{kind=link}

Iron Ore & Copper: Prospects and Pitfalls

Iron Ore & Copper: Prospects Tied to China, Brazil & Australia

After rallying 70% between December 2015 and April 2016, iron ore has joined copper in trading sideways. Both metals have suffered from grueling bear markets after setting their peaks in late 2010 and early 2011.

Iron ore was the harder hit of the two, trading at about one-third of its peak value, while copper is trading just below half its peak levels (Figure 1). Iron ore and copper are under pressure from both supply and demand. The lack of a rebound in iron ore prices, in particular, has significant consequences for Australia and Brazil, the metal’s two biggest exporters.

Figure 1: Iron Ore Has Been Much More Volatile Than Copper the Past Two Years.

{kind=link}

Iron ore constitutes 25% of Australia’s exports, equivalent to 5% of GDP, while the metal accounts for 12% of Brazil’s exports, which amounts to nearly 2% of GDP. No wonder both countries’ currencies move in tandem with iron ore prices (Figures 2 and 3).

Figure 2: Iron Ore Could Influence the Australian Dollar/U.S. Dollar Cross-Rate.

{kind=link}

Figure 3: Iron Ore Correlates Positively with the Brazilian Real.

{kind=link}

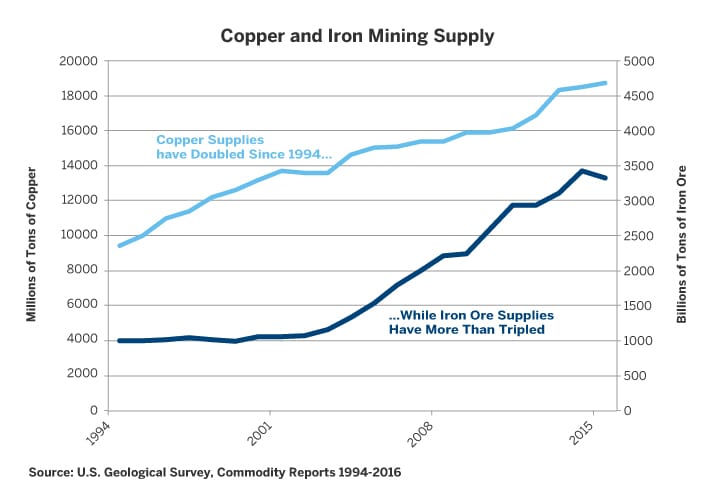

There appear to be two factors preventing a sustained rebound in either metal: supply and China. Iron ore supplies have grown much more quickly than almost any other metal.

Iron ore mining supply has tripled since 2002, while copper mining supply has risen by only 37.5% over the same period. While iron ore mining supply did fall by 2.9% in 2015, it is coming off very high levels, and 2015 production was still the second highest on record (Figure 4). The market for iron ore is still vastly oversupplied. Meanwhile, copper supplies have continued to grow as well.

Figure 4: Growth in Mining Supply of Iron Ore has Vastly Outpaced Copper.

{kind=link}

Iron ore producers ramped up their production mainly to meet demand from China. Unlike the United States, Japan and Western Europe, which meet most of their steel needs using recycled scrap, China relies largely on newly-made steel to meet its infrastructure needs. China has little in the way of recyclable steel from used automobiles and demolished buildings. China consumes 40-50% of most industrial metals, including copper, but in the past several years it has been using close to two thirds of the world’s supply of iron ore. While China is the world’s largest producer of iron ore, it still imports 25% of world production, mainly from Australia and Brazil. This makes iron ore, as well as the Australian and Brazilian economies, exceptionally sensitive to economic developments in China.

While China’s economic growth rate appears to be stabilizing after a long period of consistent slowing, it’s not clear that it can absorb enough of the still substantial supply of copper and iron ore to prevent prices from retesting recent lows.

Of particular concern is China’s soaring debt levels. Relative to GDP, China’s total level of debt (public + private) rose from below 150% of GDP in 2008 to over 255% of GDP by early 2016 as a result of China’s policy of encouraging its non-financial corporate sector to borrow and invest money in the wake of the 2008 financial crisis (Figure 5). China’s debt levels have now attained levels similar to those at which Japan (1990), the Eurozone and the United States (2007 and 2008) began their respective debt crises.

Figure 5: China’s Total Debt to GDP is 254.7%, Near Where Crises in U.S., Europe & Japan Began.

{kind=link}

When debt levels are low, accumulating additional credit adds quickly to GDP. When one person or entity borrows, their spending or investment becomes income for another person or entity, adding to economic output. When debt levels become relatively high, however, additional borrowing adds little to GDP as the new loans serve mainly to refinance existing debt.

As debt accumulated, China’s economy slowed considerably (Figure 6). Accelerating the pace of debt accumulation could stabilize the growth rate in the short term but only at a long-term cost of a potentially deeper economic downturn or longer period of slow growth. American, European and Japanese officials have found that fiscal and monetary stimuli are less effective with high levels of debt.

Figure 6: As Debt Grew, Chinese Economic Growth Slowed.

{kind=link}

So what does the sideways price action of copper and iron ore tell us about the Chinese economy? It’s a difficult question to answer with certainty, since copper and iron ore prices are governed by many factors, including supply, inventories and demand elsewhere in the world. That said, the sideways price action might be telling us that China’s economic growth rate is, in fact, not rebounding very much even in the face of stimulus measures designed to boost growth.

If iron ore prices resume their decline and if China’s economy does not rebound as hoped, this could be bad news for many commodity exporting nations, not least of all Australia and Brazil. Copper may have better sources of alternative demand than iron ore and has seen less supply growth than iron ore over the past decade. Critical to copper’s future will be demand for housing in the United States which has been rebounding very slowly but might get a boost from improved labor market conditions and continued low mortgage rates.

Recommended For You

View this article in PDF format.