{kind=link}

China-Plus-One Strategy

The disruption wrought by the COVID-19 pandemic has been profound on the world’s factory floors, possibly accelerating the adoption of a “China-Plus-One” strategy by manufacturers wishing to diversify their sources of production away from the world’s second largest economy, which is currently locked in a trade dispute with the United States. As businesses seek to wean their dependence on China, moves towards diversification seem probable.

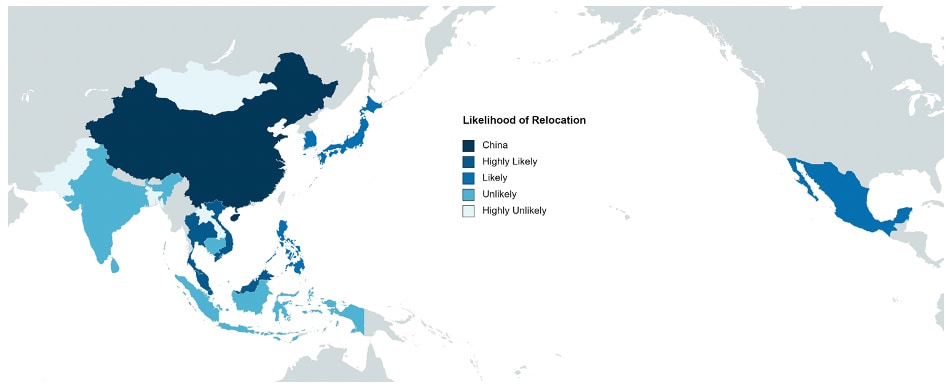

The Tiger Cub economies, namely Malaysia, Thailand and Vietnam, are in a prime position to attract manufacturers seeking to supplement their operations in China with other centers of production in the region. We have arrived at this conclusion using our “Manufacturing Attractiveness” model, which considers 23 economic indicators spanning five categories - including manufacturing competitiveness and labor costs, but not the immediate sunk costs of relocation.

American business sentiment is indicative of the shifting sands: as China looks to tap into its growing middle class to boost domestic demand for a variety of consumer goods as a way to reduce its reliance on exports, American manufacturers are increasingly looking outward.

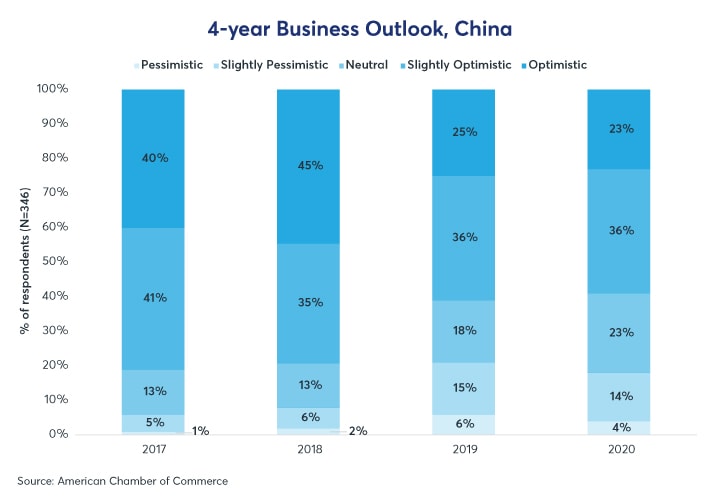

Figure 1: Optimism in the Chinese economy has fallen from 81% to 59% in 4 years

{kind=link}

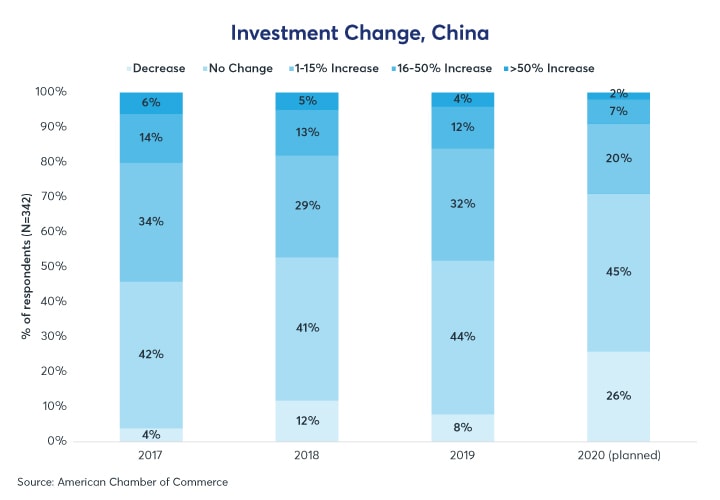

Figure 2: Proportion of business owners looking to decrease investment has risen from 4% to 26% in 4 years

{kind=link}

Among the 346 American businesses surveyed by the American Chamber of Commerce, overall optimism in the Chinese economy has declined 22 percentage points from 2017 to 2020 (Figure 1), while the proportion of business owners looking to decrease their investment in China has risen by 22 percentage points over the same period (Figure 2). The changes are reflected in the decisions undertaken by major producers. Several large electronics companies are moving production from China to Vietnam; a manufacturer of motorcycles to Thailand, and a producer of rubber to Malaysia.

While a confluence of the U.S.-China trade policy and the COVID-19 pandemic have stirred producers to reassess their supply chains; the relocations are also being spurred by several structural factors, including rising Chinese labor costs.

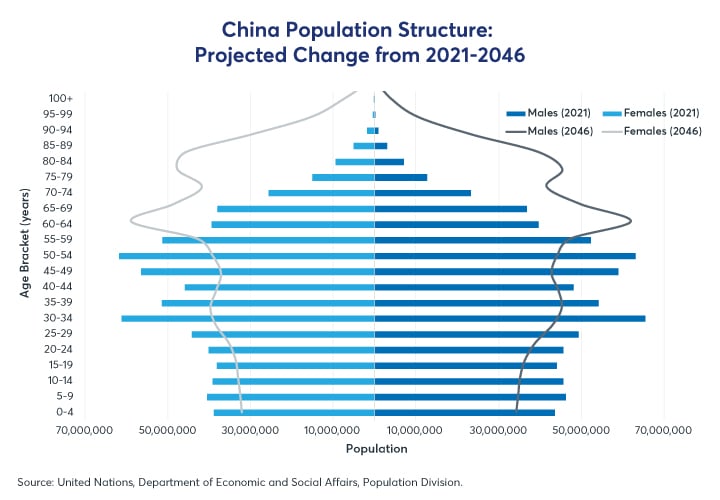

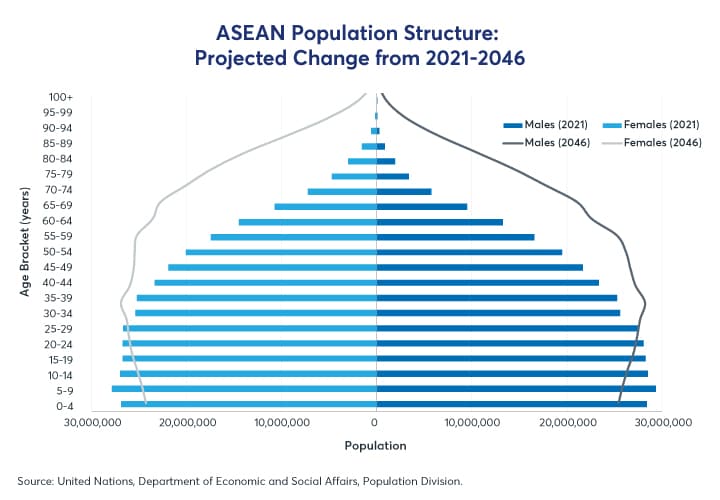

China may become a less attractive investment destination for labor-intensive industries. This could partially be the result of forthcoming demographic changes. The number of Chinese in the 20-to-65 age category is projected to shrink 14% over the next 25 years (Figure 3), while this bracket will burgeon across much of South Asia and Southeast Asia (Figures 4-6). In the short run, this could decrease the volume of readily available Chinese labor for manufacturers to call upon.

Figure 3: China may begin to see all age brackets below 60 decline

{kind=link}

Figure 4: ASEAN is projected to see a slight decrease in youthfulness, and foster a middle-class to rival that of China

{kind=link}

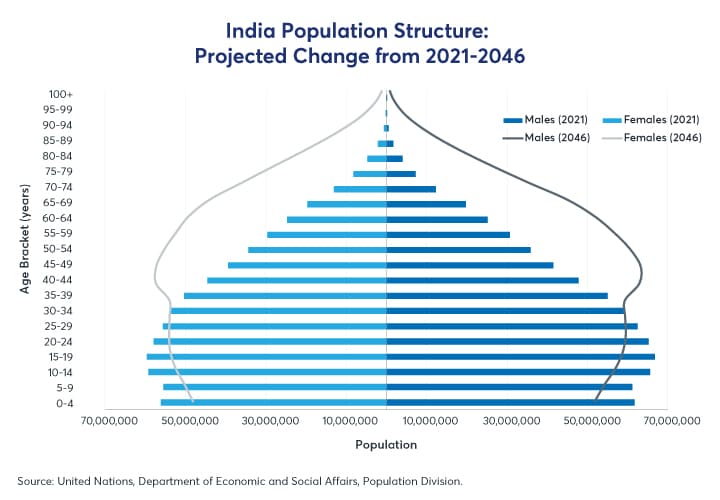

Figure 5: India is projected to become the world’s most populous nation in the next decade

{kind=link}

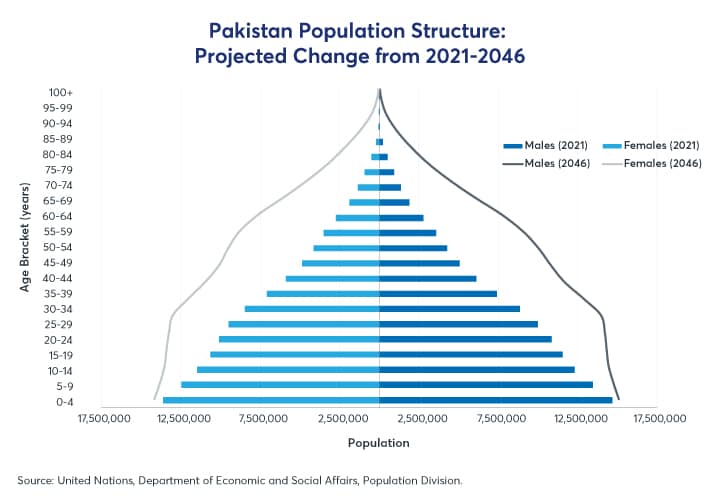

Figure 6: Pakistan is one of the few Asian nations to have not yet fully reaped the rewards of their demographic dividend

{kind=link}

The Chinese government shifted to a three-child policy in May of 2021. While the impact of such a policy change will only be seen in fertility data from 2022-23, and will not materially impact labor-force growth until the 2040s, survey data suggests that few Chinese parents are looking to have a third child. Observers attribute this attitude to rising costs of childcare and extracurricular education – an issue that the Chinese government addresses in its current five-year plan. Kindergarten fees, at times more expensive than college tuition, have increasingly encouraged grandparents to take the brunt of childcare duties. This has limited the government’s ability to raise the retirement age lest such a policy shift discourage young couples from having children.

The move from a renkou hongli (“demographic dividend”) towards a rencai hongli (“talent dividend”) does not appear to have been achieved solely through the alteration of existing legislation, supporting the case for new, resilient institutions to promote elderly care and child support.

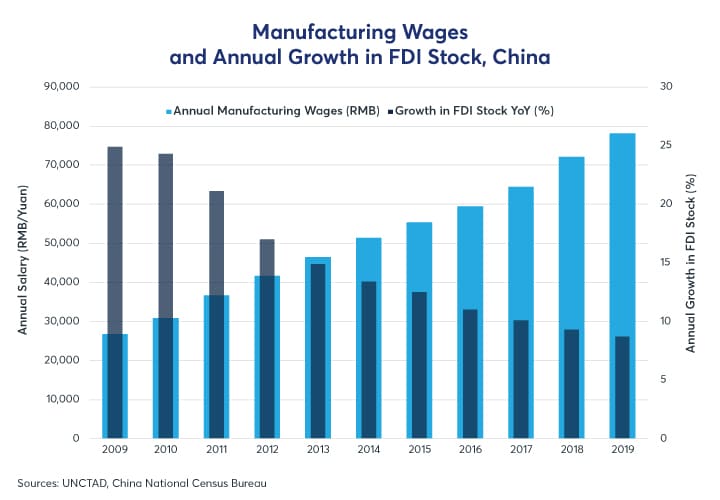

Equally, wages are growing quickly and Foreign Direct Investment (FDI) growth is slowing (Figure 7). Today, manufacturing wages in China are higher than in much of Southeast Asia and Latin America.

Figure 7: Salaries have more than doubled in 10 years, but FDI growth has slowed

{kind=link}

Rising wages are not a problem by their very nature. While wages are indeed rising precipitously, productivity growth in China has easily outstripped its competitors (Figures 8-9).

Figure 8: Chinese productivity levels have more than doubled since 2009

{kind=link}

Productivity growth has slowed in the past decade, largely following a global trend. However, part of this slowdown can be attributed to falling levels of domestic rural-to-urban migration. For most emerging markets, the highest rate of productivity growth occurs during a period of significant migration from low-productivity rural areas (where the marginal product of labor is very low) to high-productivity urban towns and cities. Such was the case for Japan in the 1950s, the Soviet Union in the 1960s, and China in the 2000s. During much of this period, China enjoyed labor productivity growth as high as 14% -- facilitated by urban employment growth of over 4%. By contrast, the growth rate of urban employment in 2019 fell to its lowest level since 1993 at below 2%.

Figure 9: Chinese productivity growth has slowed as part of a global trend

{kind=link}

Rising wages and productivity are signs of a maturing economy, and suggest that China may be moving away from labor-intensive to capital-intensive industries. However, while the Four Asian Tigers of Hong Kong, Singapore, South Korea and Taiwan all successfully pivoted to capital-intensive industries in the late 20th century, it could be challenging for China to emulate their success. The ongoing U.S.-China trade dispute could hamper Chinese ambitions to adopt Industry 4.0, the automation of traditional manufacturing practices, principally due to the decline in foreign knowledge spillovers and FDI. This may inhibit technological innovation, which could translate to lower total factor productivity growth over the next decade.

This shortfall may be filled by domestic R&D and innovative activity, should the government foster a more favorable entrepreneurial ecosystem. Chinese research universities perform exceptionally well on bibliometric indicators, yet research is now increasingly in the hands of the private sector. Private sector firms, especially those that are fast-growing and innovative, may be crowded out by state-owned enterprises (SOEs), and could face difficulties accessing credit in a capital market that is calibrated towards such SOEs – not unlike the Korean chaebol.

To this end, China set its first formal target for private lending in 2018, with the China Banking and Insurance Regulatory Commission (CBIRC) suggesting that no less than 50% of new corporate loans go to private companies that have been operating for more than three years. At the time of the announcement, the private sector accounted for more than 60% of GDP, yet received 25% of commercial loans.

Despite such structural challenges, competing with China Inc. remains no easy feat. The business environment in China remains one of the most attractive in the region and has seen a positive trend over the past decade (Figure 10).

Figure 10: The trade-off for lower wages is often a more cumbersome business environment

{kind=link}

Dynamic economies looking to outcompete China on its home turf will need to offer more than competitive wages and an abundance of youth. Consequently, we have considered 23 economic indicators across 5 categories: manufacturing competitiveness, institutions and regulation, labor market and human capital, labor costs, and tax policies. The z-scores for each category have been used to calculate a weighted average in the following proportions (Figure 11). The result is the Manufacturing Attractiveness Index (MAI).

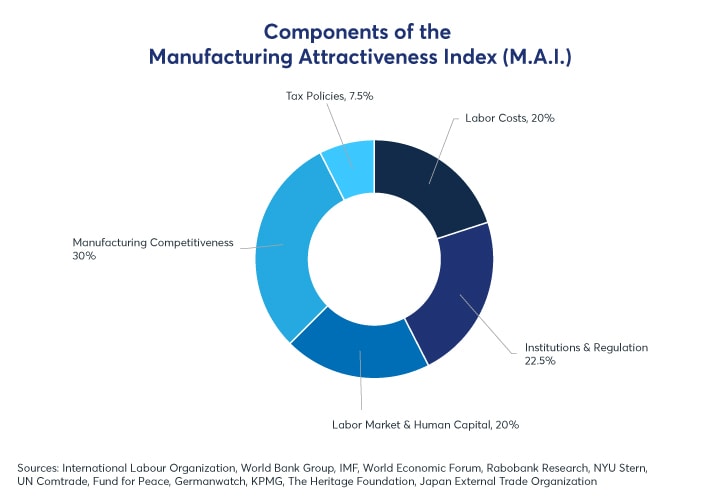

Figure 11: The Manufacturing Attractiveness Index considers 23 economic indicators

{kind=link}

A higher weight has been assigned to “Manufacturing Competitiveness” and “Institutions & Regulation”. Manufacturing Competitiveness is particularly prominent, as it dictates the comparative advantage of each nation’s export basket. For instance, much of South Asia is geared towards the production of textiles and clothing as opposed to electronics – and thus stands to gain relatively less than the Association of Southeast Asian Nations (ASEAN). With this in mind, export similarity with respect to China constitutes 25% of the overall M.A.I.

Institutions & Regulation addresses the qualms that have been reported by manufacturers currently in the process of decreasing investment in China. According to the American Chamber of Commerce -- of those decreasing investment, 29.5% are doing so due to U.S.-China trade policy, and 12.7% due to domestic competition. As a consequence, an attractive destination for such investment would be one that offered low levels of political, commercial, and macroeconomic risk – and did not offer preferential treatment to state-owned enterprises (an issue that is particularly pertinent in China’s automotive sector, which is one of the furthest away from competitive neutrality).

In contrast, we believe “Tax Policies” are relatively inconsequential. The standard deviation of corporate tax rates across South Asia and Southeast Asia is relatively low, and is thus unlikely to be a decisive factor in influencing manufacturing decisions. Moreover, the ability to collect tax (which itself is an implicit component of Institutions & Regulation) is perhaps more important than the de jure tax rate itself.

The results are as follows, with respective quartiles highlighted (Figures 12-13). A value of zero indicates the mean value in each category for the 16 countries in question. It follows that a positive value is above average for the group of 16, whereas a negative value is below average.

Figure 12: Manufacturing Attractiveness Index by Component

{kind=link}

The top contenders for FDI leaving China are Malaysia, Singapore, Thailand, and Vietnam respectively – with Japan following closely. Thailand and Vietnam benefit from similar export baskets to China, whereas Malaysia and Singapore boast efficient institutions and a highly flexible workforce. South Asia is dragged down by low levels of export similarity, principally due to its specialization into textile production.

Figure 13

{kind=link}

The relocation of production capabilities is likely to be fragmented and piecemeal. No single country can absorb all of China’s manufacturing capabilities. Only India has the manpower and domestic market to achieve such an endeavor, yet it has a dramatically different export basket. Instead, we are likely to see the production of certain products move towards certain countries, as determined by comparative advantage: Malaysia and Vietnam in electronics, Thailand in automobiles and packaged foods, Indonesia in machinery and petrochemicals, and Singapore in semiconductors and biopharmaceuticals. As a result, supply chains may be fragmented across Southeast Asia – a business strategy known as “China-Plus-One.”

Due to the size of the Chinese middle class, the manufacturing diversification is less likely to be an “exodus” and more likely to be a gradual shift. According to the American Chamber of Commerce, 58% of businesses operating in China are looking to produce for the Chinese market itself – and may thus position themselves as close to the consumer as possible. However, the extent to which this will force manufacturers to setup in China may diminish in the future if we see greater integration of the Regional Comprehensive Economic Partnership (RCEP).

With a growing middle class projected to challenge that of China by the mid-century, and more firms looking to adopt a China-Plus-One strategy (84% of Japanese companies surveyed by Nikkei are already looking to diversify their supply chain) – ASEAN and the Tiger Cub economies could become manufacturing powerhouses over the next quarter century.

Needless to say, such a projection is contingent on trade relations. The new U.S. administration appears to have adopted much of the previous administration’s stance on Sino-U.S trade, with tariffs potentially in the pipeline on Indian and Vietnamese exports. Even if some manufacturing operations move away from China, there is no guarantee that trade restrictions might not move in tandem.

It is important to recognize that manufacturers are not perfectly footloose, as the relocation of any part of a supply chain comes at a substantial sunk cost. Our model has not considered, among other variables, commercial land prices, currency volatility, the costs associated with retraining the local workforce, and the availability of transportation and shipping routes. These indicators are difficult to standardize and quantify, but would almost certainly influence manufacturing decisions. The immediate costs associated with relocation may also bring about a transitory bout of cost-push inflation, although the increased resilience of supply chains in the long run may ease price levels due to the decreased incidence of disruption.

Ayushman Mukherjee

Ayushman Mukherjee will be attending the University of Cambridge in October to study Economics.