Understanding Convexity Bias

{kind=link}

What is Convexity Bias?

SOFR futures themselves don’t have convexity. It’s instruments that behave like bonds – such as FRAs – that exhibit convexity.

Convexity bias describes the difference between payouts of equivalent SOFR futures and SOFR single period swap positions. This bias in Interest Rate instruments can be observed in how payouts respond to rate changes in the futures market versus the OTC swap market.

The relationship between the SOFR rate and SOFR futures prices

For any given change in the SOFR rate, regardless of direction, the prices of SOFR futures contracts will move inversely and proportionally either up or down. For example, a one basis point rise or fall in the expectations for three-month compounded SOFR would result in the same dollar value change in the futures payout.

If expected rates move up one basis point, the payout of a SOFR futures position would fall by $25 per contract. If expected rates had moved down one basis point instead, the futures payout would increase by $25 per contract. In either case, a one basis point move would result in a $25 variation in payouts for each SOFR futures contract.

With swap agreements, the payout is non-linear – that is, it exhibits convexity. Increases and decreases in the SOFR rate will result in different changes in payouts. The value of a swap rises more for a given decline in rates than the futures value for the same size decline.

{kind=link}

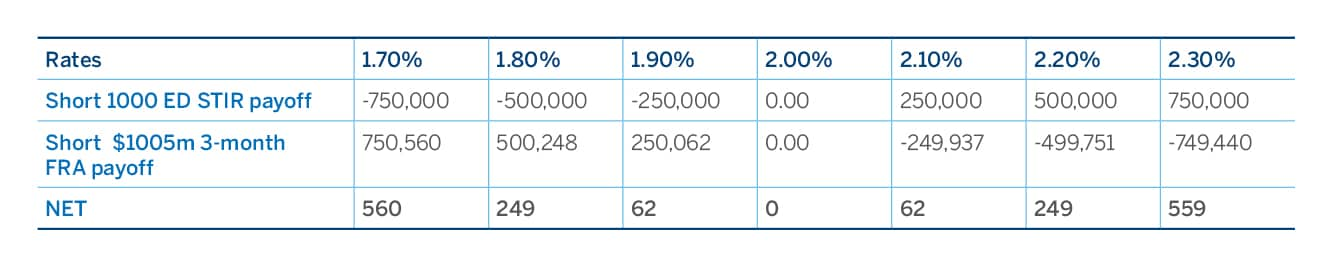

Payout difference in swap agreements vs. SOFR futures

Consider equivalent short positions in SOFR futures and in a SOFR single period swap with a notional of $1009M. As rates decrease 10 basis points from 4.0% to 3.9%, notice the short SOFR futures position decreases in value by $250,000, but the swap payout increases by $250,136.

As rates continue to drop to 3.8% percent and 3.7%, the payout difference continues to increase from $136 to $521, all the way to $1,154. The amount of the convexity is small at the short end of the curve and increases exponentially as you go further down the curve.

SOFR vs. single period swap

| Rates | 3.70% | 3.80% | 3.90% | 4.00% | 4.10% | 4.20% | 4.30% |

| Short 1,000 SOFR Fut. Payout | ($750,000) | ($500,000) | ($250,000) | $- | $250,000 | $500,000 | $750,000 |

| Short $1,009 M 3-month SPS Payout | $751,154 | $500,521 | $250,136 | $- | ($249,889) | ($499,530) | ($748,924) |

| NET | $1,154 | $521 | $136 | $- | $111 | $470 | $1,076 |

Why is convexity important?

Fixed income traders should be aware of the bias because of its effects on larger OTC transactions like swaps that are further out on the yield curve. While the change might only be a few hundred dollars on a short-term swap, changes in a five-year swap could be significantly higher – potentially costing portfolio managers valuable capital.

Still, the SOFR futures markets and the SOFR swap market closely track each other, and arbitrage opportunities keep them from getting too far out of line. For example, EFRP transactions allow traders to exchange a futures position for an equivalent OTC position to increase or decrease convexity and fine tune their portfolio.

For more information about managing these types of positions, visit cmegroup.com/EFRP.