{kind=link}

Is Gold About to Outperform Equities?

Investors don’t normally think about equity prices as exchange rates, but in a sense, they are: when one sells or buys stocks, one either raises cash or pays cash in a fiat currency. The S&P 500®, for example, can be thought of as the exchange rate between the shares of the companies in that index and the US dollar (USD). Although equity markets have been susceptible to enormous bear markets when viewed in USD terms (down 89% between 1929-33, -47% in 1973-74, -50% in 2000-02 and -60% in 2007-09), for the most part, equities go higher when seen in fiat currency terms.

The general tendency of equity markets to rise results in part from the considerable value that private sector corporations, in aggregate, generate for their shareholders over time. The tendency of stocks to rise in value in fiat currency terms is helped by the steady erosion of the currencies themselves. Even at a 2% rate of inflation, the value of the currency will halve in 35 years, which should double the value of an equity index expressed in that currency, even if corporations collectively add no real value for their shareholders. And, in the past, inflation rates have often exceeded 2%.

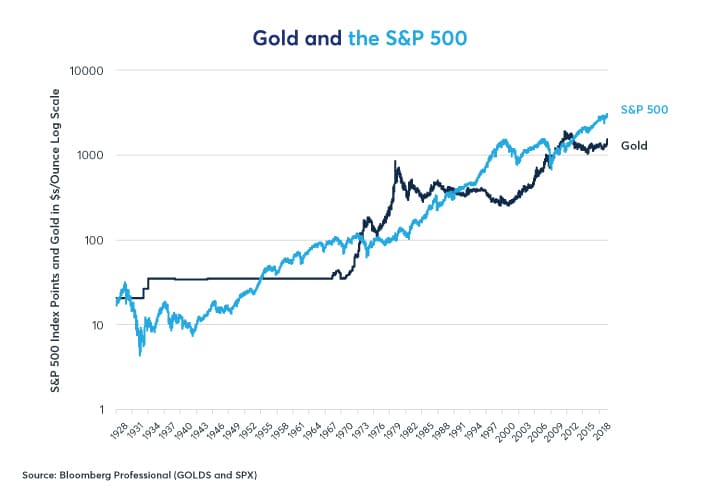

So, what happens when you revalue equities in a non-fiat currency like gold? Ignoring dividends, the S&P 500® and gold have produced similar price returns over the past 90 years (Figure 1). On average, equities have produced only 0.96% better price gain per annum than gold since 1928. With dividends, the outperformance of equities improves to 4.84% per year, on average. The current S&P 500® dividend yield, however, is just 1.91% – about half its historical average.

Figure 1: Gold/Stocks Get Similar Price Returns Over Time but Stocks Pay Dividends, Gold Doesn’t.

{kind=link}

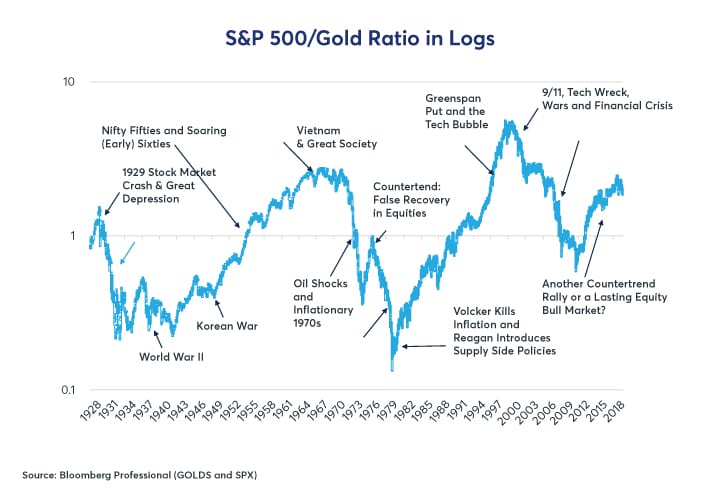

Redenominated in gold terms, the S&P 500® still achieves a positive performance, but that performance is erratic (Figure 2).

- Between January 1928 and September 3, 1929, stocks outperformed gold by 86%.

- Between 1929 and 1942, equities underperformed gold by 86% as stocks fell and gold was repegged from $23 to $35/ounce during the 1933 dollar devaluation.

- From 1942 to 1967, stocks outperformed gold (still pegged at $35/ounce) by 1,135%.

- Between 1967 and 1980, the US went completely off the gold standard, sending gold soaring as stocks collapsed in real terms, falling 95% versus the yellow metal.

- Crippling inflation generated an equity bull market and a collapse in gold prices that lasted 20 years from 1980 until 2000. During this time, the S&P 500® outperformed gold by 3,220%.

- From 2000 to 2011, gold soared and equities underperformed, falling 89% in gold terms.

- Between September 2011 and September 2018, stocks rebounded by 315% versus gold but have fallen back by 24% since, in gold terms, in the past year.

Figure 2: Re-Denominated on Gold Terms, the S&P 500® Achieves Erratic Returns.

{kind=link}

Will the equity markets’ relative outperformance versus gold since 2011 continue? Or is the equity market’s seven-year-long rebound from September 2011 to September 2018 a countertrend rally, sort of like an extended version of the one in 1975 and 1976 when stocks rebounded for a time until the other shoe dropped at the end of the 1970s? The answer to that question depends on several different factors including:

- Economic fundamentals: will they favor gold or equity investments?

- Valuation: are equity markets overvalued or undervalued?

- Geopolitics: US weakness and global chaos favors gold; US strength and global stability favor equities.

When it comes to economic fundamentals, the world could hardly look more different today than it did in the late 1970s. Then, central banks had trouble controlling consumer price inflation. Today, they have trouble generating consumer price inflation. Then, demand often outstripped supply for consumer goods; today production capacity often exceeds demand. However, that doesn’t mean that central banks don’t generate inflation at all when they lower interest rates and print money in quantitative easing (QE) operations. It’s just that now they generate a great deal of asset-price inflation and virtually no consumer-price inflation.

Although official measures of US consumer price inflation have been stable in the US since 1993 at around 2% per annum (with modest variations), that didn’t prevent gold from soaring from $280/ounce to $1,900 between 2000 and 2011, boosted, in part, by the decline in US interest rates from 6.5% to 0.125% and QE programs.

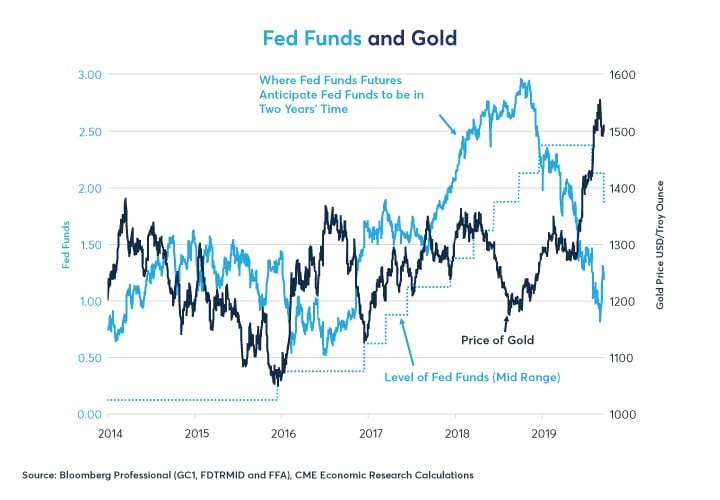

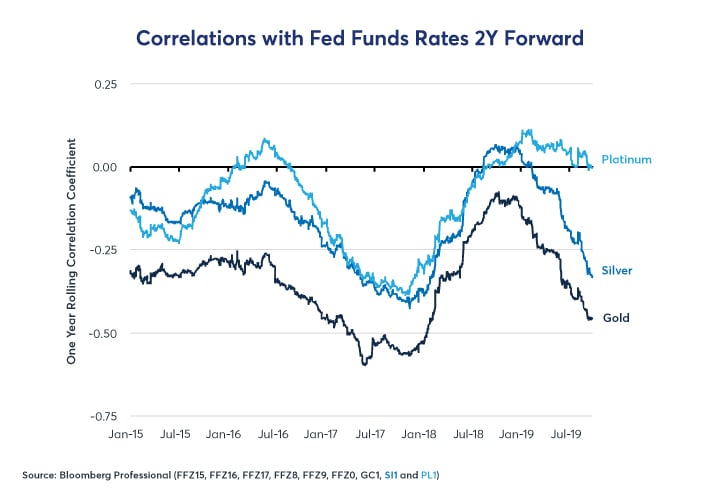

After lagging for years in the face of US monetary tightening, once again, gold has responded favorably to expectations that the Federal Reserve (Fed) will cut rates (and actually cutting rates) (Figure 3). This is not surprising given that gold has a long-term negative correlation with the movements of Fed fund futures, expressed in rate terms (Figure 4). As investors came to expect more Fed rate cuts, the price of gold soared until investors reigned in some of their expectations at the end of the summer and the advance in gold prices halted, at least temporarily.

Figure 3: Gold Prices Often Move in the Opposite Direction of Expectations for Fed Rates.

{kind=link}

Figure 4: Gold Exhibits a Consistent Negative Correlation With 2Y Expectations for Fed Funds.

{kind=link}

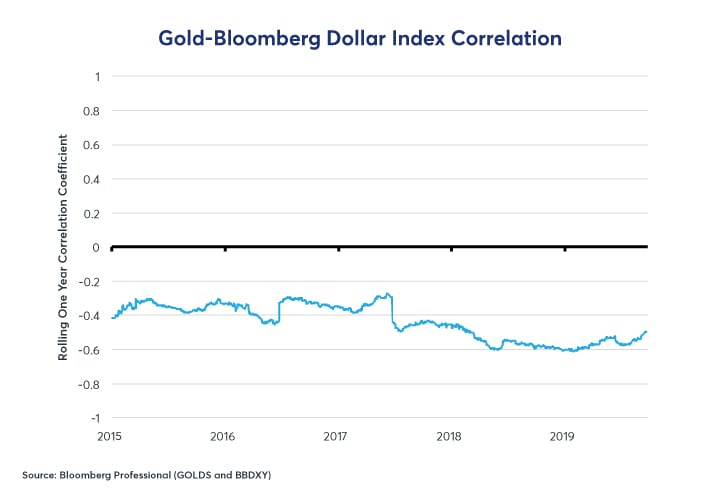

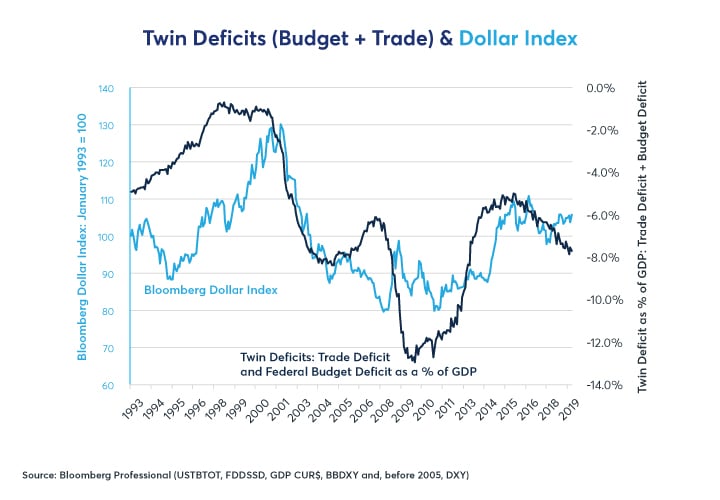

The other, even stronger factor that drives gold prices is the value of USD. Gold has a consistent and strong negative correlation with the Bloomberg Dollar Index (Figure 5). USD rose versus a basket of other currencies between 2011 and 2018, contributing to the bear market in gold. What happens to USD next depends a great deal on US fiscal and monetary policy. For the past several decades, when the US twin deficits (budget + trade) expanded, USD weakened. When those deficits get smaller, USD tends to rally (Figure 6).

Figure 5: Gold Has an Even Stronger and More Consistent Negative Correlation With Dollar Index.

{kind=link}

Figure 6: Expanding US Budget And Trade Deficits Might Herald a Weaker Dollar, Higher Gold.

{kind=link}

US deficits have exploded since 2017, with the budget deficit rising from 2.2% to 4.7% of GDP, and the trade deficit rising slightly as well. What’s truly remarkable about the expansion of US deficits is that they have grown even as unemployment has fallen to 50-year lows. Normally, deficits shrink when unemployment falls but the 2018 tax cut did not pay for itself. Corporate tax revenue plunged as the tax rate was lowered from 35% to 21% but no meaningful loopholes were closed and little money was repatriated from abroad. If Fed’s 2016-18 tightening cycle and the trade war generate a sharp slowdown in growth or an economic downturn, the deficits could rise further. Moreover, with the Fed now easing rather than tightening policy, the possibility of a USD bear market are growing, which could be extremely bullish for gold should it occur. But a looming trade war with Europe might hit the euro.

The economics of the equity market are complicated, and we will cover them in a separate paper but basically there are several reasons (widening credit spreads, rising volatility, falling earnings, underperforming small caps, a narrowing rally) why we think that equities might be in the later stages of a bull market. That bull market could still be a long way from its eventual peak but on a relative basis gold doesn’t look unattractive compared to stocks.

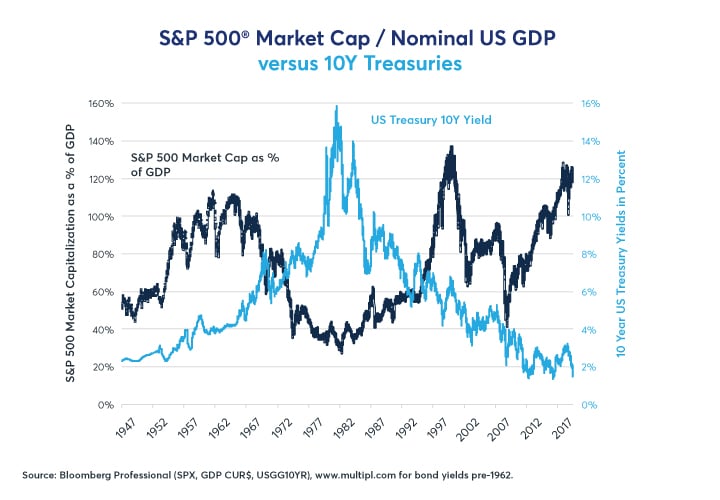

This brings us to the thorny question of the equity market’s valuation. At one level stocks look expensive. The S&P 500®’s market cap relative to GDP is well over 120% and has only been at similar levels once before since 1945. That was in 2000, on the eve of the twin 50% and 60% bear markets and a massive 500% rally in gold. On the other hand, interest rates are one third of what they were in 2000. Presumably, lower interest rates can allow the equity market to sustain much higher levels of valuation than was the case when future earnings and dividends had to be discounted at much higher rates (Figure 7). So, maybe stocks aren’t overvalued given the low yield environment. It could also be that with extremely low interest rates, both stock and bonds are both overvalued and, if that’s true, gold could become an extremely attractive alternative to equity and fixed income.

Figure 7: Overvalued or Undervalued? Hard to Say with Certainty but Certainly Not Inexpensive.

{kind=link}

Lastly, there is the question of geopolitics. Gold outperforms during periods of instability; equities outperform during periods of stability. Equities did terribly during the 1930s as militarily aggressive fascist regimes took hold in Germany and Japan while the US, under pressure from groups like The America First Committee, isolated itself on the other side of the Atlantic with the Roosevelt Administration’s hands largely tied until Pearl Harbor. Between 1942, when the Allies turned the tide in World War II, and the mid-1960s, when stocks soared as the US forged a new, global economic order, Western Europe and Japan recovered.

By the end of the 1960s, however, the combination of the Great Society domestic spending and the cost of the Vietnam War made it impossible for the US to maintain a peg of $35 dollars per ounce of gold, leading President Nixon to devalue the currency. Stagflation, the US retreat from Vietnam and Watergate created the impression that the US was weak. In 1973, Arab governments, taking advantage of Washington’s perceived weakness, reduced oil exports. Stocks collapsed and gold prices soared. Markets normalized a little in the two years after Watergate, but by 1977 the Carter Presidency, with its hesitant foreign policy, did not reassure investors. The 1979 Iranian Revolution and subsequent hostage crisis along with the Soviet invasion of Afghanistan later that year created the impression of a United States on its heels faced with aggressive foreign adversaries. Gold prices rose from $150 per ounce to over $800 as equity markets did nothing in nominal terms and saw their value substantially eroded in real terms.

During the 1980s with Reagan’s robust foreign policy and Fed Chairman Paul Volcker’s commitment to fighting inflation, gold prices crashed and stocks soared. This pattern of falling gold prices and soaring stocks continued throughout the post-Cold War Pax-Americana decade of the 1990s. The 1991 Gulf War was quickly resolved and left the world with the impression of overwhelming US military superiority.

Only after 9/11, the subsequent US invasions of Afghanistan and Iraq, both of which quickly turned into costly quagmires, did stocks begin to fall versus gold. Between 2011 and 2018, the US wound down its involvement in Iraq and returned to a less aggressive foreign policy. Markets showed little reaction to Russia’s invasion of Crimea and the world order didn’t change much under the Obama Presidency.

One question that investors need to ask themselves when valuing gold versus equities is whether that’s the geopolitical environment we find ourselves in now? Is the US more authoritative and more respected in the world or less? Will the Sino-US trade war and the decision to pull out of the Iran nuclear agreement enhance or detract from global stability? Are the US’s traditional alliances with its fellow NATO nations as well as Asian allies like South Korea and Japan becoming stronger or weaker? If investors come to believe that the world is trending towards greater instability, this could prove detrimental to equity prices and potentially quite bullish for gold.

Bottom Line

- The S&P 500 has been on a wild 90 year-long ride versus gold.

- Between 2011 and 2018, stocks outperformed gold but in the last year trend started to go back the other way.

- Fed monetary policy and the US fiscal policy have a strong influence on USD and gold.

- The question of whether stocks are overvalued is thorny and difficult to answer but may favor gold.

- If global instability grows, it may also favor gold.

Shanghai Gold futures

In Q4 2019, we will launch two financially settled Shanghai Gold futures, denominated in U.S. dollar or Chinese renminbi. Shanghai Gold futures will be a product offering based on the regional gold benchmark price from the Shanghai Gold Exchange (SGE).