{kind=link}

Three Factors That Could Undercut U.S. Farmland Values

Over the past century, U.S. farmers lived through two major crises, in the 1920s & 1930s and the 1980s. The latter occurred during a period of depressed prices for corn, soybean and wheat and a dramatic tightening of monetary policy. Inflation-adjusted farmland prices fell by over 40% during the 1980s and the Farm Credit System experienced large losses, which contributed to the stress of Savings and Loans (S&L) institutions as well as some medium and larger-sized banks.

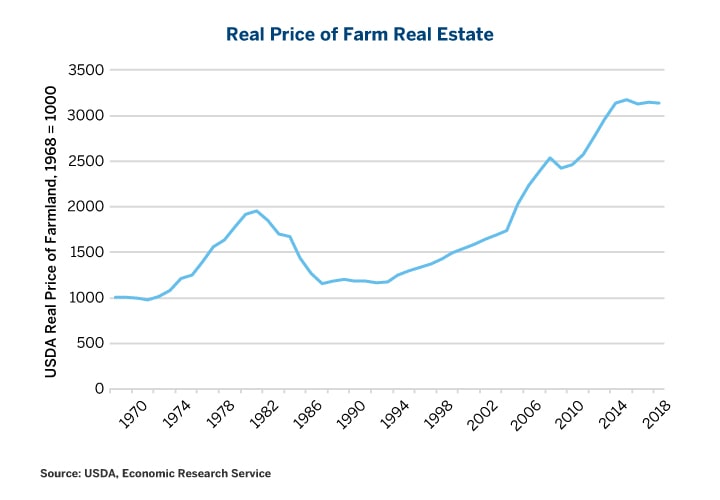

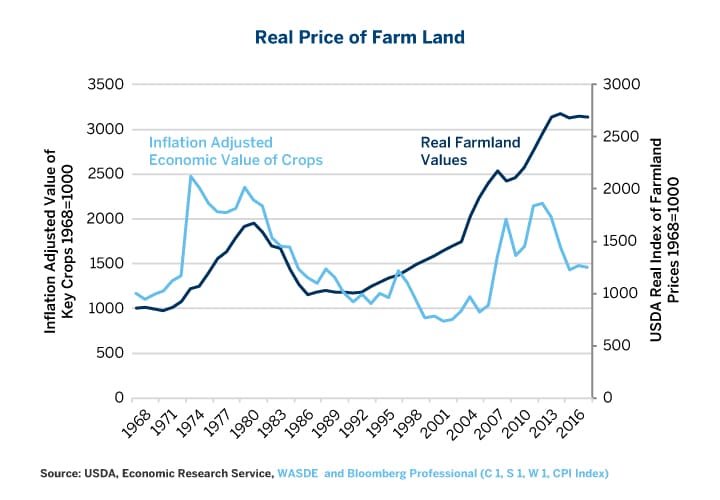

Since hitting bottom in the early 1990s, the price of agricultural land has soared, rising 169% in real terms between 1994 and 2015. Moreover, agricultural land values were largely untouched by the financial crisis, experiencing only a small dip in 2009. Since 2015, however, farmland prices have gone sideways (Figure 1). Could they be in for a significant decline in value? The answer to the question depends upon three factors: interest rates, the U.S. dollar and the price of key crops.

Figure 1: Farmland Values Rose 170% More Than Consumer Prices Between 1994 and 2015

{kind=link}

Interest Rates

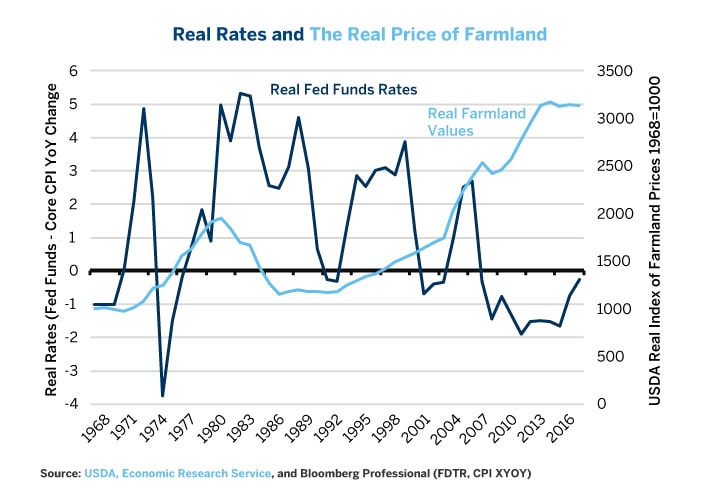

The Fed has brought interest rates back to zero in real terms. For much of the last decade, the real rate of interest in the US was negative. Short-term interest rates were around 0.125% while inflation varied from 1-2%. This fuelled a boom in farmland prices just as it had four decades earlier when the Fed held rates below inflation between 1968 and 1971, and again from 1975-77.

By contrast, extremely high real interest rates during the 1980s were a major contributing factor to that decade’s collapse in farmland values. Farmland prices began to rise again, albeit very slowly, during the 1990s, as interest rates came down but remained significantly positive for most of that decade. It wasn’t until after the Tech Wreck in 2001, when the Fed first cut interest rates to close to zero in real terms, that farmland prices began soaring (Figure 2).

Figure 2: Low/Negative Real Rates Tend to Fuel Rises in Farmland Value

{kind=link}

Now that the Fed is bringing rates back to positive in real terms, can farmland prices resume their rise, or will they fall? That depends in part upon how far the Fed goes. The Fed’s dot plot suggests that it intends to put short-term lending rates at around 3% by the end of the decade. Fed funds futures suggest that rate will most likely fall short of the Fed’s estimate but will still rise towards 2.75%. That would take rates to about 1% in real terms. 1% real rates might not be enough to dampen farmland prices by itself, but they could serve as a significant drag on any further gains.

Even if rising U.S. interest rates don’t negatively impact U.S. farmland values in a direct sense, by slowing the flow of credit and reducing the number of buyers, they could impact farmland values indirectly by pushing the US dollar higher and crop prices lower.

The U.S. Dollar and Emerging Market Currencies

U.S. agricultural production has shrunk as a share of the world total. Since 1997, U.S. corn production has declined from 41% to 34% of the world total, while soybean production has fallen from 46% to 33%. Wheat production has shrunk from 11% to 6.5% of the world total. Meanwhile, Brazilian production of corn has tripled and soybean output has nearly quadrupled. Argentina has seen its production of corn and soybean grow by 100% and 200%, respectively, over the same period. Meanwhile, Russian and Ukrainian wheat production has risen by nearly 50%.

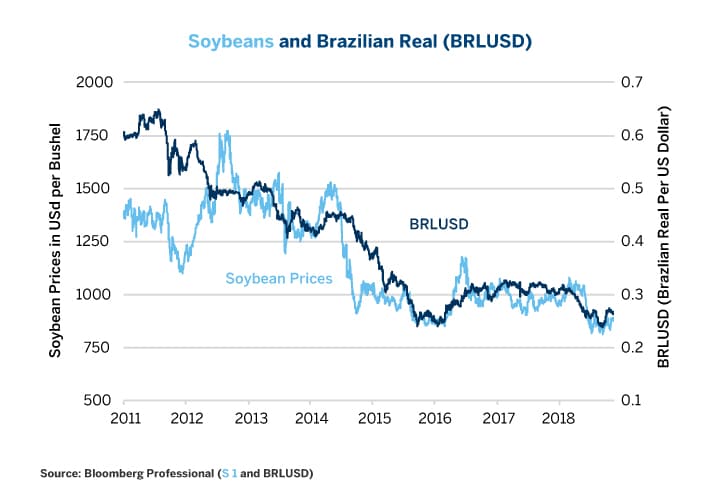

Figure 3: Brazilian Real and Soybean Prices

{kind=link}

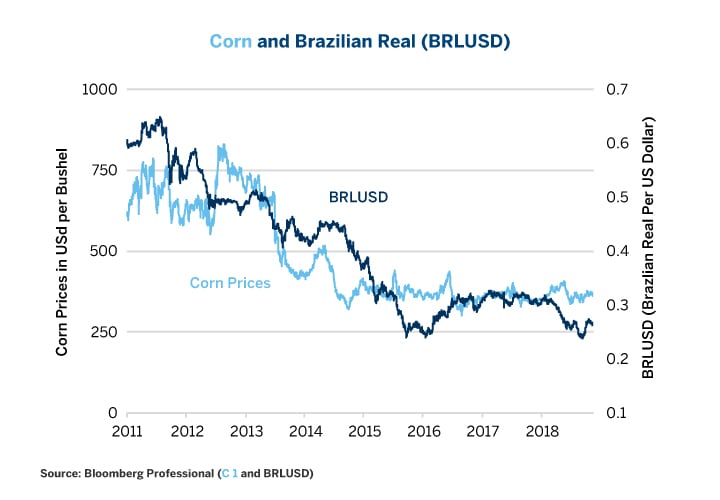

Given the rise of rival producers, it’s not surprising that the value of corn, soy and wheat has begun to track movements in currencies like the Brazilian real (BRL) and Russian ruble (RUB). When these currencies fall versus the U.S. dollar, often the prices of key crops fall along with them (Figures 3, 4 and 5).

Figure 4: Corn Prices Often Track BRL as Well

{kind=link}

Higher U.S. interest rates are contributing to the unwinding of long positions in these currencies. For much of the past decade, investors could borrow nearly for free in the U.S. dollar and lend at much higher rates (close to 10%) in places like Brazil and Russia. Now, with rising U.S. rates and unsteady commodity prices, BRL and RUB have been falling. The decline in these and other emerging market currencies benefits their farmers and lowers the global cost of production for agricultural commodities to the detriment of U.S. producers.

Figure 5: The Russian Ruble Exerts a Strong Influence on Global Wheat Prices

{kind=link}

The Price of Agricultural Goods

The value of farmland is driven by many factors, including the level of interest rates and market psychology/momentum. Another important factor is the value of agricultural production. We define this as the total production of key cash crops such as corn, soy and wheat multiplied by their average inflation-adjusted prices throughout the year.

The 1970s boom in farmland prices was preceded by a huge run-up in the value of agricultural production as prices soared, especially after 1973. Likewise, the 1980s collapse in farmland values followed on the heels of a bear market in agricultural prices that began in 1981 and didn’t hit bottom until after 2000. The later stages of the recent bull market in farmland values came after prices of corn, soy and wheat began soaring in 2007 and remained high until 2013. Since 2013, however, prices for key crops have mostly fallen to a mid-range between their 1990s and early 2000s lows and their recent highs (Figure 6).

Figure 6: Land Values Tend to Follow Crop Values

{kind=link}

Where these prices go in the future might play a key role in the evolution of farmland values. If they rebound, the value of farmland might resist the downward pull of higher interest rates. However, if corn, soy and wheat prices fall further, perhaps under pressure from a strong dollar and rising international competition, this could compound the problem of newly positive real interest rates and send farm prices on a 1980s-style slide to the detriment of both farmers and any financial institutions that have loaned them money.

To that end, the trade war between the US and China is unwelcome news, as it is likely to add to stress in the farm sector. Already, we have seen a sharp increase in U.S. soybean inventories, which could depress prices further in the future.

Bottom line:

- Farmland values seem to follow real interest rates and the value of agricultural production.

- Positive real rates might not be good for the value of U.S. farmland.

- A strong dollar could be bearish for crop prices.

- What happens to farmland values in the future might depend upon whether higher crop prices offset the potentially negative influence of higher interest rates or whether lower prices for corn, soy and wheat compound them.

Hedging Ag Markets in 2019

How will ag markets fare in 2019? The answer could depend to some extent on whether the United States and China are able to resolve their trade dispute and end the tit-for-tat tariffs between the world's two largest economies. Hedge your investment portfolio against the uncertainty with futures and options.