{kind=link}

Natural Gas: The Bust Within the Boom

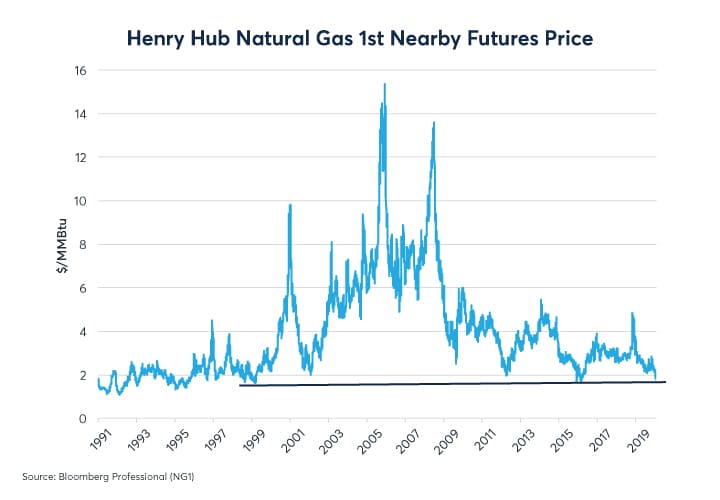

The natural gas market’s bearish sentiment, which put a lid on prices in 2019, has extended to this winter season. The exceptionally mild winter in North America, combined with other bearish fundamentals, have driven prices to nearly four-year lows. (Figure 1).

Figure 1: Natural gas prices are at their lowest in four years

{kind=link}

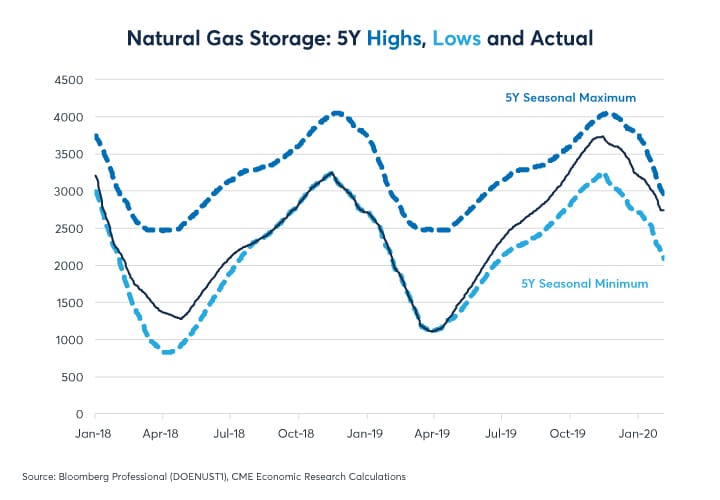

The collapse in natural gas prices sent storage levels to five-year highs (Figure 2). Beyond the weather, there is another reason for the depressed state of affairs: soaring US shale gas production (Figure 3).

Figure 2: Natural gas storage heading towards a five-year high

{kind=link}

Figure 3: Shale gas production continues to soar

{kind=link}

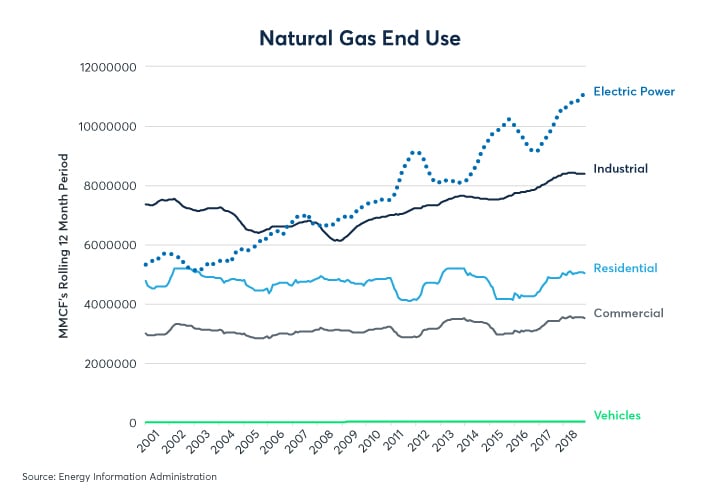

Low natural gas prices have been great news for consumers both in the US and abroad. In the US, there has been a steady increase in the use of natural gas in electrical power generation following more than a decade of depressed prices. Industrial uses have also grown. By contrast, residential and commercial use hasn’t moved much over the past few decades (Figure 4).

Figure 4: Cheap natural gas has shoved coal aside in electrical power generation

{kind=link}

Meanwhile, US exports of natural gas increased to over 4.5 Billion cubic feet (Bcf) per day by mid-2019 , up 37% from the same period in 2018. , Total US LNG export capacity rose from 5.4 billion Bcf per day in June 2019 to 6.1 Bcf by year’s end. By the end of 2020, US LNG export capacity is expected to rise to 8.9 Bcf per day.

Already the impact of US natural gas exports is becoming apparent in global prices. Unlike oil, where the prices between global benchmarks rarely diverge by more than 10-20%, natural gas prices vary significantly by region. From 2010 to -2015, the Asian price of natural gas was typically 350% above the US price while the European price averaged about 125% higher. Since natural gas was historically benchmarked to crude oil, those gaps narrowed somewhat when oil prices collapsed in the late 2014 to early 2016 period. Rising US exports since 2017 have narrowed those gaps. This is especially noticeable during the past year in which Japanese and German natural gas prices followed US prices lower, ignoring the rebound in oil prices (Figure 5). With the US becoming an increasingly prominent exporter of LNG, much of the rest of the world is beginning to look at Henry Hub – the official delivery location of NYMEX futures contracts -- rather than oil benchmarks, as a pricing source for natural gas. A further rise in US LNG exports could shrink natural gas price spreads further.

Figure 5: Soaring US production & US LNG exports are narrowing global price gaps

{kind=link}

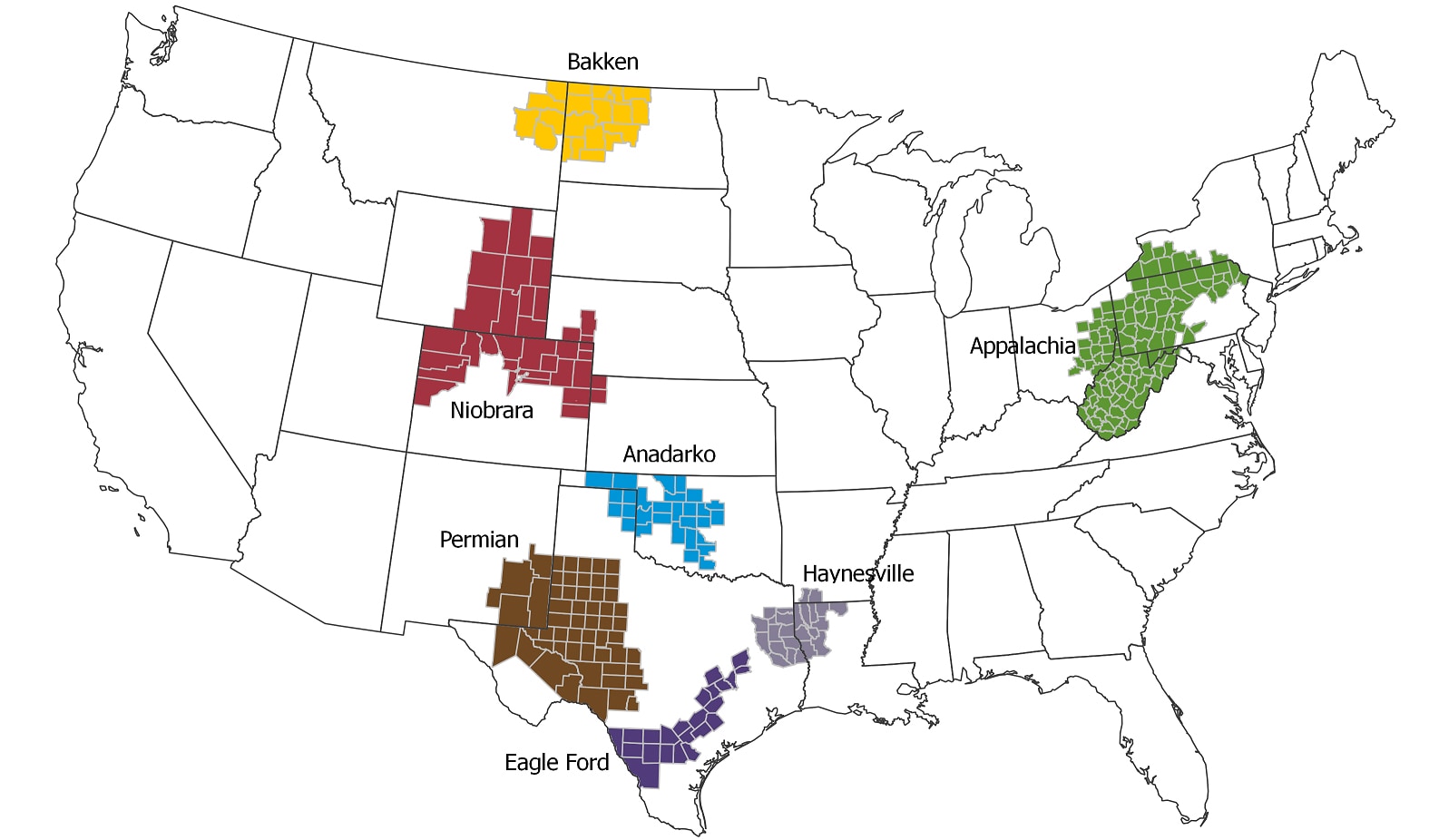

While the low prices have been great news for consumers around the world, they are taking their toll on the shale producers that have driven the boom. Shale production comes from seven major regions in the US (Figure 6) of which Appalachia, Permian and Haynesville are the most prominent (Figure 7).

Figure 6: US shale producing regions

{kind=link}

Figure 7: Appalachia, Haynesville and the Permian have driven natural gas supply growth

{kind=link}

In Appalachia and Haynesville, production is centered around natural gas whereas in the Permian and the other regions it is focused around oil with natural gas as a byproduct. Appalachian production growth slowed significantly in 2019 while it continued to rise steadily in the Permian and in Haynesville.

What all seven regions have in common is dwindling capital investment, resulting in rig counts plummeting. Between April and December 2019, the number of operating rigs in Appalachia dropped from 81 to 50, and from 63 to 52 in Haynesville. Between February and December 2019, the number of rigs in the Permian fell from 485 to 402. Rig counts in the smaller regions have declined even more steeply (Figure 8). Presumably, the recent natural gas sell off will put even further downward pressure on rig counts in Appalachia and Haynesville while the inability of WTI crude oil to sustain a rally even in the face of increased tensions in the Middle East will likely have a similar impact on investment in the other regions.

Figure 8: Rig counts are collapsing in all seven regions as firms slash capex and exploration

{kind=link}

The bearish environment continues to exert additional pressure on the exploration and production sector, which has been suffering from falling revenues and tight cash flows. Producers have been trying to navigate through the murky waters by pursuing different restructuring strategies depending on the size and health of their balance sheets. Some of them have relied on raising capital through debt. Unfortunately, the low-price environment has eroded equity valuations, amplifying the problem of holding uneconomic assets and pushing some companies to write-offs, fire sales, financial distress and even bankruptcies.

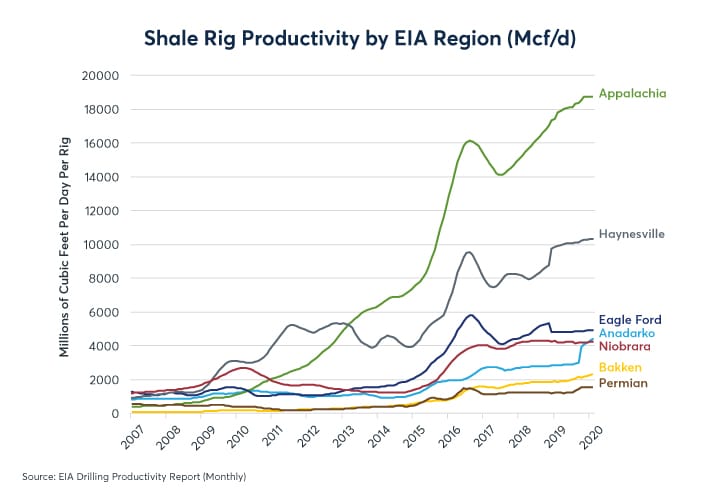

For the moment, the decline in capital expenditure (capex) has had little impact upon production amid soaring productivity per rig (Figure 9). Soaring per-rig-productivity, however, provides a distorted picture of where US natural gas production is heading. If one takes all of the exploratory rigs off line, the rig count declines while production continues apace from rigs that have already been successfully deployed. The average shale play, however, lasts for only 18-24 months. Eventually per-rig productivity could begin to decline. If that happens, the combination of low rig counts and falling productivity could cause US oil and natural gas production to begin to fall. Falling US production could, in turn, reduce storage levels and allow prices to drift higher. Even if prices go somewhat higher, however, the gap between US and global prices will remain significant and US LNG exports will likely to continue to rise.

Figure 9: The decline in exploration has sent per rig productivity higher but that can’t last forever

{kind=link}

Energy Products

See what is making headlines and moving the energy markets. Benefit from trading on NYMEX, the most extensive and liquid Energy marketplace, with an unrivaled product suite and flexible market access.