as a blue dot on the top left quadrant at (-0.5%, 0.5%).

During this sampling period, the correlation between HSI and HSCEI was at or above 0.95 – as illustrated in Figure 2. While the two contracts tend to trade “rich” or “cheap” to their respective fair value simultaneously, it is apparent that one futures contract can be trading “rich” while the other is trading “cheap”. In fact, the R-square of the regression is only 0.27..

These conditions are results of temporary imbalance of end investor demands, e.g. rotation of interest in and out of China-specific securities. These temporary imbalances revert quite often. As a result, there are plenty of trading opportunities.

The addition of the E-mini FTSE China 50 index futures adds another layer of trading opportunities to the existing set of trading instruments; as referenced earlier, participants in the FTSE China 50 ETF listed in the U.S. (FXI) can use futures to manage their exposure. This trading opportunity extends beyond Hong Kong trading hours, as the index arbitrage between the U.S.-listed ETF and the E-mini FTSE China 50 Index futures continues. As the latter continues to gain traction, trading opportunities will certainly expand for all market participants.

E-mini FTSE China 50 Index Futures

| Ticker Symbols | CME Globex: FT5 Clearing: FT5 BTIC: FTC |

| Contract Size | USD $2 x FTSE China 50 Index |

| Min. Price Increments | Outrights: 5 index points = USD $10.00 Calendar Spreads: 1 index point = USD $2.00 BTIC: 1 index point = $2.00 |

| Trading Hours | CME Globex: Mon – Fri: 5:00pm CT previous day – 4:00pm CT |

| Contract Months | Five quarterly months (March quarterly cycle – Mar, Jun, Sep, Dec) |

| Last Trading Day | Trading can occur up to the close of trading at the Hong Kong Stock Exchange (HKEX) on the third Friday of the contract month: 3:00 am CST / 2:00 am CDT |

| Final Settlement | Via cash settlement based on the official closing index value of the FTSE China 50 Index |

As of the end of March 31, 2016, the FTSE China 50 Index consisted of the following constituents:

| Ticker | Constituent Name | Weight |

| 700 HK Equity | Tencent Holdings Ltd | 9.226252 |

| 941 HK Equity | China Mobile Ltd | 8.627603 |

| 939 HK Equity | China Construction Bank Corp | 8.523511 |

| 1398 HK Equity | ICBC | 6.296481 |

| 3988 HK Equity | Bank of China Ltd | 5.153089 |

| 2318 HK Equity | Ping An Insurance Group Co of China Ltd | 4.604837 |

| 2628 HK Equity | China Life Insurance Co Ltd | 3.918043 |

| 883 HK Equity | CNOOC Ltd | 3.888586 |

| 386 HK Equity | China Petroleum & Chemical Corp | 3.653219 |

| 857 HK Equity | PetroChina Co Ltd | 3.198885 |

| 688 HK Equity | China Overseas Land & Investment Ltd | 2.798239 |

| 267 HK Equity | CITIC Ltd | 2.238301 |

| 2601 HK Equity | China Pacific Insurance Group Co Ltd | 2.218488 |

| 3968 HK Equity | China Merchants Bank Co Ltd | 2.21795 |

| 1288 HK Equity | Agricultural Bank of China Ltd | 2.135192 |

| 728 HK Equity | China Telecom Corp Ltd | 1.96699 |

| 762 HK Equity | China Unicom Hong Kong Ltd | 1.744335 |

| 2328 HK Equity | PICC Property & Casualty Co Ltd | 1.624937 |

| 1109 HK Equity | China Resources Land Ltd | 1.594322 |

| 1044 HK Equity | Hengan International Group Co Ltd | 1.459311 |

| 1988 HK Equity | China Minsheng Banking Corp Ltd | 1.398589 |

| 6837 HK Equity | Haitong Securities Co Ltd | 1.340013 |

| 1088 HK Equity | China Shenhua Energy Co Ltd | 1.22892 |

| 6030 HK Equity | CITIC Securities Co Ltd | 1.227655 |

| 3328 HK Equity | Bank of Communications Co Ltd | 1.217249 |

| 1800 HK Equity | China Communications Construction Co Ltd | 1.216478 |

| 998 HK Equity | China CITIC Bank Corp Ltd | 1.068553 |

| 1766 HK Equity | CRRC Corp Ltd | 0.940995 |

| 6886 HK Equity | Huatai Securities Co Ltd | 0.940557 |

| 3699 HK Equity | WANDA COMM | 0.924883 |

| 1211 HK Equity | BYD Co Ltd | 0.905125 |

| 902 HK Equity | Huaneng Power International Inc | 0.870165 |

| 1776 HK Equity | GF Securities Co Ltd | 0.868433 |

| 1816 HK Equity | CGN Power Co Ltd | 0.779411 |

| 656 HK Equity | Fosun International Ltd | 0.76067 |

| 2202 HK Equity | China Vanke Co Ltd | 0.741313 |

| 914 HK Equity | Anhui Conch Cement Co Ltd | 0.737101 |

| 1359 HK Equity | China Cinda Asset Management Co Ltd | 0.730741 |

| 390 HK Equity | China Railway Group Ltd | 0.668399 |

| 1336 HK Equity | New China Life Insurance Co Ltd | 0.652059 |

| 1339 HK Equity | People's Insurance Co Group of China Ltd | 0.618647 |

| 2333 HK Equity | Great Wall Motor Co Ltd | 0.578767 |

| 2238 HK Equity | Guangzhou Automobile Group Co Ltd | 0.529395 |

| 1186 HK Equity | China Railway Construction Corp Ltd | 0.51689 |

| 6818 HK Equity | China Everbright Bank Co Ltd | 0.368405 |

| 753 HK Equity | Air China Ltd | 0.298056 |

| 2727 HK Equity | Shanghai Electric Group Co Ltd | 0.29633 |

| 2799 HK Equity | China Huarong Asset Management Co Ltd | 0.200799 |

| 1618 HK Equity | Metallurgical Corp of China Ltd | 0.180399 |

| 1033 HK Equity | Sinopec Oilfield Service Corp | 0.106434 |

APPENDIX A:

Understanding “Fair Value”

The fair value, or theoretical level at which futures should be expected to trade, is a function of the cash index value plus implied financing, less dividends paid over the life of the contract:

Fair Value = Spot + Financing Advantage – Foregone Dividends

Unlike the buyer of a cash basket of index securities, who must finance the full notional value of the trade at inception, the buyer of a futures contract must only post a fraction of the notional as margin, and can invest the remaining cash in an interest-generating instrument. At the same time, the seller of futures must replicate the index returns. The amount of financing advantage above the cash basket depends on the interest rate (e.g. Interbank offer rate), as well as the time to expiration of the futures, and is reflected in the futures price. The magnitude of the financing advantage will shrink over time, until it reaches zero on the expiration day of the futures contract.3

Mathematically, the financing advantage is:

Spot Index x Interest Rate Benchmark x Time to Futures Expiry

Conversely, the buyer of a cash basket is entitled to dividend payments, while the buyer of futures is not. As a result, futures prices are adjusted downward by the amount of this foregone dividend stream to reflect this disadvantage to the buyer. Much like the financing advantage, the foregone dividend also shrinks over time, until it reaches zero on the expiration day of the futures contract.4

Hence, equity index futures trade at a premium or discount (known as the basis) relative to the cash index level, depending on whether the implied financing is greater or less than expected dividends over the duration of the contract.

Most CME Group index futures, including E-mini FTSE China 50 Index futures, can be traded through a Basis Trade at Index Close (BTIC) mechanism. The buyer and seller consummate the initial trade in terms of the basis,

i.e. the difference between futures price and the spot index. This is the same as the financing advantage less the foregone dividends. At the close of trading in the cash security market, the closing index value is known. The trade of the index futures will be concluded at the price of the closing index value plus this basis.

In essence, this mechanism allows participants to trade at fair value based on the closing index value of the day. For more information, please visit cmegroup.com/btic.

“Classic” Index Arbitrage

Market participants monitor the fair value and capitalize on price discrepancies between spot and futures levels by purchasing the cheaper alternative and selling the more expensive one. This activity, known as index arbitrage, prevents futures from trading far above or below fair value.

Futures and cash index value are publicly observable variables. Dividend streams are highly forecastable as company paying dividends would declare the dividend ahead of the ex-dividend dates. Given these quantities, the only “free” variable is the financing rate priced in by the relative prices of futures and cash index. It is thus customary to describe the market as “rich” if the implied financing rate of futures is higher than benchmark interbank financing rates. Conversely, the market is described as “cheap” if the implied financing rate5 is lower than the benchmark interbank financing rates.

When the futures price is trading “rich” or above its fair value, the premium over the spot price paid by the buyer of futures is greater than the actual cost to buy the cash basket until maturity. In this scenario, traders can sell short the futures and purchase the cash basket, thereby exerting downward pressure on the futures price and pushing upward on the cash index level until the actual basis is brought in line with fair value.

Alternatively, when the futures price is trading “cheap” or below its fair value, traders can buy the futures and sell short the underlying stocks to reestablish equilibrium. This scenario differs slightly in that a short sale of securities requires a loan of shares to sell short by a prime broker.

In reality, the costs associated with executing the arbitrage result in a no-arbitrage band within which the prices of spot and futures move without creating an arbitrage. In the scenario where futures are “cheap”, the short sale of securities requires a loan of shares to sell short by a prime broker. This borrow cost, quoted as an annualized fee, can vary significantly depending on the number of lenders and the demand for borrow, and must be known before evaluating the arbitrage opportunity. For example, if the broker fee is 50bps for borrowing the basket of securities to sell short, the implied financing cost of futures must be at least 50bps in order for the arbitrage to be attainable.

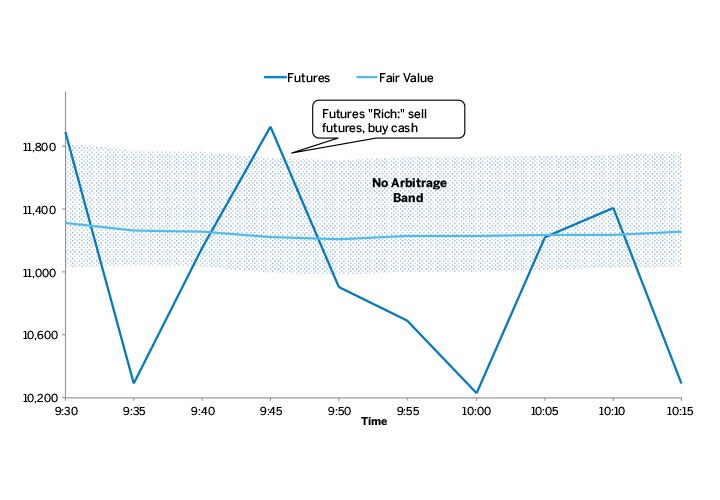

Figure 5 illustrates this arbitrage-bound band around fair value. Should the futures price exceed the upper bound or fall below the lower bound, then an arbitrage opportunity would emerge.

Figure 5: No Arbitrage-Band

{kind=link}

References

1 A more thorough explanation of fair value is detailed in Appendix A.

2 Futures prices were calculated based on the then current index value and the 1-month HIBOR as the interest rate benchmark.

3 Another way to interpret this futures premium due to financing advantage is to see it as the cost of leverage being grossed up and added to the price of the futures contract. As this gross-up amount declines, the financing cost is paid.

4 Alternatively, you can interpret the reduction of the discount of futures price due to foregone dividend as constructively receiving the foregone dividend via capital gains, as the futures price drifts up over time.

5 The "richness" or "cheapness" is the most apparent into the "roll market", in which traders swap the front month position for a back month position. These calendar spread trades are purely driven by the implied financing rate. See, for example, the quarterly roll monitor at CME Group's website for U.S. indices: www.cmegroup.com/rollpace.

View this article in PDF format.