{kind=link}

SONIA: High Time to Lower Rates

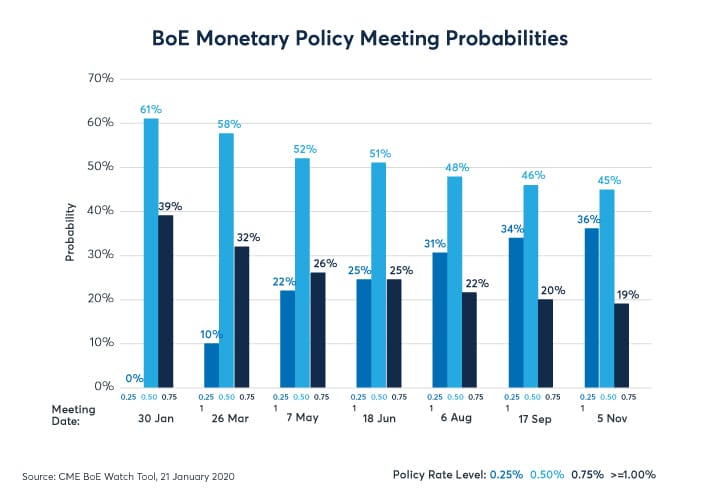

SONIA (Sterling Overnight Index Average) futures are pricing a 61% probability that the Bank of England (BoE) will cut rates at its meeting on January 30th. The probability that the BoE will cut rates at its September meeting jumps to 80% (Figure 1), as of this writing.

Figure 1: 61% chance of a January cut grows to 80% by September, according to CME’s BoE Watch Tool

{kind=link}

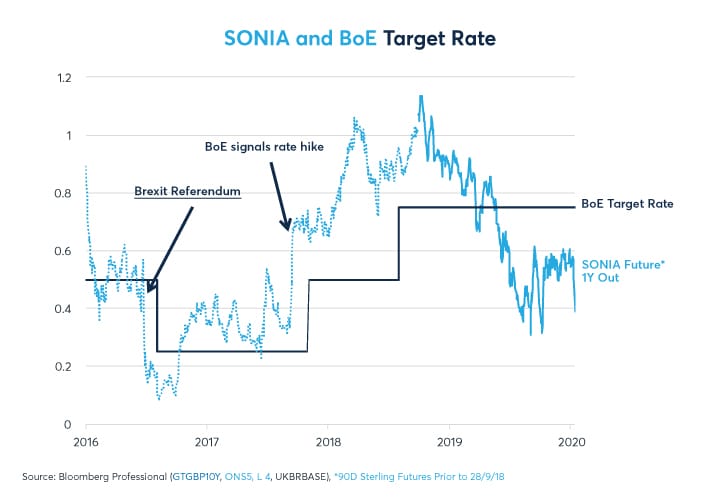

That SONIA is pricing rate cuts is not a new phenomenon. The UK interest rate curve has been pricing that rate cuts are more likely than rate hikes consistently since May 22, 2019 (Figure2). Moreover, the pricing in favor of rate cuts is less extreme now than it was during much of the late summer and early fall of 2019.

At December’s BoE meeting two of nine members voted to cut rates, and at the end of this month it is possible that at least two or possibly more might join their ranks.

Figure 2: SONIA futures have been consistently pricing BoE rate cuts since late-May 2019

{kind=link}

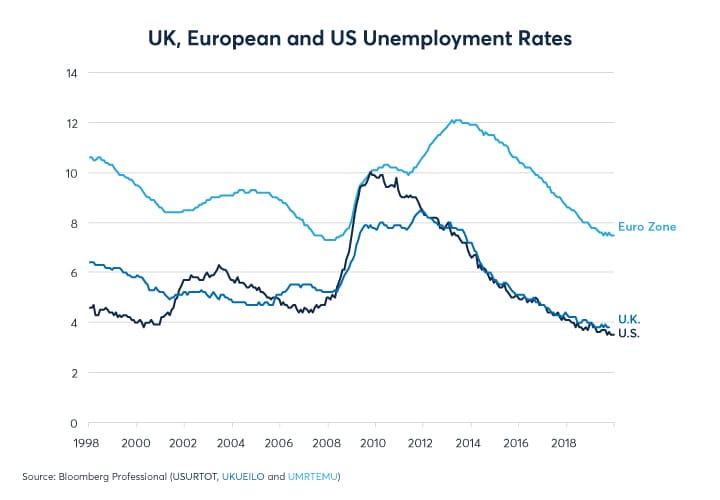

Given that UK unemployment is only 3.8% (Figure 3), discussion of rate cuts might come as a surprise. Like in the US and most of Europe, however, there appears to be no discernable connection between the level of unemployment and the rate of inflation. The UK’s Phillips Curve, which measures the relationship between jobless rates and inflation, has been flat as a pancake (Figure 4).

Figure 3: UK unemployment is at multi-decade lows

{kind=link}

Figure 4: Falling unemployment has not ignited inflation (see appendix for a really weird chart!)

{kind=link}

Moreover, UK core inflation continues to run below 2%, as it has for most of the past 22 years. The only brief exceptions were in 2010 and 2011 when the UK increased the value-added tax from 15% back to 17.5% (where it had been before a temporary reduction during the crisis) and then up to 20%. Steep increases in university fees also boosted inflation during this time. The other time when core inflation exceeded 2% came in the year after the Brexit referendum. That time inflation rates were pushed about 1% higher following the 15% decline in the trade-weighted value of the pound. Those effects quickly faded however as the currency stabilized.

Going into the last elections, economic growth ground to a halt. The manufacturing sector shrank while housing and consumer spending grew at a snail’s pace. There is some anecdotal evidence that a rebound is in store. For example, business confidence soared in the wake of the elections and the government has promised substantial fiscal stimulus. Even so, the BoE takes little risk by cutting rates. Traditionally, the main risk in easing monetary policy would be setting off consumer price inflation or fueling asset bubbles. Neither seems to be a major risk today. Housing prices have been flat overall, falling in London and rising in other parts of the UK. Moreover, it’s hard to believe that lower rates will fuel a bubble in the rather sluggish UK equity market. Consumer price inflation hasn’t been a problem in decades and won’t likely become one because of a quarter-point rate cut.

Figure 5: Except for VAT hikes & post-referendum currency crash, inflation has been low and stable

{kind=link}

Bottom Line

- Pressure is building within the BoE for a rate cut

- SONIA prices a cut with a 61% probability in January and as high as 80% in September

- UK core inflation is stable and slightly below target

- Low rates of unemployment are not creating upward pressure on prices

Appendix

Figure 3.5: Long-term there has actually been a positive relationship between inflation and unemployment because of increases in the VAT and administered prices after the financial crisis

{kind=link}

SONIA futures

Our SONIA futures offer clients expanded efficiencies and support newly created global, transaction-based indices. Sterling-denominated SONIA futures will trade alongside Eurodollar, Fed Fund and SOFR futures, creating new spread trading and margin offset opportunities.

CME BoEWatch Tool

Track the probability of a rate hike at upcoming Bank of England Monetary Policy Committee meetings