{kind=link}

"Super-Contango" and the Bottom in Oil Prices

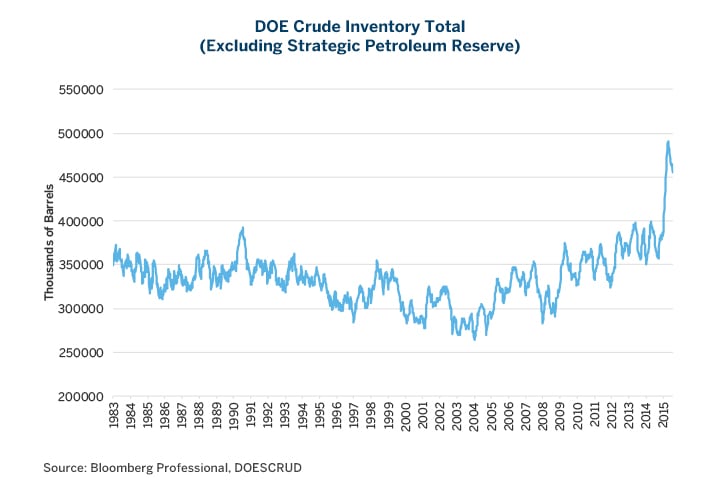

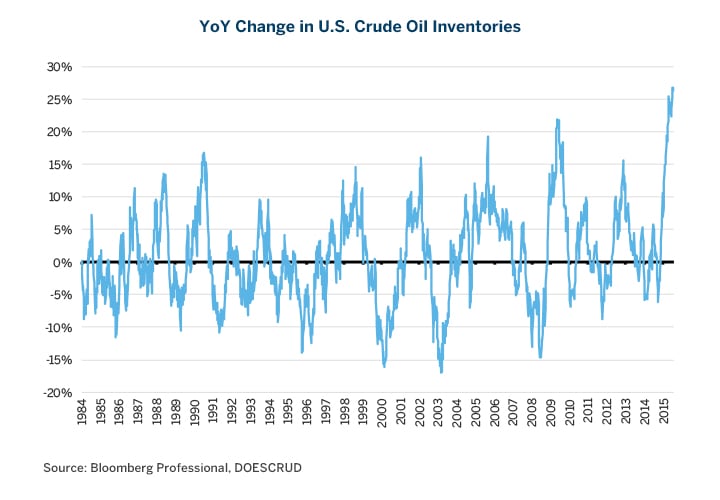

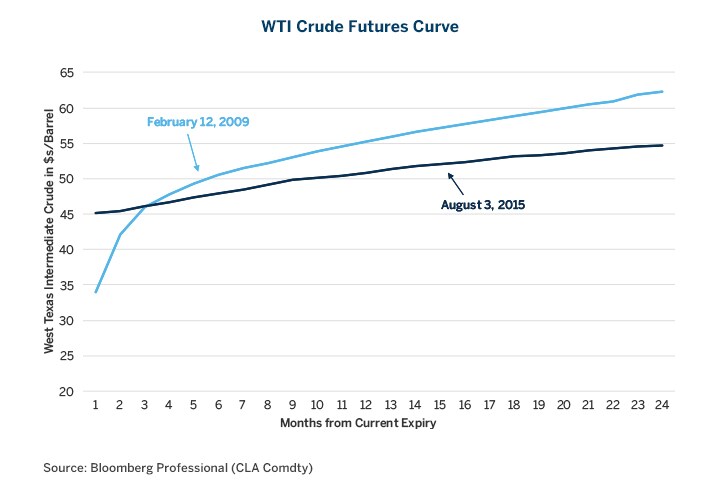

Currently, the oil curve is much less steep than it was at the bottom in 2009. This might indicate that oil prices have substantial further downside before supply and demand are brought in line.In our article, “Soaring Oil Inventories: Prices Heading for a Second Collapse?” published on June 4, 2015, we discussed the possibility that oil prices might drop again after the collapse of 2014 unless Americans drove enough to absorb the excess inventories. As we approach the end of the summer driving season, the outcome is looking pretty clear. While Americans are driving about 5% more miles than they did last year, oil inventories have not been declining as much as they usually do at this time of year. Not only are inventories near record highs (Figure 1), their year-on-year pace of increase is at a record-breaking 25% (Figure 2).

Figure 1: U.S. Oil Inventories are Close to Record Highs.

{kind=link}

Figure 2: Oil Inventories are Growing at a Record Pace with a Smaller Than Normal Summer Decline.

{kind=link}

In addition to rising inventories, the price of oil is under pressure for a number of other reasons:

- Top exporter Saudi Arabia’s production has hit a record high.

- US production continues to grow despite lower prices.

- OPEC member Iran’s production, including a reported 40 million barrels stored at sea, could begin to hit the market early next year under the terms of the Iran nuclear pact.

- Demand growth in many emerging markets is slowing.

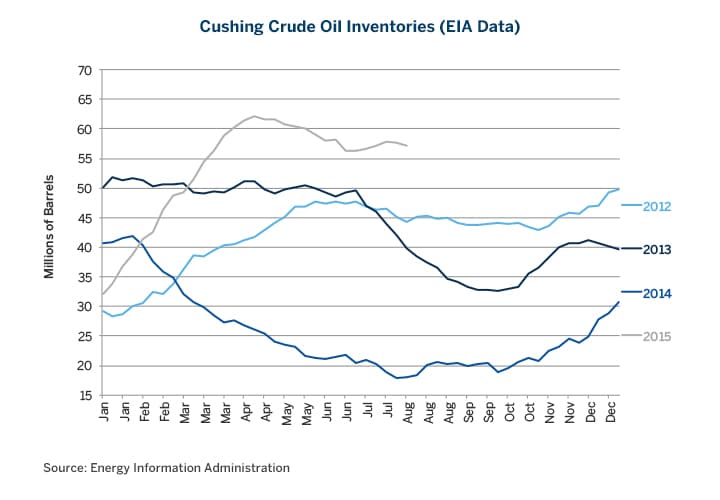

Given the inventory situation, and the potential for slower growth in many emerging markets (China, India, Latin America, the Middle East, and Russia), it would not be surprising to us to see WTI and Brent test and possibly even break their lows from January and March. Cushing crude oil inventory levels continue to remain near the highs despite the strong summer demand (Figure 3).

Figure 3: Cushing Oil Inventories Remain Near Record Highs Despite Strong Summer Demand.

{kind=link}

As such, it’s reasonable to ask what indicators we should look for to know when the price has hit bottom. We see three factors as being key:

- Inventories of crude oil.

- Inventories of products derived from crude oil (gasoline and heating oil).

- The steepness of the oil curve’s contango, and the possibility of a “super-contango.”

Inventories

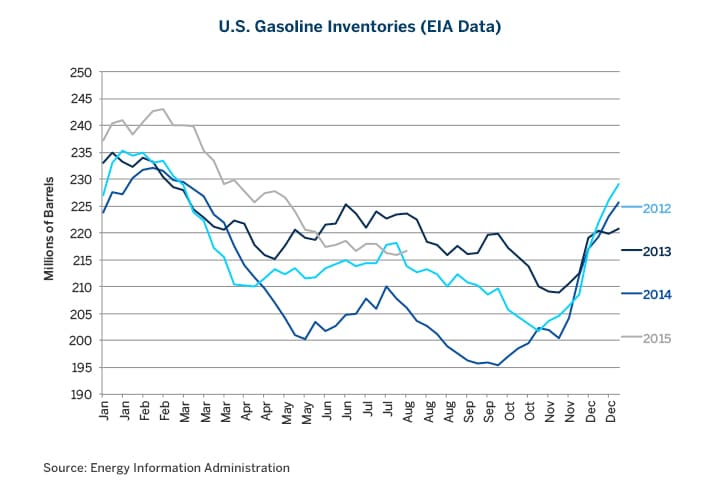

Crude oil inventories are continuing to soar and this is likely to prove bearish for WTI and Brent. The picture for oil products is, however, less clear. Gasoline inventories have been declining as expected during what has been a very active summer driving season. They are closely in line with their July 2014 levels, a bit below their 2013 levels and a bit above their 2012 levels (Figure 4).

Why gasoline inventories have fallen is partly a consequence of Americans driving about 5% more miles than last summer. Another factor is that refining capacity has not expanded in line with oil production. Refiners in the US are operating at close to full capacity (96-98%) yet just keeping pace with the expanded consumption of gasoline. Gasoline production is up about 3.5% year on year, according to the Department of Energy.

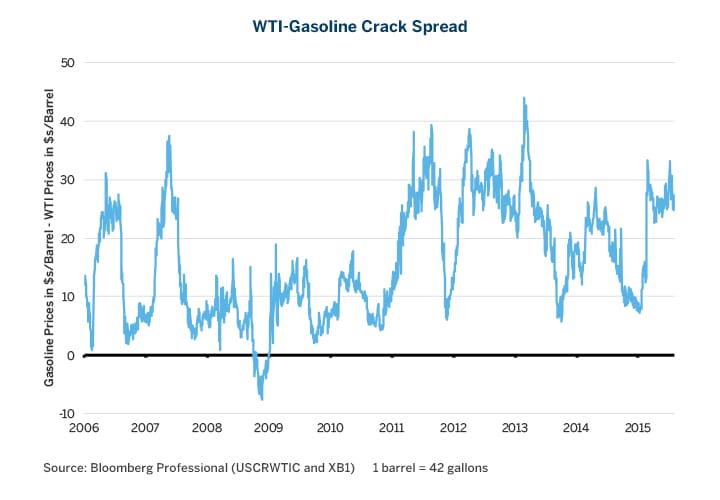

Reasonably low inventory levels of gasoline combined with record high crude oil inventories have translated into a wide crack spread between gasoline and crude oil, and high margins for refiners (Figure 5).

Figure 4: Gasoline Inventories.

{kind=link}

Figure 5: High Margins for Refiners Amid Wide Crack Spreads.

{kind=link}

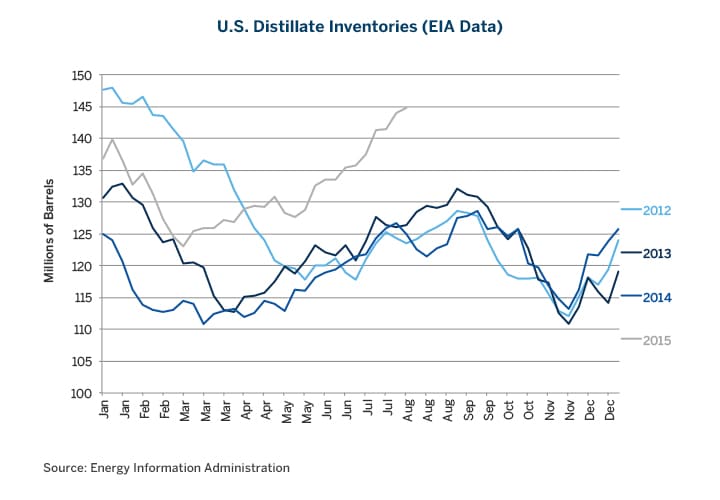

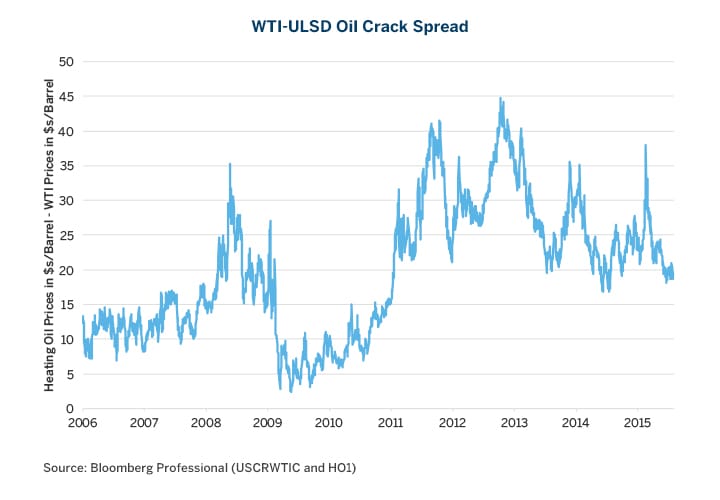

While gasoline inventory levels have been healthy, the level of distillates (mainly heating oil and diesel) is of greater concern. As of mid-July, distillate inventories were 10-15% higher than at a similar point in 2012, 2013, and 2014 (Figure 6). Not surprisingly, this has put downward pressure on the price spread of distillates with respect to crude oil. The NYMEX ULSD crack spread is close to its lowest level since 2011 (Figure 7). An additional source of concern is El Nino, which appears to be strengthening in the Equatorial Pacific. Historically, El Nino has generated warmer-than-normal wintertime temperatures in the Northern US and Canada -- the primary region for heating oil consumption. If winter does turn out to be warmer than normal in the Northern US and Canada, it could be bearish for the spread.

Figure 6: 2015 Mid-July Distillate Levels Higher than in Past Three Years.

{kind=link}

Figure 7: NYMEX ULSD Crack Spread Near its Lowest Level Since 2011.

{kind=link}

The possibility of “super-contango,” and the bottom in crude oil prices

While inventory levels are key to understanding what is happening in the crude oil market, the data has limitations. The fact remains that the US is the only source of up-to-date inventory numbers, which is part of the reason why WTI plays such an important role in the global crude oil market’s price discovery. The rest of the world is comparatively opaque regarding its inventory and production levels.

US inventory numbers aside, one can also look at the degree of contango in the oil market as an indicator of whether or not prices have hit bottom. While there is no guarantee that the eventual bottom in oil will coincide with a steep contango, past bottoms in oil prices do provide some guide.

For example, when oil prices hit bottom in late 2008 and early 2009, the market was in a steep contango (or super-contango) with spreads between some of the monthly contracts exceeding $1. On February 12, 2009, one of the lowest points in crude oil during the past decade, the March 2009 future traded at $33.98/barrel, whereas the March 2010 future traded at $55.95/barrel for a 12-month contango of $21.97. Basically, the market priced (and later got) a V-shaped recovery in oil prices as excess inventory cleared at a low cost, paving the way for higher prices later on.

Currently, the oil curve is much less steep than it was at the bottom in 2009. As of August 3rd, 2015, the August 2015 settlement price was $45.08, whereas the August 2016 contract was at $50.88, with the 12-month contango at $5.80. (Figure 8). This might indicate that oil prices have substantial further downside before supply and demand are brought in line.

However, the fundamental factors underlying the global oil market are different today compared with 2008/2009. While weaker demand growth from emerging markets, including China, as well as more fuel efficient vehicles compound the downward pressure on oil prices, in 2015 it’s mainly a supply issue. Crude oil prices have collapsed mainly because of increasing supply in the US and Saudi Arabia, as well as fears of Iranian supply coming on line. By contrast, in 2008 and 2009 it was more of a demand-destruction story, with demand collapsing amid the financial crisis. This might make contango less reliable of an indicator of a market bottom in 2015 than it was in 2009.

Figure 8: 2015 Oil Curve Less Steep than in 2009.

{kind=link}

Overall, with high inventories, growing supplies, more efficient vehicles, and slowing demand in emerging market economies, the market is not pricing a rebound in oil prices like it did during the 2009 low. This indicates that market participants expect oil prices to remain subdued for a long time, and it might also mean that the market hasn’t yet reached its ultimate bottom.

All examples in this report are hypothetical interpretations of situations and are used for explanation purposes only. The views in this report reflect solely those of the authors and not necessarily those of CME Group or its affiliated institutions. This report and the information herein should not be considered investment advice or the results of actual market experience.

Recommended For You

View this article in PDF format.