{kind=link}

Dividend Futures as an Inflation Hedge?

Dividend Futures Overlooked as Inflation Hedge?

Have S&P 500® Annual Dividend Index futures been overlooked as an inflation hedge? With headline U.S. consumer price inflation surging to levels not seen since 2008, and to 1990 levels when excluding food and energy, investors are surely seeking ways to hedge their portfolios against the risk of rising inflation.

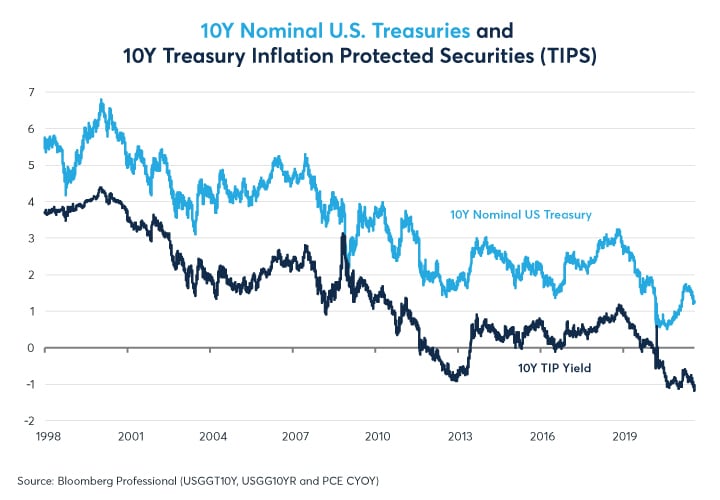

The most obvious choices for inflation hedging have drawbacks. For starters, Treasury Inflation Protected Securities (TIPS) offer -1.1% real yields (Figure 1). In other words, they will hedge upside risk against inflation but only with a one-percent loss with respect to the consumer price index (CPI).

Figure 1: As of July 19, 2021, 10-year TIPS pay consumer price inflation minus 1.07%

{kind=link}

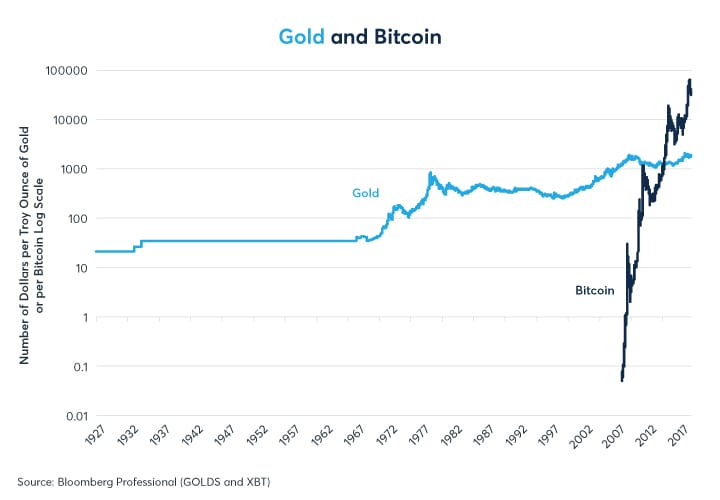

Other potential inflation hedges include bitcoin and gold (Figure 2), which are at fairly high levels historically. Gold isn’t far from its previous record high while bitcoin prices, though 50% or so off their recent record levels, are still trading higher than they ever had prior to the end of 2020. This isn’t to say that they couldn’t go higher – gold rose from $35 per ounce to $800 during the 1970s-- but both can be volatile inflation hedges. Since 1980, gold has seen drawdowns of as much as 70%. Since it came into existence in 2009, bitcoin has already seen three previous drawdowns of 93%, 83% and 82%.

Figure 2: Gold, relatively close to all-time highs, and bitcoin are subject to deep drawdowns

{kind=link}

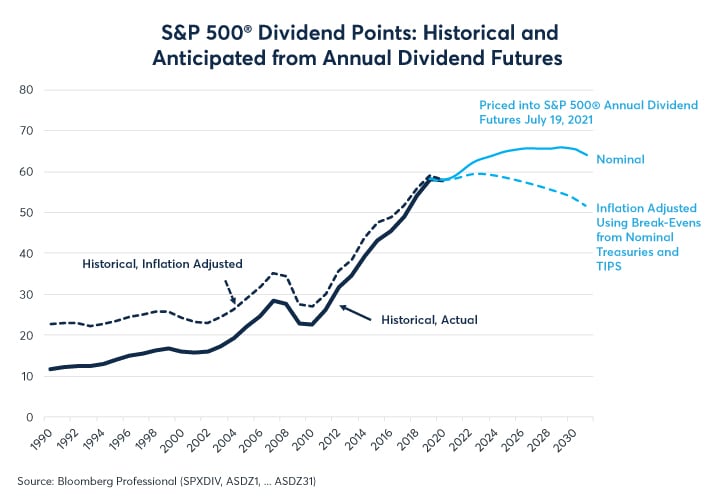

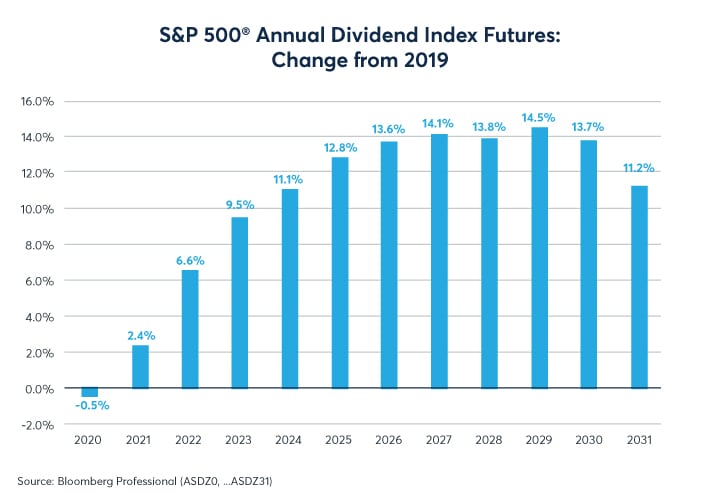

Contrast this with the pessimistic scenario priced into S&P 500 Annual Dividend Index futures. Although equity markets are trading near record highs, dividend futures see little prospect for dividend growth over the course of the 2020s, with market prices suggesting only about a 10-15% increase in payouts in nominal terms and an outright decline after inflation (Figures 3 and 4).

Figure 3: Dividend futures price low growth in nominal dividends & after-inflation declines

{kind=link}

Figure 4: Annual Dividend Index Futures suggest little growth in dividends during the 2020s

{kind=link}

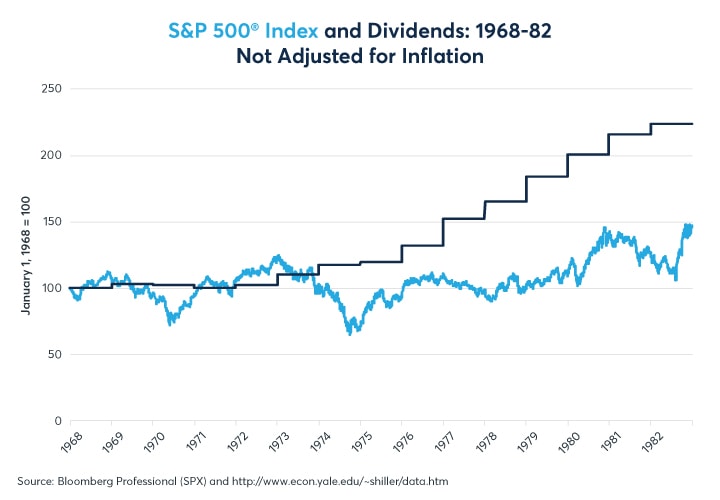

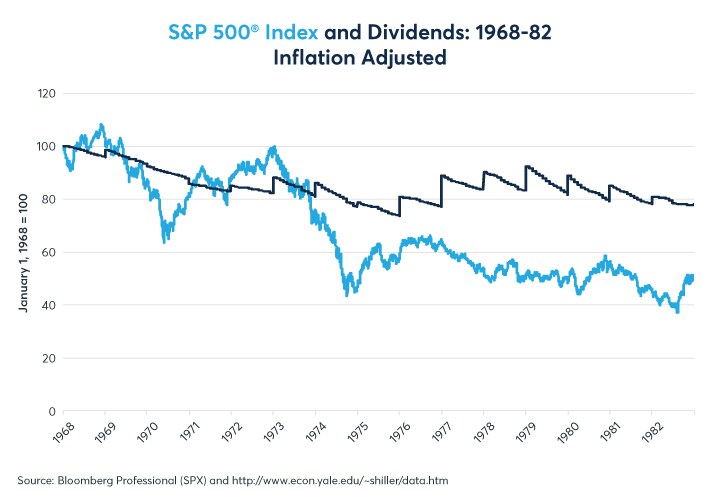

The last time the U.S. experienced severe and sustained inflation, dividends grew quickly even as equity markets suffered. From 1968 to 1982, the U.S. economy experienced stagflation, suffering four recessions (1969-70, 1974-75, 1980 and 1981-82) driving unemployment from 3.5% to 10.8% amid inflation rates that rose to as high as 13.5%. Stock and bond markets performed poorly. From its peak in 1968 to its low in 1982, the S&P 500 dropped by 6% in nominal (not inflation adjusted) terms. After taking inflation into account, it fell by 66%. Meanwhile, long-term U.S. Treasuries lost 48% of their value in real terms.

By contrast, dividend payments soared. In 1968, the S&P 500 paid out 3.07 index points worth of dividends. By 1982, dividend payments had risen to 6.87, a 124% increase in nominal terms which was in line with a 119% increase in corporate earnings over that period (Figure 5). Dividends didn’t quite match inflation, falling by 19% in real terms over the 1968-82 period or by about 1.5% per year. That’s not too far from the more or less guaranteed after-inflation loss that one would likely experience today on a 10-year TIPS if held to maturity. In any case, dividends did a lot better than the inflation-adjusted S&P 500 itself (Figure 6).

Figure 5: Dividends grew much faster than equity prices during the 1970s inflation

{kind=link}

Figure 6: Dividends came closer to keeping pace with inflation than equities

{kind=link}

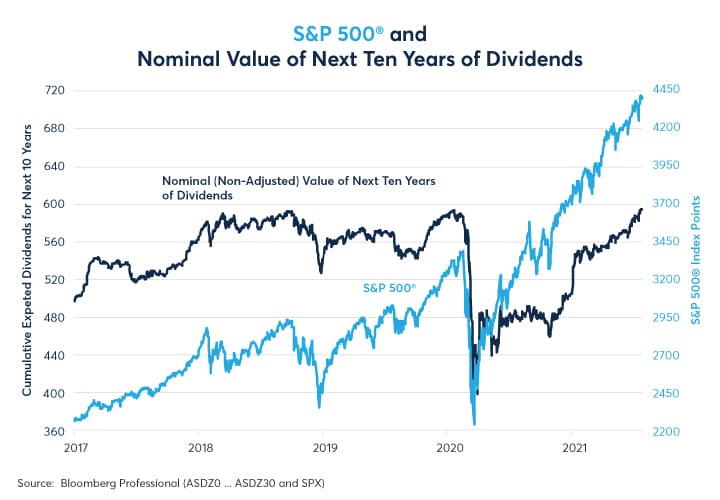

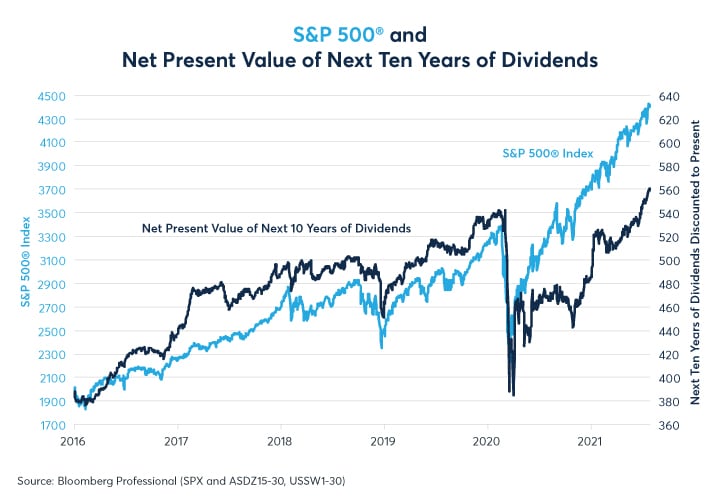

If one looks back to the beginning of 2017, the sum total of the market’s expectations for the next 10 years’ worth of dividends has only risen by 17% from 496 to 584 S&P 500 index points. Meanwhile, the S&P 500 itself is up 91% (Figure 7).

Figure 7: Expectations for future dividend payments stagnated even as stocks soared

{kind=link}

There seem to be two reasons why the S&P 500 has risen so much more quickly than dividends:

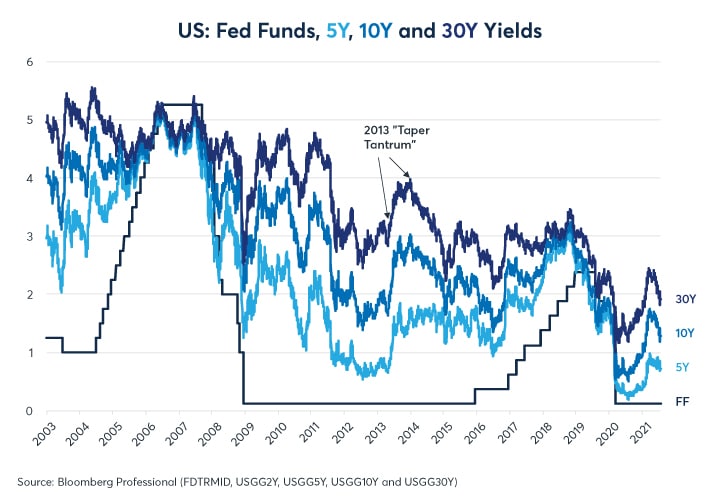

- Long term rates have fallen; at the beginning of 2017, 30-year bonds were at 3%; today they are closer to 1.85% (Figure 8). Declining long-term rates not only make bonds less attractive as an alternative to equities, they also increase the net present value (NPV) of future dividends.

- Quantitative easing (QE) appears to have driven the S&P 500 away from even the net present value of dividends. Between January 2017 and March 2020, the S&P 500 and the NPV of dividends tracked one another closely. Since the Fed began QE4, with $4.5 trillion in asset purchases so far, stocks have risen even faster than the rebound in dividends the fall in long-term interest rates would suggest (Figure 9).

Figure 8: Falling long-term rates has raised the NPV of future dividend payments

{kind=link}

Figure 9: Even falling long-term bond yields can’t explain all of the market’s pandemic rally

{kind=link}

The problem for equity investors is that the S&P 500 and other indices might be negatively sensitive to rising bond yields. If the scenario of quiescent inflation, currently favoured by central bankers and investors alike, turns out to the correct, equity and bond investors may do just fine in coming years. However, if, inflation proves to be more persistent, a reckoning could be in store. Rising bond yields would, all else being equal, lower the NPV of future corporate cash flows, be they earnings or dividends. Moreover, rising yields could make bonds relatively more attractive, enticing investors out of the equity market and into fixed income.

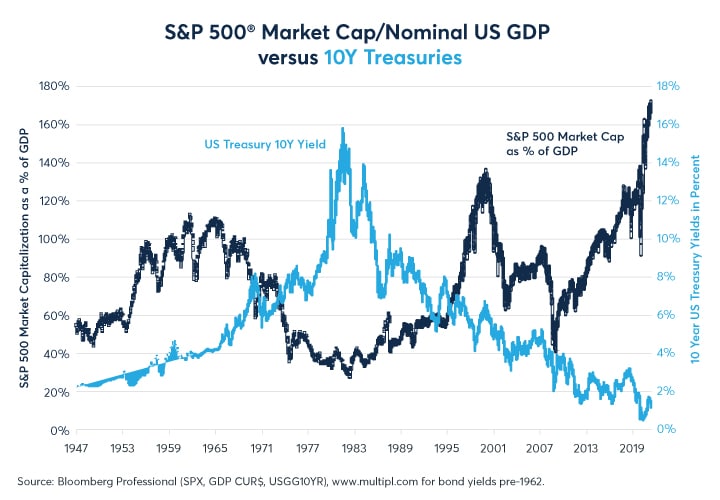

That equity valuation and bond yields tend to vary inversely is hardly news (Figure 10) but it is worth pointing out that the S&P 500’s market cap plunged from 110% of GDP in the mid-1960s to just 28% of GDP by 1982. Today, the S&P 500’s market cap is at a post-World War II record of 171% of GDP.

Figure 10: Equity valuations and bond yields tend to vary inversely

{kind=link}

For much of the past 40 years, stock prices have been rising faster than dividend payments for one reason: we have been in a secular downtrend in long-term rates. Should higher inflation reverse that trend, and eventually begin to send long-term interest higher, stock prices might underperform the growth of dividend payments once again, as they did from the late 1960s until the early 1980s. If that turns out to be the case, the S&P 500 Annual Dividend Index futures might turn out to be a decent inflation hedge, especially since its currently pricing such slow growth in dividends going forward.

Futures trading is not suitable for all investors and involves the risk of loss. Futures are leveraged investments and, because only a percentage of a contract’s value is required to trade, it is possible to lose more than the amount of money deposited for a futures position. Therefore, traders should only use funds that they can afford to lose without affecting their lifestyles and only a portion of those funds should be devoted to any one trade because traders cannot expect to profit on every trade.

Dividend Index Futures

S&P 500 Dividend Index futures provide efficient tools to hedge or express a view on the U.S. dividend market, regardless of the direction of the S&P 500 index.