{kind=link}

Did Quantitative Easing Help Spur Growth?

When it comes to quantitative easing (QE), go deep or go home. Using nearly a decade of evidence we look at what impact QE had in the United States, UK, Eurozone and Japan. Despite all the hopes and fears generated by the asset-purchase programs of central banks to stimulate their economies, for the most part, as far as we can tell QE had no actual impact on growth. Therefore, there is no reason to fear the ending of QE or even the reversing of QE as in the shrinking of a central bank’s balance sheet bloated by these asset purchases.

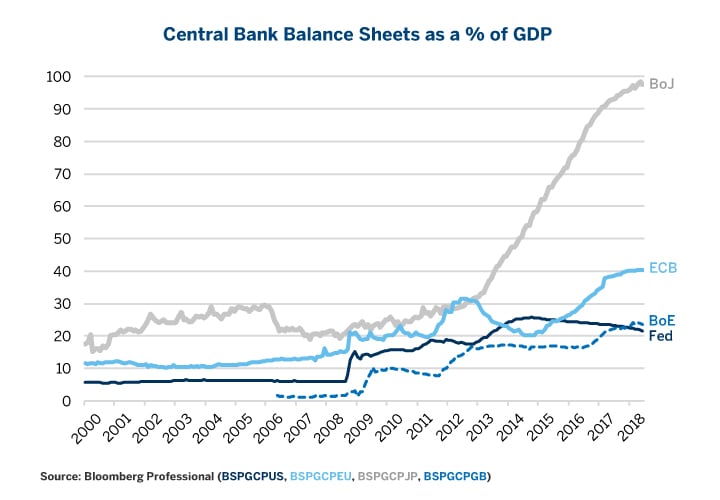

There is one major caveat though. Unlike in the U.S. or Europe, QE may have helped Japan recover, perhaps because of the gargantuan nature of the Bank of Japan’s (BoJ) asset-purchase program (Figure 1). Or, more likely because the BoJ targeted part of its QE where it really mattered – in corporate debt and equities. As the BoJ winds down its QE, it will be interesting to see how the Japanese economy responds.

Figure 1: Should the Ending of the Massive Balance Sheet Expansion be a Concern?

{kind=link}

The U.S. Experience

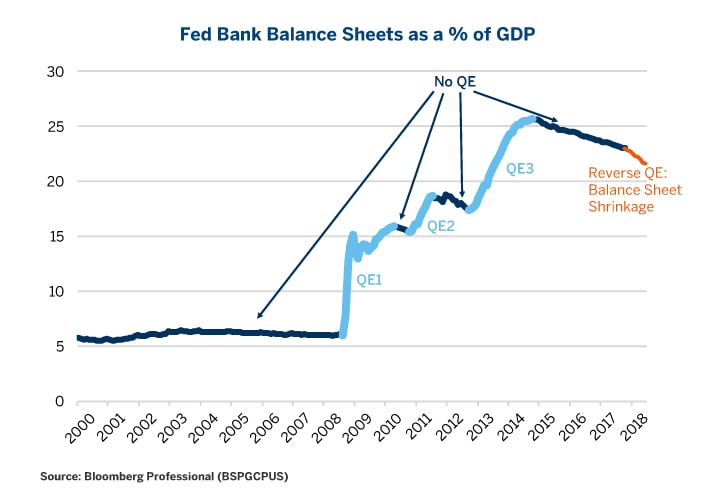

QE has gone through essentially seven phases since it began: three phases of QE, with the Fed buying mostly U.S. Treasuries and some highly rated securitized mortgages, and three phases of post-QE pause. Finally, since October 2017, the Fed has been doing a reverse QE – shrinking its balance sheet in dollar-terms and not just as a percentage of GDP (Figure 2).

Figure 2: Three Phases of QE and Now Reverse-QE.

{kind=link}

Evaluating the impact of QE1, which began in 2008, is nearly impossible. At the time the Fed began rapidly expanding its balance sheet, a number of other events and policy changes were taking place. They included the banking bailout, the auto bailout, advent of zero interest rates, the stimulus package and an accounting change that allowed banks to hold assets on their books to maturity at cost rather than marking them to market. Had all of these taken place in the absence of QE1, how would the economy have performed? Would it have recovered as it did? At the time, it was anybody’s guess.

Since evaluating the impact of QE1 is so difficult, the Fed can be forgiven for being hopeful that launching QE2 in late 2010 would speed up the recovery. So far as we can tell, QE2 had little or no impact on the pace of the economic expansion. That said, QE2 came close on the heels of QE1 and was relatively modest in size, making it hard to tell what impact it had.

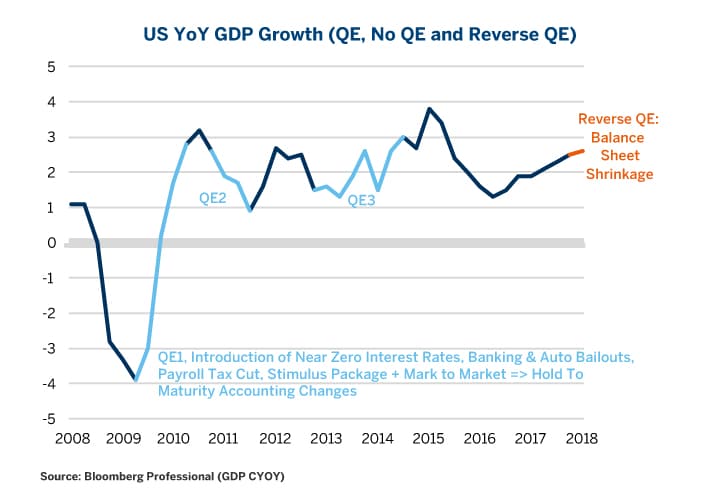

As such, it’s really QE3 that provides the strongest evidence. QE3 began in mid-2012 and ran through the early part of fall in 2014. QE3 was nearly the size of QE1 and came well after its predecessor QE2. By all appearances it had no impact on the pace of economic growth. Neither did ending it. After the Fed brought it to a close in the fall of 2014, the economy spent the next three years growing at about the same pace as before. Finally, in the nine months since the Fed began actively shrinking its balance sheet, the economy actually accelerated – although the improvement is probably the result of tax cuts and spending increases and not due to how many bonds the Fed had on its balance sheet (Figure 3).

Figure 3: If Fed’s QE Had Any Impact on GDP Growth, It’s Not Simply Obvious.

{kind=link}

The Eurozone Experience

The European Central Bank’s (ECB) QE program differs from the Fed’s in a few key aspects:

- Timing: The timing of the balance-sheet expansions and contractions were completely independent of the Fed.

- Multiple sovereigns: The ECB had to buy bonds issued by over a dozen sovereign nations, whereas the Fed only had to buy from one government.

- Credit quality: the ECB went lower in terms of credit quality than the Fed, which stayed with AAA securities.

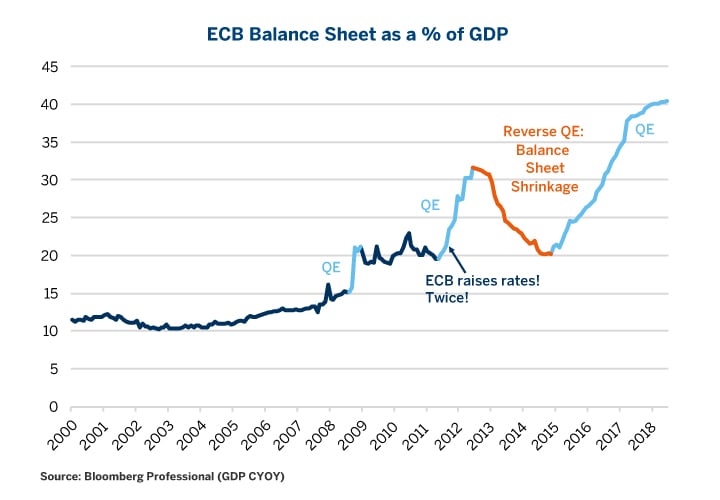

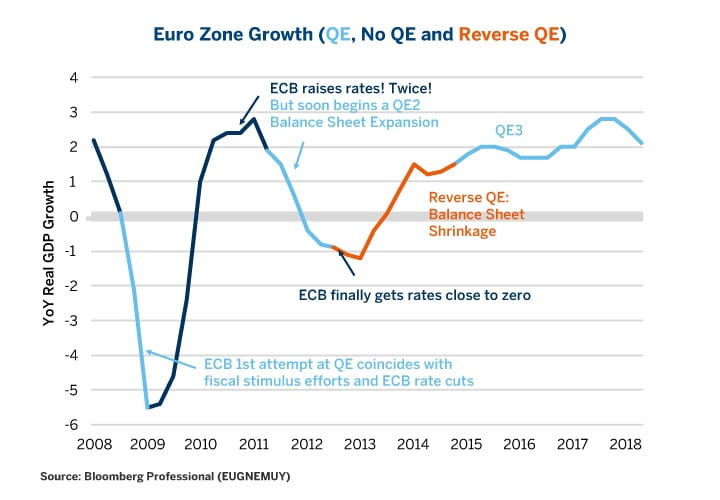

For all these differences, the lack of obvious economic impact remains the same. The ECB expanded its balance sheet significantly in 2008 and the economy began to rebound in late 2009. Even so, the rebound may have been more supported by a vast expansion of fiscal deficits and the ECB cutting rates from 4.5% to 1% than by the initial balance sheet expansion (Figures 4 and 5).

Then in 2011, the ECB began a sort of QE2 (although it didn’t call it that). Did this help the Eurozone economy? Absolutely not. The Eurozone economy tanked during the second part of a double dip recession. Sovereign-bond spreads exploded despite the ECB asset purchases. The culprit though wasn’t QE2, it was the fact that 1) unlike the Fed and the Bank of England, the ECB had not yet cut rates to zero and 2) fearing inflation, it raised rates twice in 2011, even as it expanded its balance sheet.

In 2012, the ECB completely reversed course. Its new chairman, Mario Draghi, promised to do whatever it took to prevent Spain, Italy, Portugal and Ireland from defaulting on their debts. Moreover, the ECB began cutting rates and eventually brought them to zero. Curiously, during 2012 and 2013, the ECB’s balance sheet contracted from over 30% to around 20% of GDP. Was this a disaster for the economy? Not at all. The economy actually hit bottom and then began to expand.

Finally, in 2014 with a recovery underway, the ECB began a massive bond-buying program that continues to this day. Did the pace of economic growth accelerate as the bond buying picked up? In short, no. So far as we can tell, it did not. The ECB subsequently began to slow its pace of purchases in 2017 with no obvious impact on the pace of economic growth so far.

Figure 4: The ECB’s 2013-14 Balance Sheet Shrinkage Didn’t Hurt Growth.

{kind=link}

The lesson from Europe is clear: what matters is getting rates to zero in a crisis and keeping them low. Balance-sheet expansion won’t help if the central bank raises rates as the ECB did twice in 2011. The corollary is that there is little to be feared, from a macroeconomic perspective, either from a halt to QE or from a future ECB balance-sheet shrinkage. Yields on certain government bonds, notably the German Bund, might go higher but that probably wouldn’t be a bad thing for the economy.

Figure 5: Get Rates to Zero and Forget About the Balance Sheet is the Lesson from Europe.

{kind=link}

The UK Experience

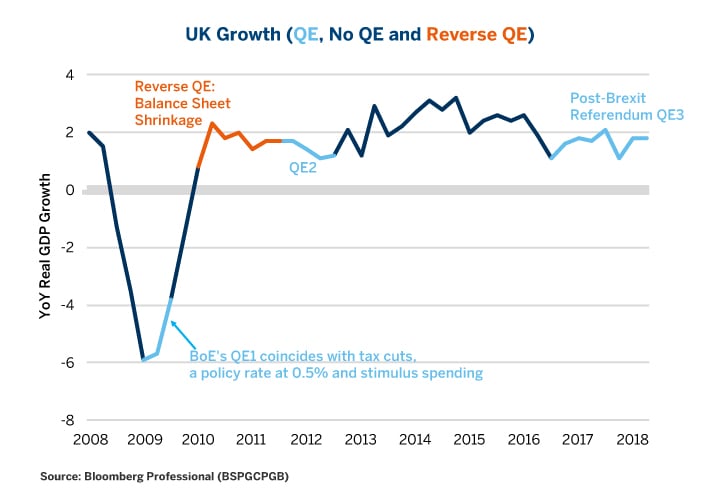

In many respects the UK’s experience of the 2008 crisis is similar to that of the U.S. The banking system suffered but the central bank got rates below 1% quickly and kept them there; the government implemented a large fiscal stimulus in 2009 followed by a long period of austerity. Neither the U.S. nor the UK experienced a double dip recession like the Eurozone did after the ECB hiked rates 2011.

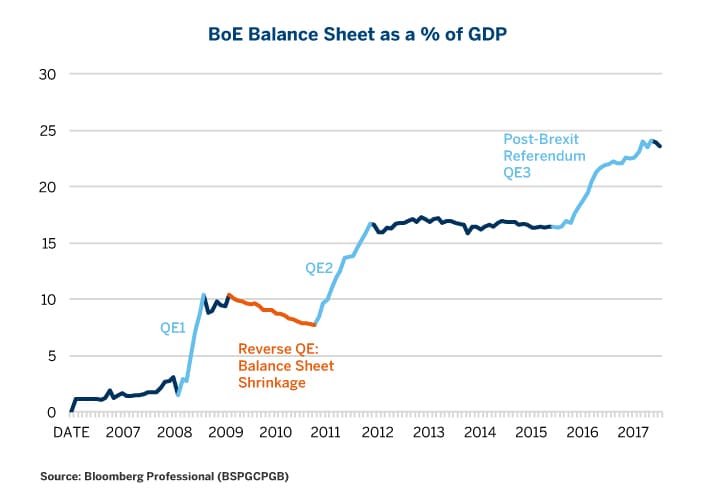

Likewise, the Bank of England’s QE more closely resembled that of the Fed in terms of asset mix, but the timing differed. The BoE’s version of QE1 and QE2 lagged the Fed’s by about six months to a year and its QE3 began only after the Brexit referendum. As is the case with the Fed, the BoE’s QE1 is difficult to evaluate because it occurred at a time when so many other policy changes were taking place. BoE’s QE2 and QE3 produced no discernable acceleration in GDP growth. The BoE also shrunk its balance sheet in 2010 and 2011 and, as in the Eurozone experience, allowing the size of the balance sheet to decline did not result in a drop in the pace of economic growth (Figures 6 and 7).

Figure 6: BoE Balance Sheet Expansion Shows Little Correlation to Growth.

{kind=link}

Overall, the UK experience endorses the notion that QE doesn’t really work and ending or reversing QE doesn’t much matter. Rather, what matters is getting policy rates close to zero quickly and keeping them there. QE might depress government bond yields but that doesn’t appear to improve economic growth. After all, in the decade since the crisis began, the problem in the U.S. and the UK was never that the government paid too much to borrow money; it was that the private sector lacked access to credit, but subsequently it did.

Figure 7: BoE Balance-Sheet Shrinkage in 2010 and 2011 Didn’t Derail the Recovery.

{kind=link}

Japan: The Contrarian (Sort of)

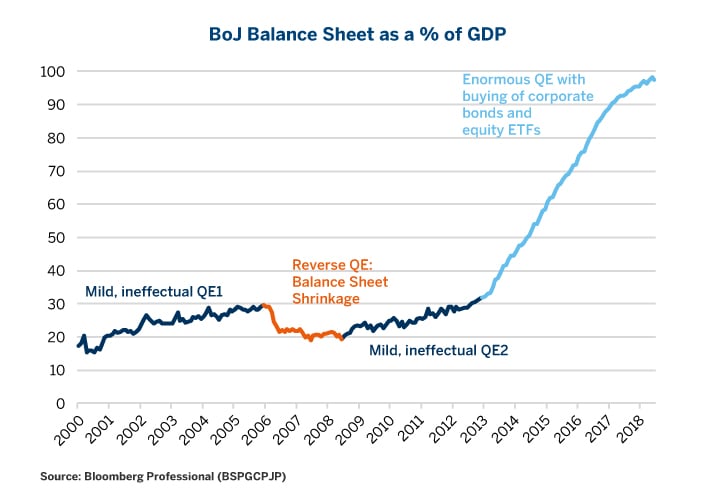

Between 2000 and 2005, Japan made a feckless attempt at QE that looked, in retrospect, much like what the Fed, the ECB and the BoE would do in the next decade. Their balance sheets expanded from 15% to 30% of GDP but the economy remained stagnant and deflation persistent. Then in 2006 and 2007, they shrunk their balance sheets and the economy did fine.

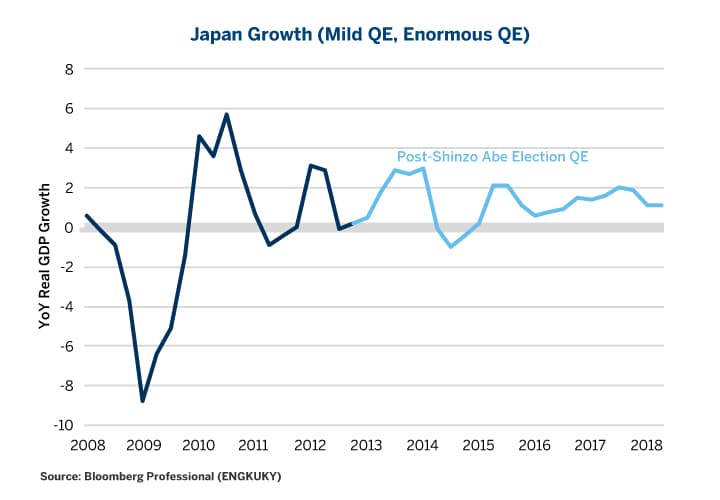

Like the rest of the world, the 2008 crisis hit Japan’s GDP hard. The Bank of Japan (BoJ) responded with a mild QE that took the balance sheet back up to 30% of GDP from 20% between 2009 and 2012. It was to little avail. Then in 2013, something radical happened. The BoJ dispensed with its minor purchases of government bonds and conducted a vast QE, taking its balance sheet from 30% to nearly 100% of GDP. Economic growth remained solid but didn’t necessarily accelerate (Figures 8 and 9). We would add that Japan’s GDP growth understates the country’s economic improvement: one must remember that Japan’s population is declining, so real GDP per capita is improving faster than the GDP chart will indicate. Moreover, Japan’s long period of deflation has more-or-less ended.

Figure 8: BoJ QE Differs by More Than Just Size But (Credit Quality) Depth.

{kind=link}

What differentiated the BoJ’s QE after Shinzo Abe’s election victory was not just size but depth. Rather than merely buying up Japanese Government Bonds (JGBs), the BoJ went deep in terms of credit quality. It bought corporate bonds and even equities via exchange traded funds (ETFs). In doing so, they may have discovered the true key to a successful QE. What matters isn’t government bond yields. What matters is whether the private sector can begin borrowing and lending money and can afford to finance its debt burden.

Figure 9: Did Japan’s Massive QE Really Boost Growth?

{kind=link}

This should come as no surprise. The Eurozone, which has the unique situation of multiple sovereign nations issuing debt into a common currency, began to recover when the ECB backstopped the debt of Italy, Portugal, Ireland and Spain, putting the markets on notice that it would do “whatever it takes.” Likewise, our research into U.S. employment shows that one factor alone explains 60% of the month-on-month change in non-farm payrolls: credit spreads. If credit spreads are wide (meaning that loans are difficult to get or unavailable), employment collapses. If credit spreads are narrow, employment grows. It’s that simple.

Amid a synchronized global expansion, the BoJ, ECB and BoE are all following the lead of the Fed and ending QE. Someday they may go into reverse QE. Fear not. So long as they keep rates at an appropriate level (meaning low), economic growth will likely continue despite the lack of support from asset purchases. Bond markets could sell off but that won’t likely slow growth unless credit spreads blow out.

That said, QE isn’t over. Like the monster in a hit horror movie, it will likely be back for a sequel. If the Fed continues to tighten policy at anything like its current pace, it could produce a recession later this decade or in the early 2020s. The temptation to go into QE4 will be strong.

In the meantime, debt levels are soaring in Australia, Canada, China, Hong Kong, Singapore and South Korea. Even if the Europeans, Americans and Japanese aren’t tempted by another QE, the central banks of some of these other countries might be. If so, they would be well advised to look at the experience of the past decade and think seriously about buying a small amount of corporate bonds and equity ETFs rather than a massive quantity of public or quasi-public debt. Going deep in terms of credit quality or even out of the realm of credit and into equity might get them a bigger bang for their buck than needlessly noodling around buying up government bonds.

If the central bank charter doesn’t permit buying corporate bonds or equities, maybe the central bank charter needs to change in case such a strategy is needed.

Bottom Line

- After a decade, there is little evidence that QE boosts growth.

- There is equally little evidence that balance-sheet shrinkage slows growth.

- It might be more effective for central banks to buy corporate bonds or equities via ETFs.

CME Interest Rates Products

10-Year Treasury Note futures ADV rose nearly 42% during Singapore trading hours (8 a.m. to 8 p.m. SGT) in Q2 2018 versus a year ago while open interest grew nearly 13% during the same period. Protect your investment portfolio with our liquid Interest Rate products.