{kind=link}

Hedging Portfolio with Commodity Currencies

Investors who wish to gain exposure to commodities can do so directly through futures, options and other derivatives; or indirectly, and perhaps unintentionally, through the currencies of commodity exporting nations. The Australian dollar (AUD), Canadian dollar (CAD), Brazilian real (BRL), Mexican peso (MXN), Russian ruble (RUB) and the South African rand (ZAR) demonstrate positive and, at times, reasonably strong correlations to a large basket of commodities. (Figure 1).

Figure 1: Correlations Between Commodities and Commodity Currencies.

| Correlation Coefficients | AUD | CAD | BRL | MXN | RUB | ZAR |

| West Texas Intermediate Crude Oil | 0.3 | 0.53 | 0.26 | 0.39 | 0.52 | 0.34 |

| Ultra Low Sulfur Diesel | 0.29 | 0.49 | 0.26 | 0.35 | 0.47 | 0.29 |

| Gasoline | 0.25 | 0.39 | 0.22 | 0.3 | 0.42 | 0.22 |

| Gold | 0.25 | 0.25 | 0.13 | 0.04 | 0.06 | 0.25 |

| Silver | 0.32 | 0.33 | 0.22 | 0.13 | 0.18 | 0.31 |

| Platinum | 0.33 | 0.34 | 0.25 | 0.19 | 0.17 | 0.39 |

| Palladium | 0.28 | 0.29 | 0.2 | 0.17 | 0.19 | 0.3 |

| High Grade Copper | 0.31 | 0.29 | 0.16 | 0.15 | 0.19 | 0.25 |

| Iron Ore | 0.14 | 0.15 | 0.14 | 0.16 | 0.11 | 0.13 |

| Corn | 0.16 | 0.18 | 0.19 | 0.18 | 0.11 | 0.16 |

| Soybeans | 0.12 | 0.13 | 0.14 | 0.11 | 0 | 0.12 |

| Wheat | 0.17 | 0.11 | 0.08 | 0.07 | 0.08 | 0.17 |

| Lumber | 0.11 | 0.1 | 0.11 | 0.06 | 0.1 | 0.09 |

Source: Bloomberg Professional (AD1, CD1, BR1, PE1, RU1, RA, SIR1, CL1, HO1, XB1, GC1, SI1, PL1, PA1, HG1, C 1, S 1 W 1, TIO1 and LB1), CME Economic Research Calculations

These correlations offer opportunities for investors who have exposure to either currencies or commodities. For example, one could take a position in a commodity and potentially reduce portfolio risk by taking an opposite position in a positively-correlated currency (Figures 2-5). What makes this even more interesting is the chasm between the carry in currencies and commodities. Some currencies, notably those of emerging markets, exhibit positive interest rate carry versus the U.S. dollar (USD) and other developed market currencies. By contrast, certain commodities exhibit negative carry when they are in contango (when prices in the future are above current levels), a situation that persists much of the time. Essentially, holders of emerging market currencies usually receive an interest rate premium while holders of commodities most often pay storage, insurance, interest and incidental costs.

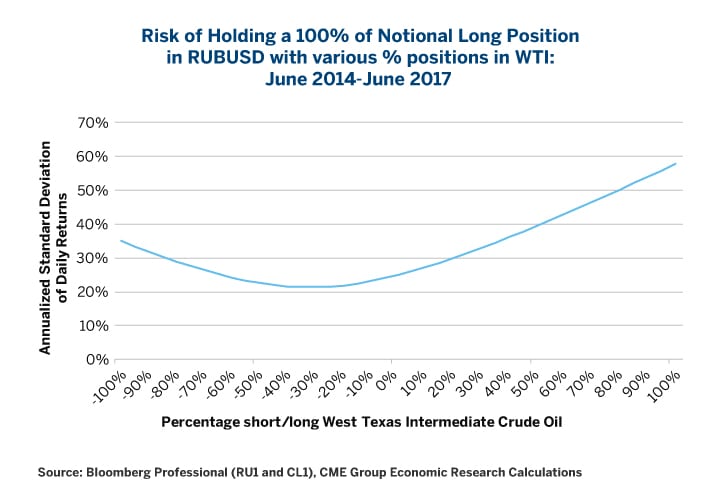

Figure 2: A 30% WTI Short Would Have Minimized Risk from a 100% RUBUSD Long the Past 3 years.

{kind=link}

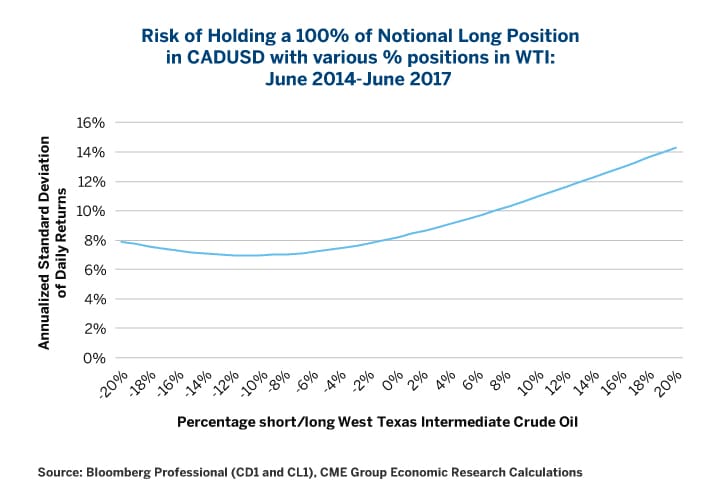

Figure 3: A 10% WTI Short Would Have Minimized Risk From a 100% CADUSD Long the Past 3 Years.

{kind=link}

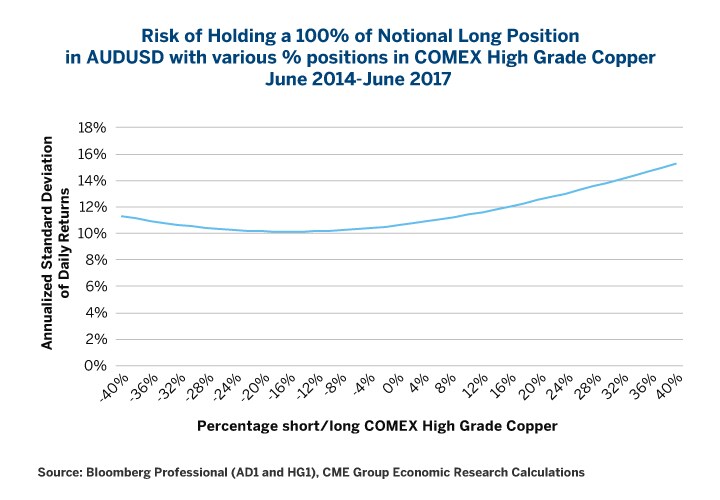

Figure 4: A 15% Copper Short Would Have Minimized Risk From a 100% AUDUSD Long the Past 3 Years.

{kind=link}

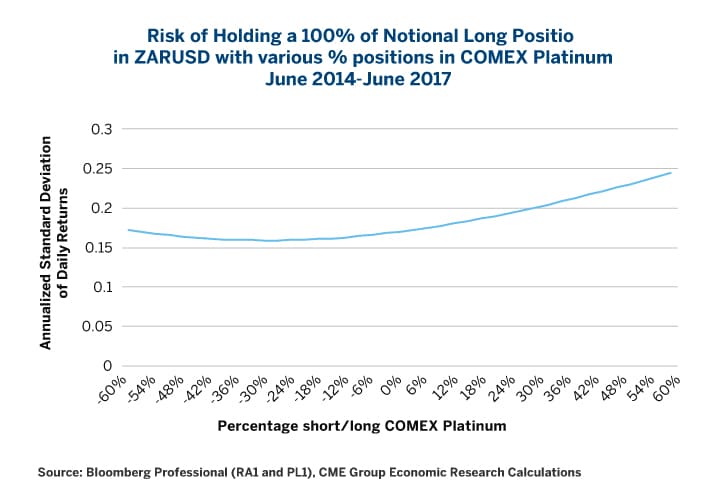

Figure 5: A 15% Platinum Short Would Have Minimized Risk From a 100% ZARUSD Long the past 3 Years.

{kind=link}

FX Carry

Calculating currency carry is simple: it’s essentially the interest rate differential between two currencies that accrues over time. Almost all emerging market currencies pay more in interest rates than the U.S. dollar (USD), giving them a positive carry. Positive carry enhances the upside return on upward moves in the spot currency, while buffering losses on downside moves. The ruble is a great case in point: it has fallen 60% versus the USD in spot terms over the past decade, but with the carry reinvested, it has only fallen by about 10% (Figure 6).

Figure 6: The Ruble Benefits from Strongly Positive Carry Versus Reserve Currencies Like USD.

{kind=link}

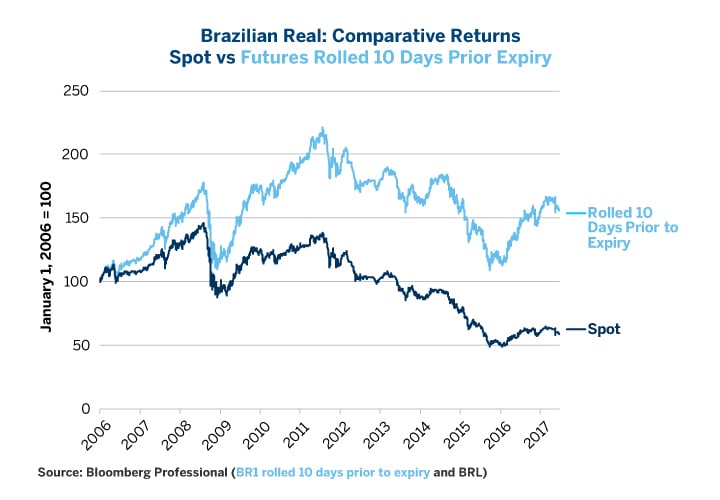

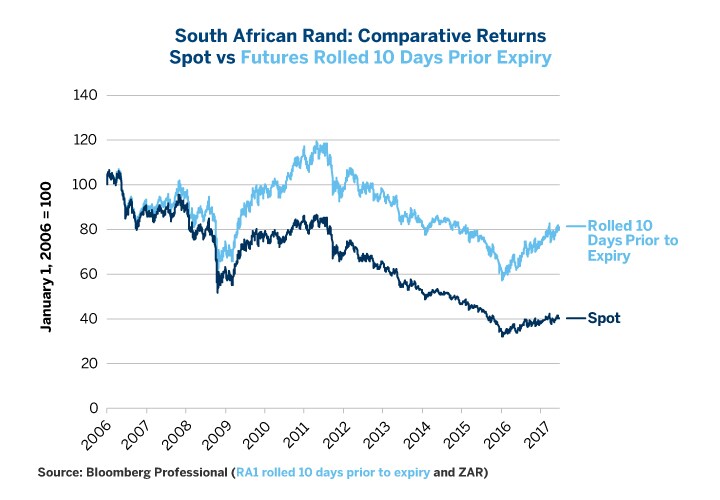

It’s an even more dramatic story for the Brazilian real: it has fallen by about 45% over the past decade in spots terms but has risen by more than 50% when accounting for currency carry (Figure 7). In a similar vein, the South African rand’s (ZAR) spot rate has fallen by 60% versus USD since 2006, but an investor who remained long futures or invested ZAR in an interest-bearing account would have only lost 20% over the same period (Figure 8).

Figure 7: Brazilian Real Carry Has Obliterated Spot Losses Since 2006.

{kind=link}

Figure 8: Rand carry has absorbed two-thirds of the spot losses since 2006.

{kind=link}

For other currencies, the story is less dramatic. In the spot market, the Mexican peso would have lost about half of its value since 2006, but an investor who owned the Mexican peso and received Mexican deposit rates while paying U.S. deposit rates would have lost only 20% over the same period (Figure 9).

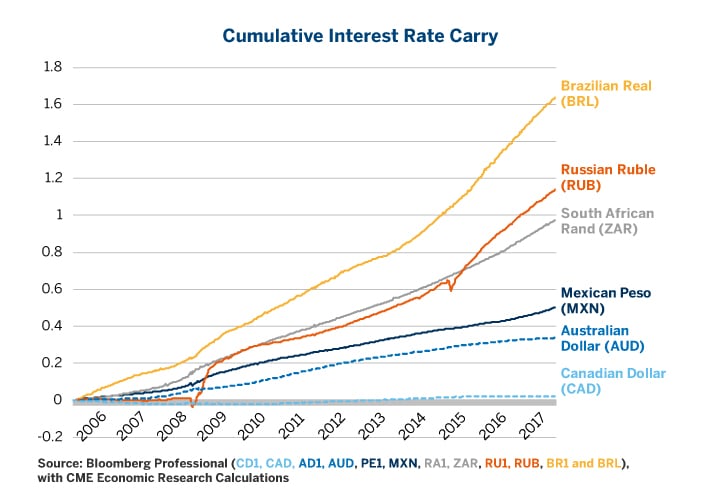

Interest rate differentials between USD, AUD and CAD are much smaller. U.S. rates are now above Canadian rates and may soon be above those in Australia. That means that CAD carry is negative versus USD at the moment and barely positive for AUD. As such, one doesn’t get much of a buffer in the event that AUD or CAD fall in value versus USD, nor if they rise (Figure 10).

Figure 9: Peso Carry Has Absorbed 60% of Spot Market Losses.

{kind=link}

Figure 10: Cumulative Interest Rate Carry on Various Commodity Exporting Currencies.

{kind=link}

Negative Carry in Commodity Markets

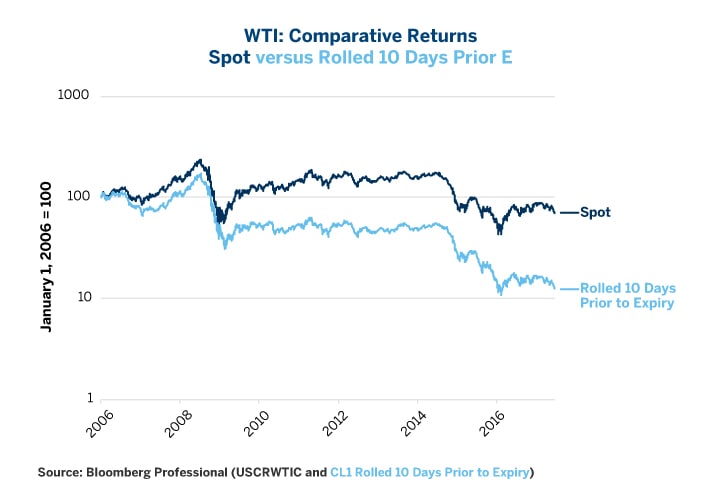

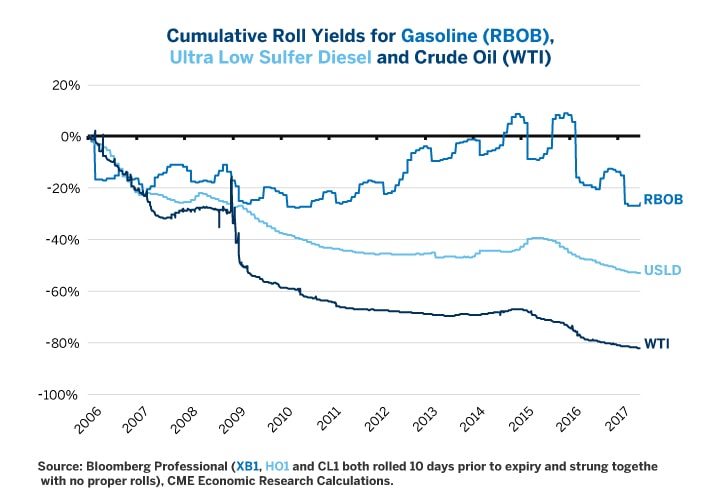

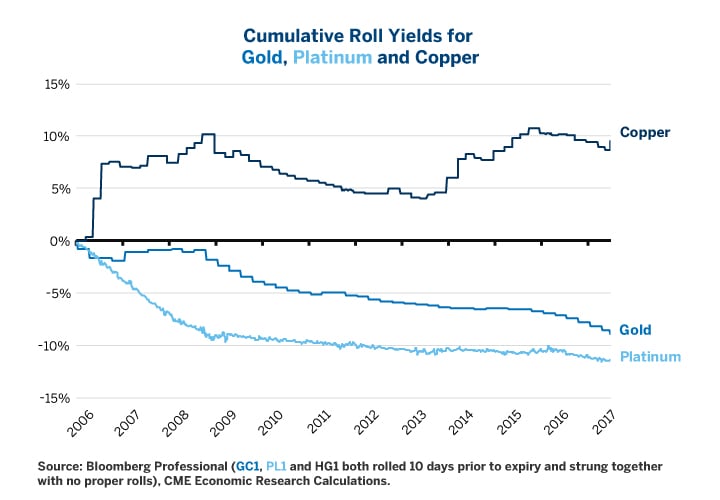

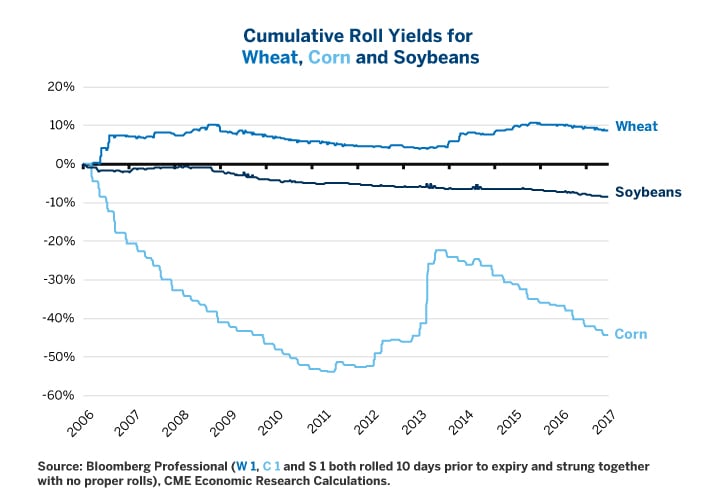

Unlike currencies, commodities don’t pay interest. Moreover, commodities must be stored, sometimes at significant cost. When a commodity’s forward price curve is positively sloped (future prices are higher than the spot price), it is said to be in contango, which implies negative carry. Unfortunately for buy-and-hold commodity investors, most commodity markets are in contango most of the time. Oil is a great example of this (Figure 11) and it’s true of other energy products and, to a lesser extent, metals and agricultural commodities (Figures 12-14).

Figure 11: Contango Costs: WTI fell 5% in Spot Terms But Fell 85% When Futures are Rolled Forward.

{kind=link}

Figure 12: Cumulative Energy Roll Yields.

{kind=link}

Figure 13: Cumulative Metals Roll Yields.

{kind=link}

Figure 14: Cumulative Agricultural Commodities Roll Yields.

{kind=link}

Factors to Consider When Trading Commodities Versus Commodity Currencies

Given that the commodity export currencies tend to 1) be positively correlated with commodity markets and 2) tend to have positive carry whereas commodities often display negative carry, should one be just long the commodity export currencies and short commodities to hedge? It’s an interesting question and a risky strategy. Here are factors to consider before taking that path:

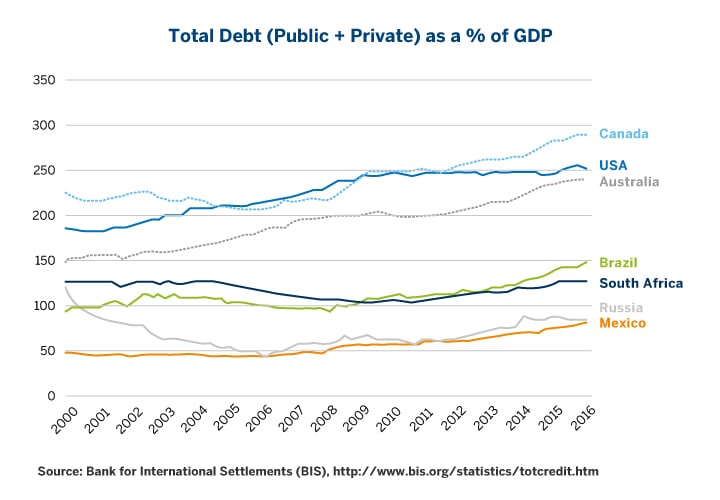

- What are the current interest rate differentials and where are they likely to head? While looking to the past can be interesting and informative, investing is about the future. Just because interest rate gaps between two currencies were large in the past doesn’t mean that they will remain large in the future. One great indicator of the sustainability of large interest rates gaps between currencies of commodity exporting countries and USD is the total level of debt (public + private). As debt levels rise, interest rates will eventually have to fall to make the debt burden sustainable (Figure 15). To a great extent, this explains why there is now negative carry on CADUSD: Canada’s debt burden exceeds that of the United States. Australia’s debt level is approaching U.S. levels. Brazil’s debt levels are also rising, albeit to moderate levels which might limit BRL’s carry going forward. South Africa, Russia and Mexico have lower levels of debt, affording their central banks more flexibility in terms of tightening policy.

- More broadly, changes in monetary policy expectations are among the factors that move currency markets.

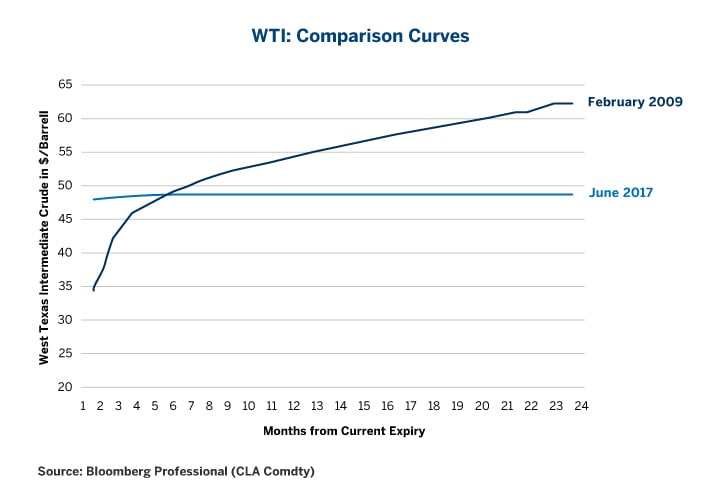

- Is the commodity currently in contango or in backwardation? A commodity, like oil, might tend to be in contango but can sometimes flip into backwardation, in which case it will exhibit positive carry until the backwardation situation reverses. For example, WTI had a strongly positive contango in 2009 but is relatively flat today, implying only a weak negative carry for the moment (Figure 16).

Figure 15: Typically, Higher Debt Implies Lower Interest Rates.

{kind=link}

Figure 16: Commodity Cost-of-Carry Varies Considerably with Time.

{kind=link}

- As such, while commodities’ storage costs and the absence of interest payments may burden the returns to long-only investors over time, they retain an inherent value that fiat currencies cannot have. That said, emerging market currencies often pay high interest rates precisely because central banks need to compensate holders for the currency’s perceived risk.

- Correlations are unstable: While the correlations between a given commodity and a given currency might tend to be positive over time, there is no guarantee that they will be positive at any particular moment in time.

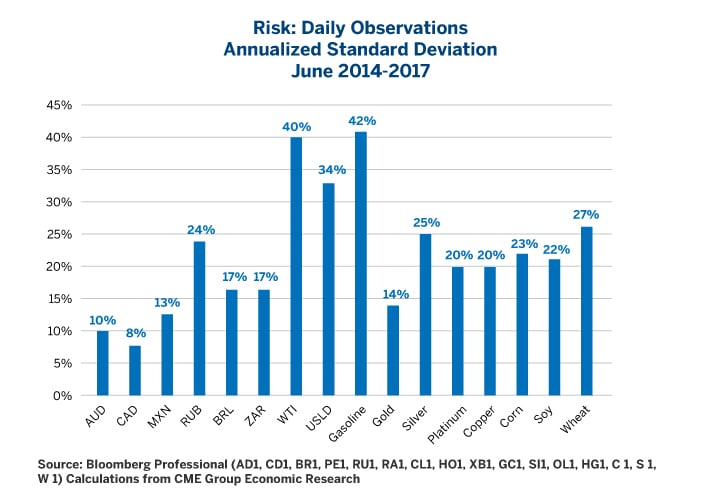

- Risk differentials: the key in the sizing of trades is knowing how volatile the two instruments are. Broadly speaking, commodities tend to be much more volatile than currencies (Figure 17). The relative volatility of currencies and commodities is also unstable over time.

Figure 17: Commodities are Often More Volatile Than Currencies.

{kind=link}

Recommended For You

Limiting Risk

Learn how to recognize the risk-reducing aspects of portfolios containing off-setting positions in highly-correlated instruments like commodity currencies and commodities.