{kind=link}

The Rationale for Ag Options' Upward Skew

The Rationale for Ag Options’ Upward Skew

Across most markets, out-of-the-money (OTM) put options tend to be more expensive than OTM call options. This is most obviously true in the equity market, where investors fear downside risks more than upside risks. It’s also true in the crude oil market, where, despite political risks to the upside, downside risk is usually the main concern. Precious metals, fixed income and currency markets are quirkier and, by-and-large, upside and downside risks are more symmetrical or, at least, more time varying. Options on agricultural goods, however, are unique: call options are usually more expensive than puts – between 74% and 99% of the time since early 2017, depending on the product (Figures 1 -3).

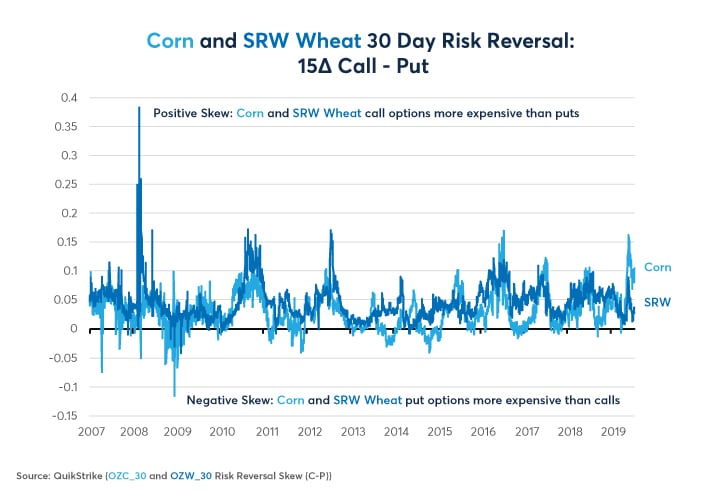

Figure 1: Since 2007, Corn Options Have Been Positively Skewed 84% of the Time; Wheat 99%.

{kind=link}

Figure 2: Soybean & Soymeal Have Been Positively Skewed 74% & 80% of the Time, Respectively.

{kind=link}

There are two broad explanations for the upside skew (also called “risk reversal”) in ag options. First, it could be that the underlying price behavior in these markets shows positive skewness. If so, the positive skewness in options markets would be a logical response. Secondly, if there is no positive skewness in underlying prices returns, the other major explanation is market structure: food buyers are more willing to pay premiums for upside protection than farmers are to pay for downside protection.

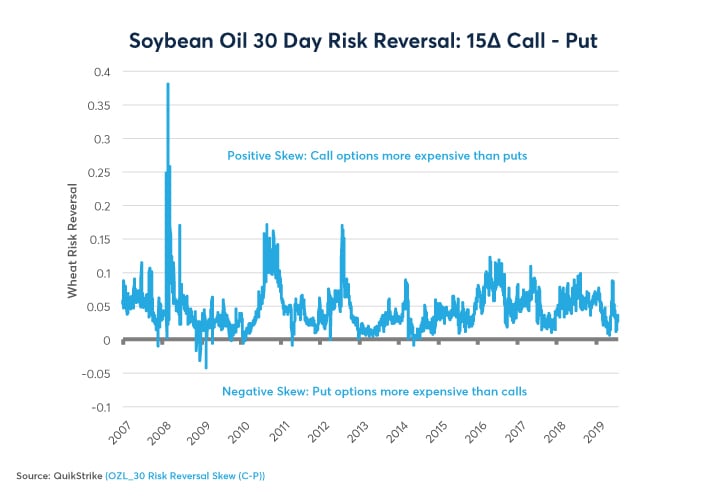

Figure 3: Since January 2007, Soybean Oil Options Have Been Positively Skewed 99.3% of the Time.

{kind=link}

The first of these explanations is easy to test. While one might imagine that the threat of droughts, floods, heat waves and cold spells might put a positive skew in agricultural goods price returns, using daily data since 1970, there is no persistent upside skewness to the underlying returns of corn, wheat, soybeans or soymeal. In fact, soybeans have shown a persistent, if slight, negative skewness in daily price returns. Soybean oil is an exception. Since 1970, there has been a slight upside skewness in daily price returns but not one that would pass most significance thresholds: usually skewness has to be greater than +0.5 to meet even minimal significance tests (Figure 4).

Figure 4: Outside of Soybean Oil, there is no Persistent Upside Skewness in Daily Price Returns.

{kind=link}

As such, this leaves us with the structural explanation of the upside skewness in crop options markets. On the supply-side of the agricultural markets are millions of farms operating world-wide, including 2.16 million in the US alone. For these millions of farmers, the chief risk is, of course, a decline in prices. On the demand side are a relatively small number of firms that purchase a large portion of the world’s crops for processing, distribution and sale. For these food buyers the primary risk in a sudden and extreme rise in prices.

The upside skewness may result from a combination of factors. First, many producers may sell their grains and oilseeds forward but then buy call options so that they can benefit from extreme upside moves in prices. While hedging strategies vary from producer to producer, they may in aggregate be more willing to sell futures and buy calls than to hedge by buying put options. Secondly, buyers of grains and oilseeds, who are much less numerous, may be willing to hedge extreme upside risk with OTM calls. This isn’t to suggest that there aren’t food producers or even food buyers who use puts; rather that there is a structural bias in the market for paying for more for OTM calls than paying for OTM puts despite a general lack of evidence that agricultural goods markets are more susceptible to extreme upside than extreme downside moves.

The other item to note about skewness is that it isn’t consistent over time. Sometimes the agricultural goods markets do show negative skewness. Is this a warning sign of further price declines to come? Or is it a signal that agricultural goods are oversold and that prices are likely to bounce back? Likewise, at times the upwards skewness moves to extreme levels. Is this a signal of further prices rises to come or a signal that the market is overbought and susceptible to near term declines? Our analysis doesn’t provide a definitive answer to these questions but might nevertheless offer some useful insights.

To answer these questions, we indexed the skewness on a scale of 0-100 over rolling two-year periods and compared it to the actual payoff of a fully funded long futures position in the various crops over the subsequent three months (so there’s no look-ahead bias). For example, if the crop option skewness was the most skewed to the downside it had been during the previous two years, the index would have a reading of zero. If the crop option market was the most positively skewed that it had been during the past two years, the index would have a reading of 100. We then broke the results down into deciles and looked at the subsequent three-month performance of the reinvested futures rolled 10 days prior to expiry from 2008 until early 2019.

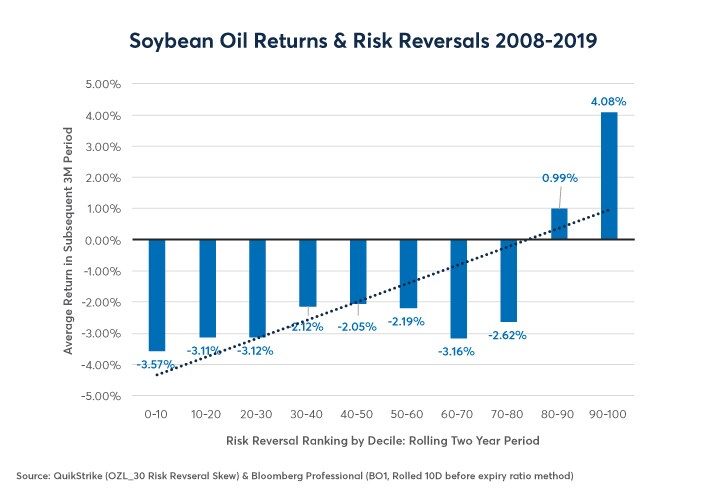

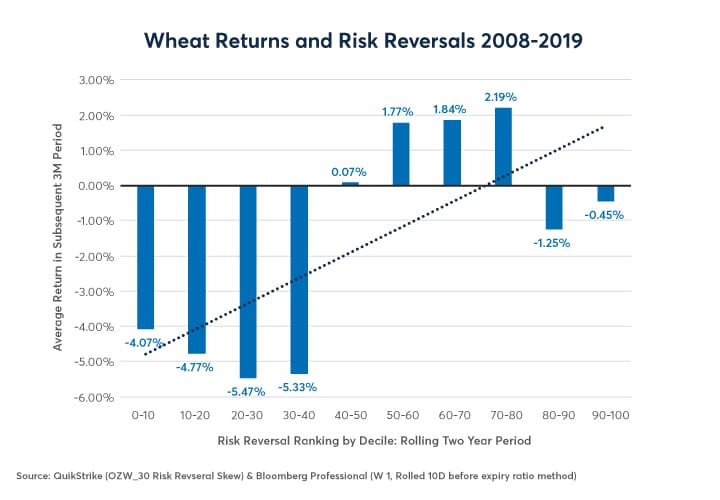

In the two markets which have the strongest tendency to be positively skewed, soybean oil and wheat, options traders did a pretty good job of anticipating directional risks between 2008 and 2019. When upside skewness was less than average (and in rare cases outright negative), futures prices tended to fall over the next three months. When skewness was exceptionally positive, the return on futures contracts tended to be more positive (Figure 5 and 6).

Figure 5: Soybean Oil Options Skewness Has Been Positively Correlated with Future Price Movements.

{kind=link}

Figure 6: Lower-Than-Average Positive Skewness in Wheat has Often Signaled Further Price Declines.

{kind=link}

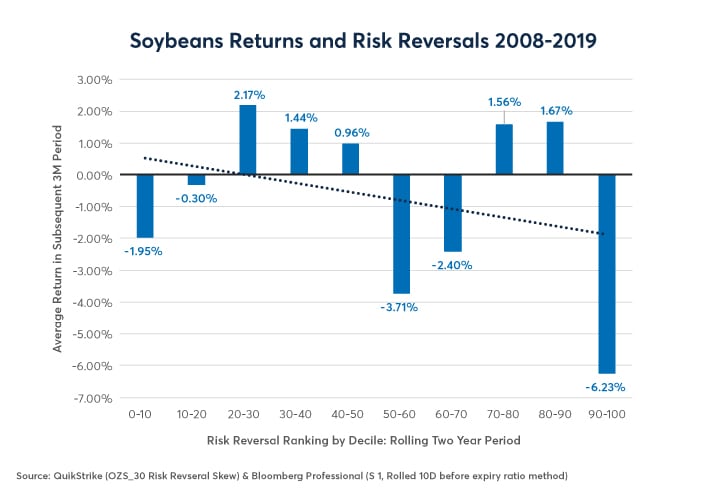

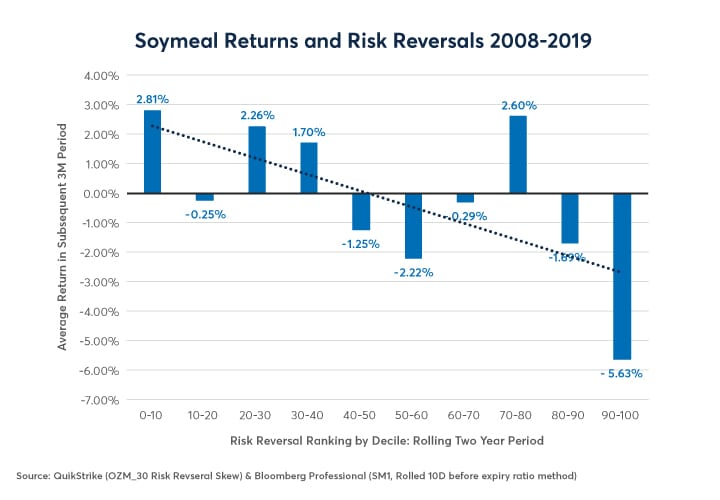

For soybeans and soymeal, the two options markets with the weakest inclination towards positive skewness in options prices, the correlation between the degree of skewness and subsequent movements in futures prices has worked the opposite way. Extreme positive skewness was often a sell signal during the 2008 to 2019 period whereas extreme negative skewness sometimes signaled those markets hitting bottom and were about to rally (Figures 7 and 8).

Figure 7: Extreme Positive Skewness Sometimes Correlated with Coming Soybean Price Declines.

{kind=link}

Figure 8: Soymeal Future Returns Correlated Negative With Its Degree of Skewness From 2008-2019.

{kind=link}

Between 2008 and 2019, corn prices have done best at the extremes; when skewness was exceptionally high or low. By contrast, corn prices tended to fall over our sample period when skewness was close to its two-year moving average (Figure 9).

Figure 9: Corn Showed the Weakest Correlation with Options Skewness Among the Crops.

{kind=link}

We would emphasize that these results are sensitive to their sample period and going forward the relationship between current levels of options skewness and subsequent changes in futures prices could look very different than it did in the past decade. Also, the lack of consistent result among the various agricultural goods suggests that options skewness as an indicator of future returns should be taken with a large grain of salt. Nevertheless, even for those who don’t deal in the options markets, the relative prices of OTM calls and OTM puts might be worth looking at if only to ask questions about how the market is currently positioned.

Bottom Line

- Agricultural options markets display a nearly consistent upward skewness.

- The skewness appears to result from market structure and not from skewness in the price returns of the underlying goods.

- Wheat and soybean oil have the strongest tendency towards positive skew.

- The degree of skewness isn’t necessarily a reliable indicator of future price movements.

Ag Options

Our diverse selection of Agricultural options offers the flexibility you need for effective risk management and the ability to execute volatility strategies or event-driven trades. Our portfolio of Grain, Oilseed, Livestock, and Dairy products provides an array of opportunities from outright and spread options, including Calendar and Intercommodity Spread Options, to short-term alternatives such as Weekly and Short-Dated New Crop Options.