Since 2014, cost pressures have continued to mount in the bilateral swap market and voluntary clearing of OTC products has increased. Interest rate swap clearing in G4 currencies has increased 80%, while clearing in the 17 currencies outside of the G4 has soared 238% across the industry.

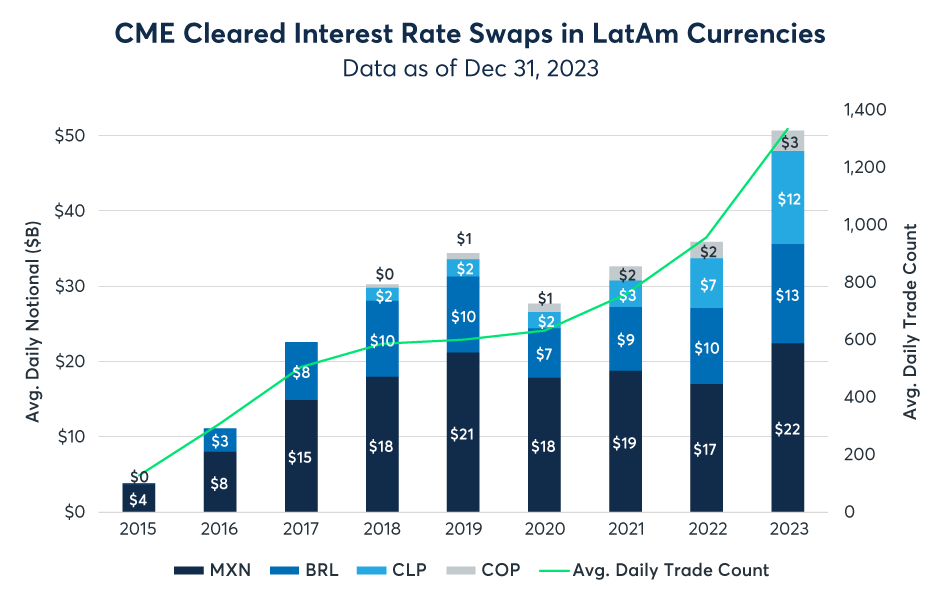

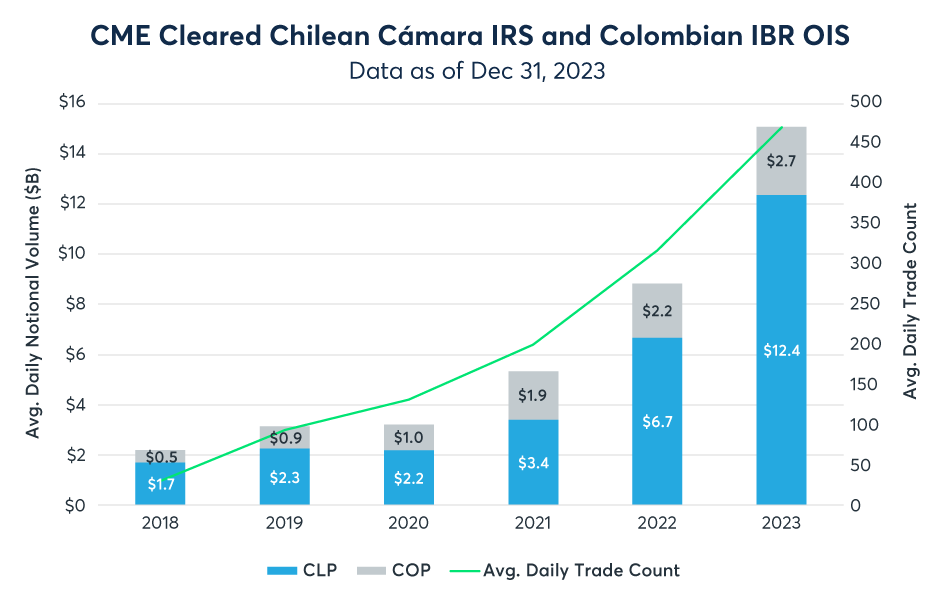

CME is the global leader in Latin American (LatAm) swap clearing. Since launching MXN TIIE and Brazilian CDI swaps, volume and participants have continued to grow in what is now a deeply liquid cleared swap market. In response to strong customer demand, on May 21, 2018 we launched Chilean Peso (CLP) and Colombian Peso (COP) swap clearing. To enhance our customers capital efficiencies in their LatAm businesses, we offer regular compression cycles for Brazilian and Mexican swaps.

Contact Us

CONVERSION PLAN

Cleared MXN 28D TIIE swaps transition

As a part of the global transition to risk-free rates, Mexico will be transitioning from 28D TIIE to the TIIE de Fondeo, or F-TIIE, for its benchmark interest rate. CME Group is working to help facilitate this transition for cleared swaps.

- Cleared IRS ADN in Latin American currencies exceeded $60 billion per day in 2024; +19% YoY,

- 410+ unique global participants have cleared LatAm IRS at CME Group, including 75+ LatAm based participants.

- Over $18.1 trillion compressed by TriReduce in LatAm currencies.

- 74TriReduce cycles in LatAm currencies with members and non-members participating.

Mexican TIIE IRS and F-TIIE OIS

- 2024 ADN: $28.9 billion ADTC: 664.

- 345 participants clearing to date.

- 40+ liquidity providers and 20 FCMs live.

- TIIE conversion successfully completed in November 2024; TIIE28 Waiver Period ends December 31, 2025.

Brazilian CDI IRS

- 2024 ADN: $16.2 billion ADTC: 257.

- 268 participants clearing to date.

- 30+ liquidity providers and 16 FCMs live.

Chilean Cámara IRS and Colombian IBR OIS

- CLP 2024 ADN: $12.2 billion ADTC: 307.

- COP 2024 ADN: $3.3 billion ADTC: 161.

- 235 CLP participants clearing to date.

- 226 COP participants clearing to date.

- 30+ liquidity providers and 19 FCMs live.

| Product Name | Product Type | Maximum Maturity | Floating Rate Index | Settlement Currency | Price Alignment Rate | Variation Margin, Coupons and Fees | Holiday Calendar | Settlement & Business Day Convention |

FX Rate |

|---|---|---|---|---|---|---|---|---|---|

| Mexican Peso (28D TIIE IRS) |

Interest rate Swap | 31 Years | MXN-TIIE-Banxico | MXN | SOFR adjusted by FX overnight and tomorrow next rates | MXN | Mexico City | MXN will be settled on a next day (T+1) basis Default will be ACT/360 | |

| Mexican Peso (F-TIIE OIS) | Overnight Index Swap |

31 Years | MXN-TIIE ON-OIS Compound | MXN | SOFR adjusted by FX overnight and tomorrow next rates | MXN | Mexico City | MXN will be settled on a next day (T+1) basis; Default will be ACT/360 | |

| Brazilian Real | Zero Coupon Swap | 10 Years | BRL-CDI* | USD | SOFR | USD | Brazil Business Day** | USD will be settled on a next day (T+1) basis Default will be Bus/252 | The below FX rate will be used to convert BRL coupon payments to USD: “ask” price reported on Bloomberg Page BZFXPTAX at approximately 1:15 p.m. Sao Paulo time, on the relevant date |

| Chilean Peso | Interest Rate Swap, Zero Coupon Swap | 20 Years | CLP-TNA (Indice Cámara Promedio) | USD | SOFR | USD | Santiago (CLSA) and New York (USNY) | Santiago (CLSA) and New York (USNY) | CLP.DOLAR.OBS/CLP10 |

| Colombian Peso | Overnight Index Swap | 20 Years | COP-IBR-OIS-COMPOUND | USD | SOFR | USD | Bogotá (COBO) and New York (USNY) | USD will be settled on a next day (T+1) basis. Default will be ACT/360 | COP.TRM/COP02 |

* Refers to the Overnight Brazilian Interbank Deposit Rate Annualized as the average of the DI-OVER-EXTRA Grupo as published by CETIP

** A business day in any of San Paulo, Rio de Janeiro or Brasilia not otherwise declared as a financial market holiday by the BM&F

© 2026 CME Group Inc. All rights reserved.