Introduction to Fed Fund Futures

{kind=link}

Federal Funds, Fed Funds for short, are generally a transaction of an unsecured loan of U.S. dollars to a borrower or purchaser that is a depository institution (DI) from a lender or seller that is a DI, foreign bank, government-sponsored enterprise or other eligible entity. These transactions are usually conducted on an overnight or next day (T + 1) basis.

The Federal Reserve Bank of New York (FRBNY) gathers transactional data on Fed Funds daily from participating banks and broker dealers. Using a volume-weighted average, the FRBNY calculates the Effective Fed Funds Rate (EFFR) and publishes this number on its website.

Fed Funds and Overnight Interest Swap (OIS) rates are highly correlated and therefore, many IRS discounting models will use either Fed funds, OIS or both when building a forward discounting curve. In addition, Fed Fund futures are also used for trading and other funding curve risk management strategies.

Fed Fund Futures - Contract Specifications

Fed Fund futures contracts are based on the EFFR rate as reported by the FRBNY. Contracts are listed monthly, extending 36 months or three years out on yield curve.

Fed Fund futures are traded in IMM index terms, that is, as a price rather than a rate. The price is simply the implied rate subtracted from 100. For example, if the average monthly Fed Funds rate for September is 1.20% the futures price would be 100 - 1.20 = 98.800.

At final settlement, Fed Fund futures are cash-settled, there is no physical delivery involved. The final settlement calculation at expiry is the total of all the daily rates published by the FRBNY divided by the total number of days in that month.

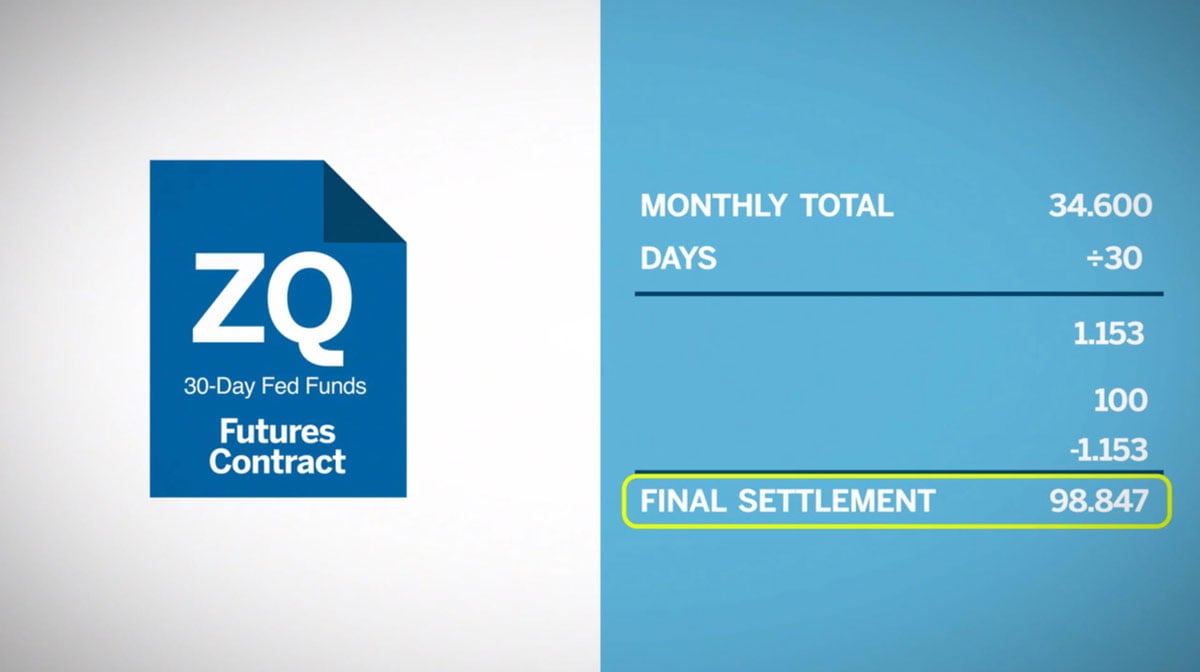

Fed Funds Example

For this example, we will use the September 2017 Fed Funds contract. There are 30 days in the month of September. When we calculate the total of all the reported EFFR rates from FRBNY = 34.600.

You would then divide that by the number of days in the month 34.600 ÷ 30 = 1.153.

Take this number and subtract from 100 you get 100 – 1.153 = 98.847. Therefore, 98.847 was final settlement for the September 2017 Fed Funds futures contract.

{kind=link}

Backward Looking Futures Contract

To determine the final value of a Fed Funds futures contract, one must wait until the end of the contract month to determine its price. In other words, this contract is backward looking. Since the Federal Open Market Committee (FOMC) sets the Fed Fund target rate, the months when there is an FOMC meeting can be very important to contract pricing. But since most FOMC meetings occur mid-month, the first Fed Fund futures contract to be fully affected by a rate change would be the next deferred contract month, rather than the contract in which the meeting takes place.

Summary

Understanding the pricing mechanics of a futures contract is essential to understanding its trading behavior. While the contract construction of Fed Funds futures is simple the market forces that go into its pricing like, FOMC meetings, inflation expectations and employment statistics are sometimes complex and uncertain.