Trading SOFR Futures

{kind=link}

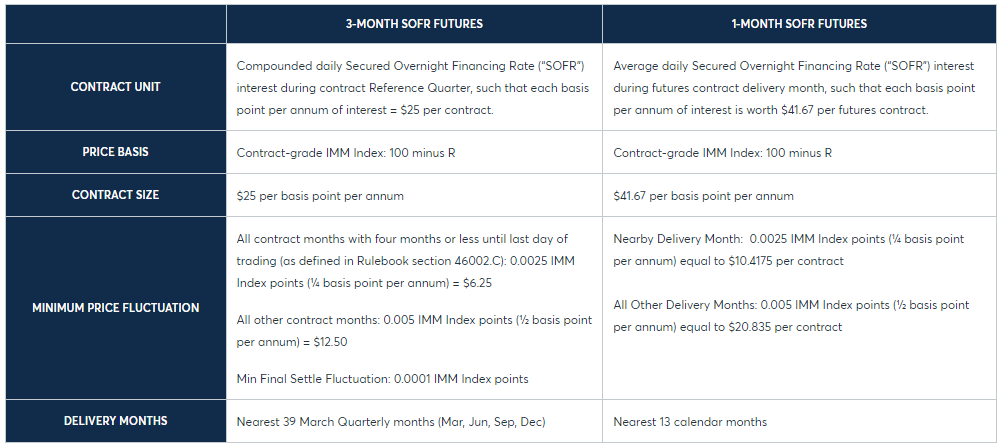

CME Group offers one-month and three-month futures contracts based on the Secured Overnight Financing Rate (SOFR).

The combination of one-month and three-month contracts facilitates price discovery at various points of the money market curve.

The one-month SOFR futures contracts apply the monthly average of overnight SOFR to one-month contracts that are nearly identical to our 30-Day Fed Fund futures in terms of contract design. SOFR futures trade in IMM index points. The final settlement price is determined by the arithmetic average of the daily SOFR during the delivery month carried out to the fourth decimal place.

The last trading day and final settlement will be the last exchange business day of the contract delivery month.

The three-month SOFR futures contracts basis point value is $25 per basis point. It also trades in IMM index points. The final settlement prices will be determined by daily compounding of the overnight SOFR rate covering the actual day count for that contract’s interval.

Exchange Calculation Methods

The exchange will apply daily compounding between quarterly IMM dates for the purpose of determining final settlement prices of expiring Three-month SOFR futures.

SOFR futures allow for enhanced price discovery and risk management of short term interest rate product.

{kind=link}