{kind=link}

Replicating Swap Spreads with Futures

Spreading Treasury Futures and MAC Swap Futures

While credit risk exposure has traditionally been captured by spreading over-the-counter (OTC) interest rate swaps (IRS) against on-the-run (OTR) U.S. Treasury notes or bonds, the expansion of Exchange listed US Dollar Interest Rate Swap futures (MAC Swap Futures) at the major tenor points of the Treasury yield curve (2-, 5-, 7-, 10-, 20-, 30-Years) has created new opportunities for market participants to futurize credit risk spreads. Among potentially many applications, when they are used in conjunction with Treasury Note futures or Treasury bond futures, MAC Swap Futures provide an alternative, capital- efficient means to acquire or to hedge swap spread exposures. Following a brief overview of MAC Swap Futures, Treasury futures, and Swap Spreads, this note illustrates how.

MAC Swap Future Overview

MAC Swap Futures are contracts for physical delivery of plain-vanilla interest rate swaps (IRS) cleared and guaranteed by CME Clearing. Each contract is for $100,000 notional principal of its deliverable-grade IRS. When a MAC Swap Future for a given delivery month is initially listed for trading, the Exchange assigns a standardizing fixed rate for its delivery-eligible IRS (eg, 0.50%, 0.75%, 1.00%), typically aligned with the corresponding Market Agreed Coupon (MAC) IRS rate recommended by the SIFMA Asset Management Group. (For more about MAC IRS, please visit http://www.sifma.org/services/standard-forms-and-documentation/swaps/ .) Accordingly, any MAC Swap Future’s deliverable-grade IRS has an effective date equal to the third Wednesday (ie, IMM Wednesday) of the MAC Swap Future contract’s delivery month, and pays semiannual fixed interest at its assigned standardized fixed rate per annum in Exchange for quarterly payments of floating interest equal to three-month ICE LIBOR. For more about the structure of MAC Swap Future contracts, please visit http://www.cmegroup.com/trading/interest-rates/deliverable-swaps.html

The buyer of a MAC Swap Future who takes her contract to delivery becomes the receiver of fixed interest (payer of floating) in the delivered IRS. Conversely, upon delivery the holder of short position in a MAC Swap Future becomes the receiver of floating interest (payer of fixed) in the delivered IRS

Exhibit 1 -- MAC Swap Future Nomenclature

| Swap Futures | Deliverable-Grade IRS Exposure |

| Buyer (Long) | Fixed Rate Receiver (Floating Rate Payer) |

| Seller (Short) | Fixed Rate Payer (Floating Rate Receiver) |

A MAC Swap Future contract’s price is quoted as 100 points of par (equal to $1,000 per price point) plus the net present value (NPV) of its deliverable-grade IRS. NPV is equal to the present discounted value of the IRS’s fixed rate payments minus the present discounted projected value of its floating rate payments --

NPV = PV(Fixed rate) – PV(Floating rate)

The NPV is then converted to contract price points and 32nds of price points and added to 100. Because NPV may be either negative or positive, depending on the projected value of floating rate payments relative to fixed rate payments, MAC Swap Future contract prices may be quoted either above or below par. In the hypothetical examples below, NPV is either $33 or -$33 per MAC Swap Future contract. With each 32ndof a contract price point equal to $31.25 (or $1000 per point / 32), the absolute magnitude of NPV in each case is 1.056 / 32nds. Given that contract minimum price increment is set to ½ of 1/32nd (equal to $15.625 per contract) for 7-Year MAC Swap Future and 1/32nd for 20-Year MAC Swap Future, NPV in these cases would be apt to be quoted at the nearest 32nd (Exhibit 2).

Exhibit 2 -- Examples of MAC Swap Future Pricing

| Fixed Rate PV ($) | Floating Rate PV ($) | NPV ($) | Convert to Points & 32nds | Price (Points & 32nds) |

| 300 | 267 | 33 | $33 / ($31.25 per 32nd) | 100-01 |

| 267 | 300 | -33 | -$33 / ($31.25 per 32nd) | 99-31 |

Treasury Futures Overview

Treasury Futures are among the most highly traded of all futures products. Futures delivery months are March, June, September, or December. Each contract is fulfilled by delivery of $100,000 ($200,000 for 2-Year U.S. Treasury Note futures) face value of Treasury notes with various remaining term to maturity (RTM) from the first day of its delivery month, as shown in Exhibit 3.

Exhibit 3 –Treasury Futures RTM

| Treasury Future | Minimum RTM | Maximum RTM |

| 2-Year (TU) | 1-Year 9-Months | 2-Years |

| 5-Year (FV) | 4-Years 2-Months | No more than 5-years 3-Months |

| 10-Year (TY) | 6-Years 6-Months | No more than 10-years |

| Ultra 10-Year (TN) | 9-Years 5-Months | No more than 10-years |

| Classic T-Bond (US) | 15-Years | Less than 25-Years |

| Ultra T-Bond (UB) | 25-Years | 30-Years |

All Treasury Note and Bond futures rely upon a system of delivery invoice conversion factors standardized to a notional yield of 6% per annum. When prevailing market yields are above 6%, consequently, the Treasury issue that is cheapest to deliver (CTD) into an expiring futures contract tends to be the member of the deliverable grade with longest Macauley duration. Conversely, when market yields are below 6%, as at present, the deliverable-grade security with shortest duration tends to be CTD into its corresponding expiring futures contract.

For more about Treasury futures, please visit http://www.cmegroup.com/trading/interest-rates/

Swap Spread Overview

The credit spread between private and public credit risk--represented respectively by the credit risk of banks and the U.S. Treasury--is a market that has traditionally been captured by spreading over–the-counter (OTC) IRS against the on-the-run (most recently issued) cash U.S. Treasury notes and bonds. The swap spread at each tenor is equal to the spot starting swap rate less the yield of an on-the-run U.S. Treasury note of comparable maturity. Typically, a swap spread trade encapsulates an outlook on the expectation of improvement or deterioration in the public and private credit markets, depending on the position of the market participant.

As changes in market structures and banking regulations increase demand for off-balance sheet exposure, liquidity in Treasury futures has grown significantly, rising to levels comparable to cash Treasuries markets. Increasing futures liquidity, coupled with the close relationship between the cash swap spread (OTC IRS rate – OTR Treasury yield) and futurized swap spread (MAC Swap Future – Treasury Future), allows market participants the opportunity to capture cash swap spread exposure by spreading similar MAC Swap Future and Treasury futures.

Exhibit 4 illustrates the current price and yield dynamics of Treasury futures and their corresponding MAC Swap Future contract:

Exhibit 4 – MAC Swap Future vs. Corresponding Treasury Future

| MAC Swap Future | Treasury Future | CTD Tenor |

| 2-Year MAC Swap Future | 2-Year (TU) | 1-Year 9-Months |

| 5-Year MAC Swap Future | 5-Year (FV) | 4-Years 2-Months |

| 7-Year MAC Swap Future | 10-Year (TY) | 6-Years 6-Months |

| 10-Year MAC Swap Future | Ultra 10-Year (TN) | 9-Years 5-Months |

| 20-Year MAC Swap Future | Classic T-Bond (US) | 20 -Years |

| 30-Year MAC Swap Future | Ultra T-Bond (UB) | 25-Years |

It is worth noting that the lack of Treasury bond issuance between 2001 and 2006 leads the US contract to reflect yield and price dynamics in the 20- to 22-year neighborhood of the Treasury yield curve.

The following sections of this note will demonstrate how one could spread Treasury futures and MAC Swap Futures to achieve very similar results to the traditional cash swap spread, while also benefiting from the significant capital savings offered by futures products.

Managing Risk with MAC Swap Futures

Spreading IRS against Treasury securities with comparable underlying terms to maturity is a familiar means of trading the swap spread, ie, the interest rate spread between money center bank credit exposure and US Treasury credit risk. Spreads between MAC Swap Futures and Treasury futures enable users to synthetically acquire or hedge swap spread exposures (or other credit spread exposures that are reasonably correlated with swap spreads).

Exhibit 5 -- Swap Spreads

| Credit Conditions | MAC Swap Futures | Treasury Futures |

| Improving (narrowing swap spreads) | Buy | Sell |

| Deteriorating (widening swap spreads) | Sell | Buy |

In any such instance, the appropriate futures spread ratio is built on the relative interest rate sensitivities of the legs of the spread, ie, the dollar value per futures contract of a one basis point (bp) per annum change in the contract’s respective underlying interest rate exposure (basis point value, or BPV). For example, let BPVTN be the dollar value of change in a TN contract’s price associated with a change of one bp in Treasury yields of the CTD issue, and let BPVMAC Swap Future be the dollar value of change in MAC Swap Future contract price arising from a one bp change in the corresponding delivered IRS fixed rates. The spread ratio between the two, expressed as number of MAC Swap Futures per TN, is:

Spread Ratio = BPVTN / BPVMAC Swap Futures

Spreading TN with 10-Year MAC Swap Futures

The following example demonstrates a TN-MAC Swap Future spread at approximately the 10-Year point. TN is assumed to be for June 2016 delivery (TNM6), for which the cheapest-to-deliver contract-grade Treasury note is assumed to be the 2-1/4% of 15 November 2025 with a conversion factor (CF) of 0.7367 for June 2016 deliveries. For the June 2016 10-year MAC Swap Future (N1UM6) the contract grade is a 10-year plain-vanilla IRS with a fixed rate of 2-1/4 percent per annum for delivery (ie, with a swap effective date) on Wednesday, 15 June 2016 (Exhibit 6).

Exhibit 6 – June 2016 TN, 10-Year MAC Swap Future

| Futures Contract | TNM6 | 10-Yr MAC Swap Future N1UM6 |

| Delivery Date | 30 June 2016 | 15 Jun 2016 |

| CTD Treasury | 2-1/4 of 15 Nov 2025 | |

| CTD CF | 0.7367 | |

| IRS Maturity Date | 15 Jun 2026 | |

| IRS Fixed Rate (%) | 2-1/4 | |

| BPV per Contract ($) | 118.64 | 99.17 |

| Duration (Yrs) | 8.42 | 9.48 |

When assessing the interest rate sensitivity of a Treasury futures contract, a reliable approach is to find the forward BPV of the CTD security (BPVCTD), with the most probable futures delivery date serving as the forward date, then to deflate the result by the corresponding delivery conversion factor. In these examples, taking the premise that the last delivery date (Thursday, 30 June 2016) is the most likely, the forward BPV of the Treasury issue is $87.40 per bp per $100,000 face value. Combining the ingredients gives us $118.64 per bp per contract as the BPV for TNM6:

BPVTN = BPVCTD / CFCTD = $87.40 / 0.7367 = $118.64

Assuming one aims to either shed or acquire swap spread exposure by spreading 10-year MAC Swap Futures against TN, the BPV-weighted spread ratio would be 1.20, or 120 10-year MAC Swap Futures long (short) for every 100 TY contracts short (long) –

BPVTN / BPVN1U = $118.64 / $99.17 = 1.20

While this approach may be adequate for some purposes, the slight difference in tenor of the two legs—9-years 5-months for the Treasury future and 10-years for the MAC Swap Future-- incorporates an element of yield curve exposure in addition to the desired swap spread exposure.

Cash Swap Spread vs Futures Swap Spread

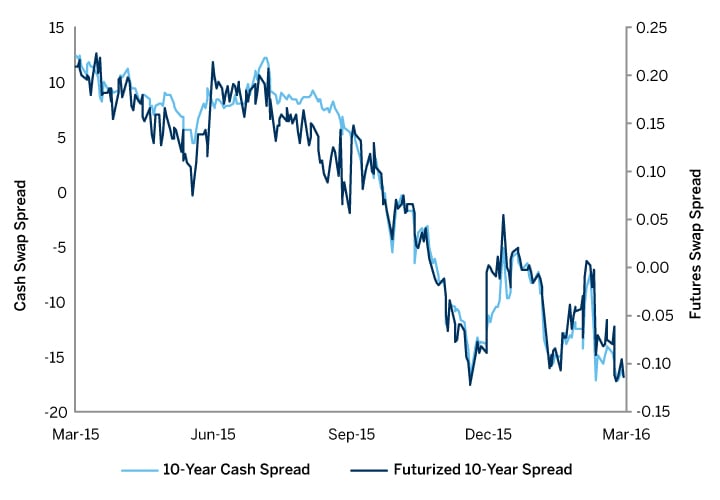

For those firms expressing views on swap spreads, the traditional trading methodology requires combining an OTC spot-starting interest rate swap (IRS) with a Treasury security. With the introduction of MAC Swap Futures, market participants can futurize this spread by combining a deliverable swap future and U.S. Treasury future—achieving closely correlated outcomes with significant capital efficiencies. Exhibit 7 illustrates the close relationship between the futurized 10-year swap spread and the 10-year cash swap spread from March 2015 to March 2016:

Exhibit 7 – Cash Swap Spread vs Futures Swap Spread

{kind=link}

Exhibit 8 details a scenario in which a market participant compares the PnL results of a cash swap spread using 10-year Treasury notes against 10-Year OTC IRS, and a futures swap spread of the 10-Year Treasury note futures (TN) against 10-year MAC Swap Futures:

Exhibit 8 – Cash PnL vs Futures PnL

| Cash Swap Spread | ||||

| Treasury Security Leg | ||||

| Date | Instrument | Face Value | Price/Rate | PnL |

| Mar 28 | T-Note (buy) | $10 Million | 97-20.75 32nds | $48,437 |

| Apr 29 | T-Note (sell) | $10 Million | 98-.25 32nds | |

| Interest Rate Swap Leg | ||||

| Date | Instrument | Notional | Price/Rate | PnL |

| Mar 28 | IRS, Pay Fixed | $9.6 Million | 1.759% | -$52,704 |

| Apr 29 | IRS, Rec Fixed | $9.6 Million | 1.727% | |

| Net Payment | -$4,266 | |||

| Future Swap Spread | ||||

| Treasury Future Leg | ||||

| Date | Instrument | Contracts | Price | PnL |

| Mar 28 | TNM6 (buy) | 73 | 139-21 32nds | $66,156 |

| Apr 29 | TNM6(sell) | 73 | 140-18 32nds | |

| MAC Swap Future Leg | ||||

| Date | Instrument | Contracts | Price/Rate | PnL |

| Mar 28 | N1UM6 (sell) | 89 | 104-7.5 32nds | -$43,109 |

| Apr 29 | N1UM6 (buy) | 89 | 104-23 32nds | |

| Net Payment | $23,046 | |||

Because the resultant net payments of the two types of spreads are closely related, the more advantageous methodology of trading the swap spread can be found in the type of spread that has the higher net payment: capital requirement ratio.

The futurized version of the swap spread (MAC Swap Future and Treasury futures) is created using two contracts traded through, and cleared via, the Exchange. This allows for risk offsets that are applied the moment the positions are cleared—significantly reducing the capital requirements to complete the spread.

The cash efficiencies achieved by utilizing MAC Swap Futures (futurized interest rate exposure) as opposed to IRS (OTC interest rate exposure) are further illustrated in Exhibit 9, which details the margin requirements for the aforementioned products. Exhibit 10 illustrates the percentage margin offset currently offered for MAC Swap Futures and Treasury futures products.

Exhibit 9—IRS vs MAC Swap Future Margin Requirements*

| Instrument | Margin Requirement (per 100k) |

| 2-Year IRS | $565.00 |

| 2-Year MAC Swap Future | $400.00 |

| 5-Year IRS | $1427.00 |

| 5-Year MAC Swap Future | $1000.00 |

| 7-Year IRS | $2217.00 |

| 7-Year MAC Swap Future | $1400.00 |

| 10-Year IRS | $3119.00 |

| 10-Year MAC Swap Future | $1750.00 |

| 20-Year IRS | $6651.00 |

| 20-Year MAC Swap Future | $3400.00 |

| 30-Year IRS | $9607.00 |

| 30-Year MAC Swap Future | $5200.00 |

Exhibit 10—MAC Swap Future and Treasury Offsets*

| TU | FV | TY | US | UB | |

| 2-Year | 70% | 60% | 50% | 0% | 0% |

| 5-Year | 70% | 80% | 70% | 60% | 50% |

| 7-Year | 35% | 70% | 70% | 65% | 55% |

| 10-Year | 0% | 60% | 75% | 70% | 60% |

| 20-Year | 0% | 55% | 65% | 70% | 65% |

| 30-Year | 0% | 50% | 60% | 65% | 70% |

*As of April 7, 2016. For more information on futures margins please visit CME Group Margins

Cash Efficient Hedging

MAC Swap Future contracts offer highly correlated hedging abilities of interest rate risk exposures as OTC IRS, but with significant gains in operational efficiency.

The current methodology for portfolio margining OTC IRS and Treasury futures requires transferring cleared futures positions into cleared OTC swaps margin accounts. While this does not impact overall positions in the IRS or futures trading accounts, it necessitates an additional layer of operational diligence during the end-of-day position management process.

Because MAC Swap Futures are futurized OTC interest rate swaps, there are immediate risk offsets against other interest rate futures held in CME futures position accounts. MAC Swap Futures offer firms that are unwilling or unable to transfer Treasury futures into OTC IRS margin accounts the ability to achieve the cash efficiencies of portfolio margining IRS and Treasury futures without requiring transferring positions between margin accounts. This not only provides a more efficient method for reducing overall margin requirements, but also reduces operational requirements and communication between Clearing Firms and the Exchange during the end-of-day settlement and position management process.

Benefits of Executing in Futures Markets

The benefits of using MAC Swap Futures and Treasury futures to establish swap spread positions include off-balance sheet exposures, counterparty credit risk mitigation, greater capital efficiencies, standardization, and price transparency. Customers can develop opposite long/short positions in MAC Swap Futures and Treasury futures by executing in the transparent, anonymous and liquid markets available on CME Globex or by executing block trades provided that each leg meets its respective minimum size requirement. Additionally, customers may also create equal and opposite MAC Swap Futures and Treasury futures positions by utilizing pre-defined, implied inter-commodity spreads that eliminate risk of legging positions in outright markets.