{kind=link}

Understanding SOFR Futures

This note spells out the workings of CME Three-Month SOFR futures and One-Month SOFR futures, examines how they complement the exchange’s established short-term interest rate futures, and discusses intermarket spread trading.1

Contents

1 Secured Overnight Financing Rate

4 CME Three-Month SOFR Futures

9 CME One-Month SOFR Futures

11 Complementarity Between SER and SFR

12 Spread Trading with SOFR Futures

17 Product Codes

Secured Overnight Financing Rate

The Federal Reserve System convened the Alternative Reference Rates Committee (“ARRC”) in November 2014 (i) to identify alternative reference interest rate benchmarks that are firmly based on transactions from a robust underlying market and that comport with the International Organization of Securities Commissions (“IOSCO”) Principles for Financial Benchmarks, and (ii) to formulate a plan to facilitate acceptance and use of the chosen alternative. On 22 June 2017, the ARRC endorsed the Secured Overnight Financing Rate (“SOFR”) as its preferred alternative reference rate. Regular production and publication of SOFR began Tuesday, 3 April 2018.

The SOFR value for any US government securities market business day (“business day”) is published by the Federal Reserve Bank of New York (“FRBNY”) around 8:00 a.m. New York time on the next business day.2 SOFR comprises a broad enough universe of overnight Treasury repo trade activity to make it a benchmark for all seasons, firmly rooted in transaction data from multiple and diverse sources3 --

- Tri-party Treasury general collateral (“GC”) repo transactions cleared and settled by Bank of New York Mellon (“BNYM”), excluding repo transactions made through the Fixed Income Clearing Corporation (“FICC”) General Collateral Financing (“GCF”) repo market, and excluding transactions in which the Federal Reserve is a counterparty.

- Tri-party Treasury GC repo transactions made through the FICC GCF repo market, for which FICC acts as central counterparty.

- Bilateral Treasury repo transactions cleared through the FICC Delivery-versus-Payment (“DVP”) service.

FRBNY applies various filters, trims, and inclusion rules to these data sources to isolate overnight Treasury GC repo transactions from other repo market activity, and to ensure that SOFR adheres to the IOSCO Principles.4 FRBNY then pools them, ranks the aggregate of repo trading volumes by their transaction rates, from lowest to highest, and computes the transaction-weighted median repo rate (ie, the repo rate for which half of the day’s trading volume is transacted at rates that are equal to it or less than it, and for which the other half of the day’s trading volume is made at rates that are equal to it or greater than it). The transaction-weighted median repo rate becomes the day’s SOFR benchmark value.

The trade-volume-weighted median methodology brings at least three advantages. It is a more robust statistic than alternatives such as, e.g., the trade-volume-weighted average. The value it produces, moreover, is almost always an interest rate level that actually has been observed, at which business actually has been conducted. And it aligns with the calculation method for the daily effective federal funds rate (EFFR) and for the daily overnight bank funding rate (OBFR), which was adopted by the Federal Reserve in March 2016.5

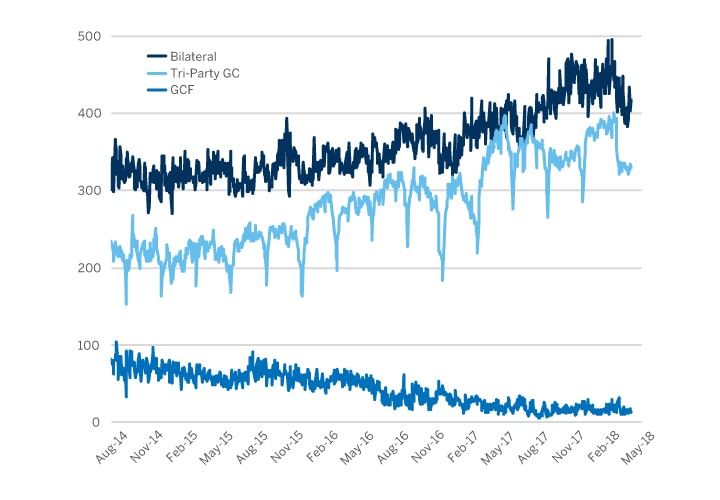

SOFR’s underlying transaction pool is massive. In 2017 average daily trading volumes ran $332 bln in BNYM tri-party Treasury GC repo, $21 bln in FICC GCF Treasury repo, and $393 bln in FICC DVP bilateral Treasury repo, making total average traffic flow of $745 bln per day (Exhibit 1).

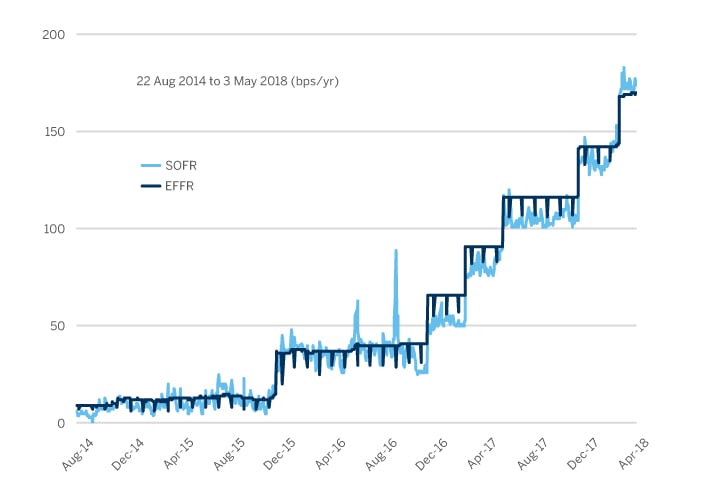

Although the available 3-1/2 years of evidence is limited, the data suggest that SOFR and EFFR share a common trend (Exhibit 2). Their short-term dynamics are quite different, however, with SOFR exhibiting noticeably more volatility. Between September 2014 and April 2018, the median absolute value of daily change in SOFR was one basis point. For EFFR it was zero. In other words, half the time, SOFR rises or falls from its previous daily level by a distance of one basis point or more, while, at least half the time, EFFR doesn’t change from day to day.

Exhibit 1 -- Trade Activity ($ Billions per Day) in SOFR Data Sources, 22 Aug 2014 through 3 May 2018

{kind=link}

Source: FRBNY

Exhibit 2 -- Daily EFFR and Estimated SOFR Values (Basis Points per Annum), 22 Aug 2014 through 3 May 2018

{kind=link}

Source: FRBNY

CME Three-Month SOFR Futures

Exhibit 3 summarizes contract specifications for Three-Month SOFR (“SFR”) futures.

Exhibit 3 -- CME Three-Month SOFR Futures Contract Specifications

| Trading Unit | Compounded daily SOFR interest during contract Reference Quarter, such that each basis point per annum of interest = $25 per contract. Reference Quarter: For a given contract, interval from (and including) 3rd Wed of 3rd month preceding Delivery Month, to (and not including) 3rd Wed of Delivery Month. |

| Price Basis | Contract-grade IMM Index: 100 minus R. R = compounded daily SOFR interest during contract Reference Quarter. Example: Contract price of 97.2950 IMM Index points signifies R = 2.705 percent per annum. |

| Contract Size | $25 per basis point per annum (or $2,500 per contract-grade IMM Index point) |

| Minimum Price Increment (MPI) | Contracts with Four Months or Less Until Termination of Trading: 0.0025 IMM Index points (¼ basis point per annum) equal to $6.25 per contract All Other Contracts: 0.005 IMM Index points (½ basis point per annum) equal to $12.50 per contract |

| Termination of Trading | Last Day of Trading: Exchange Business Day first preceding 3rd Wed of Delivery Month. Termination of Trading: Close of CME Globex trading on Last Day of Trading. |

| Delivery |

By cash settlement, by reference to Final Settlement Price, on 3rd Wed of Delivery Month (or, more generally, first US government securities market business day following Last Day of Trading). R = [ Πi {1+(di /360)*(ri /100)} – 1 ] x (360/D) x 100 n = Number of US government securities market business days in the Reference Quarter i ~ Running variable indexing US government securities market business days during Reference Quarter Πi=1…n denotes the product of values indexed by the running variable, i = 1,2,…,n. ri = SOFR value for ith US government securities market business day di = Number of calendar days to which ri applies D = Σi di (ie, number of calendar days in Reference Quarter) |

| Delivery Months | Nearest 39 March Quarterly months (Mar, Jun, Sep, Dec). For each contract, Contract Month is the month in which the Reference Quarter begins. Example: For a “Sep” contract, Reference Quarter starts on IMM Wed of Sep and ends with Termination of Trading on first US government securities market business day before IMM Wed of Dec, the contract Delivery Month. |

| Trading Venues and Hours | CME Globex and CME ClearPort: 5pm to 4pm, Sun-Fri. |

| CME Globex Algorithm | Allocation (A Algorithm, with Top Order Allocation = 100% and Pro Rata Allocation = 100%) |

| Block Trade Minimum Size |

Asian Trading Hours (4pm–12am, Mon-Fri on regular business days and at all weekend times) 250 contracts European Trading Hours (12am– 7am, Mon-Fri on regular business days) 500 contracts Regular Trading Hours (7am–4pm, Mon-Fri on regular business days) page 3 on pdf 1,000 contracts |

| Product Codes | CME: SR3 Bloomberg: SFR Cmdty |

In certain important ways – contract sizing and critical dates, for instance – the contract features resemble CME’s flagship Three-Month Eurodollar (“ED”) futures.

Contract Critical Dates

The “contract month” convention for naming SFR futures mirrors the established convention for ED futures. To see how, consider two contracts:

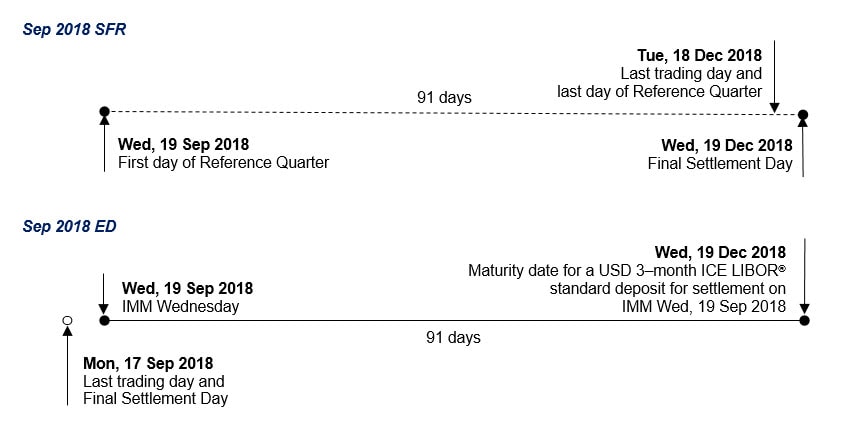

- One is a September 2018 SFR future that comes to final settlement on the third Wednesday of December 2018. The interval of interest rate exposure that informs the contract final settlement price – the contract Reference Quarter -- starts on the third Wednesday of September 2018 and ends on the third Wednesday of December 2018.

- The other is a September 2018 ED future that comes to final settlement on the Monday before the third Wednesday of September 2018. The final settlement price is based on the USD three-month ICE LIBOR ® corresponding to a three-month term unsecured bank funding transaction that settles on the third Wednesday of September 2018 and that matures three months later, in mid-December.

Both are referenced as “September” contracts, and the interval of interest rate exposure for one is essentially the same as for the other. Crucially, the settlement date for the ED contract’s hypothetical three-month term bank funding rate – the third Wednesday of September 2018 – is identical to the start date of the SFR contract’s Reference Quarter, the period over which daily SOFR interest is compounded --

{kind=link}

Last Trading Day

…is the first business day before the 3rd Wednesday of the contract delivery month, ie, the business day first preceding the last day of the contract Reference Quarter. Example: For the September 2018 SFR contract, the scheduled last day of trading is Tuesday, 18 December 2018, as depicted above

Final Settlement Price

…is 100 contract price points minus daily compounded SOFR interest during the contract Reference Quarter, rounded to the nearest 1/100th of one basis point per annum. The exchange computes an expiring contract’s final settlement price on the morning of the third Wednesday of the contract delivery month,6 after FRBNY has published the SOFR value based on trade activity for the final day of the contract’s Reference Quarter (typically the preceding Tuesday, more generally the first preceding business day).

Example: Consider a hypothetical June 2017 SFR contract. The contract Reference Quarter spans 91 days, from (and including) Wednesday, 21 June (the third Wednesday of June), until (and not including) Wednesday, 20 September (the third Wednesday of September). Exhibit 4 details determination of the contract final settlement price on Wednesday, 20 September, when FRBNY would have published the SOFR value for Tuesday, 19 September.

Exhibit 4 -- Daily Compounding of SOFR Values for Hypothetical June 2017 SFR Futures

(Highlighted dates = business days immediately preceding US government securities market holidays)

| Date | Days | SOFR (bps) | Gross Return |

| 21-Jun | 1 | 102 | 1.000028333 |

| 22-Jun | 1 | 102 | 1.000028333 |

| 23-Jun | 3 | 106 | 1.000088333 |

| 26-Jun | 1 | 105 | 1.000029167 |

| 27-Jun | 1 | 103 | 1.000028611 |

| 28-Jun | 1 | 105 | 1.000029167 |

| 29-Jun | 1 | 108 | 1.000030000 |

| 30-Jun | 3 | 121 | 1.000100833 |

| 3-Jul | 2 | 110 | 1.000061111 |

| 5-Jul | 1 | 105 | 1.000029167 |

| 6-Jul | 1 | 103 | 1.000028611 |

| 7-Jul | 3 | 101 | 1.000084167 |

| 10-Jul | 1 | 101 | 1.000028056 |

| 11-Jul | 1 | 101 | 1.000028056 |

| 12-Jul | 1 | 101 | 1.000028056 |

| 13-Jul | 1 | 102 | 1.000028333 |

| 14-Jul | 3 | 102 | 1.000085000 |

| 17-Jul | 1 | 104 | 1.000028889 |

| 18-Jul | 1 | 102 | 1.000028333 |

| 19-Jul | 1 | 101 | 1.000028056 |

| 20-Jul | 1 | 102 | 1.000028333 |

| 21-Jul | 3 | 102 | 1.000085000 |

| 24-Jul | 1 | 105 | 1.000029167 |

| 25-Jul | 1 | 104 | 1.000028889 |

| 26-Jul | 1 | 104 | 1.000028889 |

| 27-Jul | 1 | 105 | 1.000029167 |

| 28-Jul | 3 | 104 | 1.000086667 |

| 31-Jul | 1 | 109 | 1.000030278 |

| 1-Aug | 1 | 103 | 1.000028611 |

| 2-Aug | 1 | 101 | 1.000028056 |

| 3-Aug | 1 | 101 | 1.000028056 |

| 4-Aug | 3 | 101 | 1.000084167 |

| Date | Days | SOFR (bps) | Gross Return |

| 7-Aug | 1 | 101 | 1.000028056 |

| 8-Aug | 1 | 101 | 1.000028056 |

| 9-Aug | 1 | 101 | 1.000028056 |

| 10-Aug | 1 | 103 | 1.000028611 |

| 11-Aug | 3 | 106 | 1.000088333 |

| 14-Aug | 1 | 109 | 1.000030278 |

| 15-Aug | 1 | 112 | 1.000031111 |

| 16-Aug | 1 | 109 | 1.000030278 |

| 17-Aug | 1 | 110 | 1.000030556 |

| 18-Aug | 3 | 108 | 1.000090000 |

| 21-Aug | 1 | 105 | 1.000029167 |

| 22-Aug | 1 | 103 | 1.000028611 |

| 23-Aug | 1 | 103 | 1.000028611 |

| 24-Aug | 1 | 109 | 1.000030278 |

| 25-Aug | 3 | 108 | 1.000090000 |

| 28-Aug | 1 | 106 | 1.000029444 |

| 29-Aug | 1 | 104 | 1.000028889 |

| 30-Aug | 1 | 105 | 1.000029167 |

| 31-Aug | 1 | 115 | 1.000031944 |

| 1-Sep | 4 | 110 | 1.000122222 |

| 5-Sep | 1 | 105 | 1.000029167 |

| 6-Sep | 1 | 103 | 1.000028611 |

| 7-Sep | 1 | 104 | 1.000028889 |

| 8-Sep | 3 | 105 | 1.000087500 |

| 11-Sep | 1 | 105 | 1.000029167 |

| 12-Sep | 1 | 105 | 1.000029167 |

| 13-Sep | 1 | 105 | 1.000029167 |

| 14-Sep | 1 | 109 | 1.000030278 |

| 15-Sep | 3 | 111 | 1.000092500 |

| 18-Sep | 1 | 104 | 1.000028889 |

| 19-Sep | 1 | 101 | 1.000028056 |

| 20-Sep |

Data Source: FRBNY

On each Date:

“Days” =

# days from SOFR trade/settlement day to next business day

“Gross Return” =

1 plus (Days/360) x (SOFR/10000)

Example:

“Gross Return” on Fri, 1 Sep = 1 plus (4/360) x (110/10000) = 1.000122222

Final Settlement Rate:

[ (Product of All Gross Returns) minus 1 ] x (360/91) x 100

Example:

[ 1.002670427 minus 1 ]

x (360/91) x 100 =

1.056432494 pct/yr

Round to the nearest 1/100th bp:

1.0564

Final Settlement Price: 98.9436 = 100 minus 1.0564

As Exhibit 4 suggests, the computational conventions for compounding of daily SOFR values closely resemble those that apply in standard US dollar overnight index swaps (“OIS”), in which each OIS contract’s floating rate leg is based on business-day-compounded EFFR. That is, SOFR will accrue as simple interest over weekends and US government securities market holidays and as compound interest otherwise.7

Futures Final Settlement Prices and SOFR Revisions

FRBNY normally publishes the SOFR value based on “yesterday’s” transaction data at around 8:00am New York time “today”. What happens if later “today” FRBNY discovers errors in those data (as provided to it by either BNYM or DTCC Solutions) or in the calculation process? Or what if transaction data that had been unavailable in time for regular publication at 8:00am “today” were to become available later in the day?

In any such instance, FRBNY may publish a revised SOFR value at approximately 2:30pm New York time, subject to two restrictions: (1) FRBNY will issue a revised SOFR value only on the same day as the initial rate value was published, and no later, and (2) it will issue a revised SOFR value only if the size of the revision – the magnitude of difference between the corrected rate value and the initial rate value that was published earlier that day -- exceeds one basis point per annum. Any time a SOFR value is revised, FRBNY will include a footnote to identify the revision.8

FRBNY’s revision policy interacts with SFR futures final settlement prices in two ways. First, for all but the last business day in an expiring contract’s Reference Quarter, the contract final settlement price calculation will incorporate any revised values that FRBNY has issued. Second, for the last business day of the expiring contract’s Reference Quarter, the SOFR value that enters into calculation of the final settlement price shall be the value first published by FRBNY, irrespective of any revised SOFR value that FRBNY might publish at 2:30pm that day.

Price = 100 Minus Rate

Not just at final settlement but at all times, the SFR contract price takes the familiar IMM Index form, derived by subtracting from 100 the value (either expected or actual) of the contract’s three-month SOFR interest exposure, as described above.

Example: Suppose it is early August. Consider the nearby September SFR contract, which comes to final settlement in December. If the consensus view among market participants is that daily SOFR interest will compound between mid-September and mid-December (ie, during the contract Reference Quarter) at an annualized rate of 2 percent, then the futures contract price should trade at or around 98.00 (equal to 100.00 minus 2.00).

If any newly arrived information or change in market circumstances prompts market participants collectively to expect a rise (or fall) in SOFR by the time of the contract Reference Quarter, then the contract price will fall (or rise).

1 Basis Point = $25

Gains or losses on a contract position are calculated simply by determining the number of interest rate basis points (“bps”) by which the contract price has moved, then multiplying by the value of one bp per contract. As with ED futures, each basis point of contract interest is worth $25. Thus, SFR contract size is $2,500 x the contract IMM Index.

Minimum Price Increment = Either ¼ Bp or ½ Bp

The price of a SFR contract trades in increments of either ¼ bp or ½ bp, depending upon the contract’s proximity to its final settlement date. Generally, the minimum price fluctuation is ½ bp (equal to $12.50 per contract). Each contract’s minimum price fluctuation reduces to ¼ bp (equal to $6.25 per contract), however, as of the first Trade Date following the weekend that precedes the third Wednesday of the month before the contract month. Broadly put, this means each contract will trade in minimum price increment of ¼ bp during the four months before it comes to final settlement.

Example: Consider the September 2018 SFR contract. Its Reference Quarter starts on (and includes) Wednesday, 19 September, and ends on (and excludes) Wednesday, 19 December. Its minimum price increment is ½ bp through close of trading on Friday, 10 August. When trading resumes on Sunday, 12 August, for trade date Monday, 13 August, its minimum price increment is ¼ bp.

Contract Listings = 39 Quarterlies (Whites through Coppers)

SFR listings comprise four March Quarterly (March, June, September, and December) contracts in the nearby “White” year and in each of the deferred “Red”, “Green”, “Blue”, “Gold”, “Purple”, “Orange”, “Pink”, “Silver”, and “Copper” years. Thus, a newly listed SFR contract will be tradable for approximately ten years before it comes to final settlement.

CME One-Month SOFR Futures

The structure of the One-Month SOFR (“SER”) futures contract, summarized in Exhibit 5, resembles the exchange’s 30-Day Federal Funds (“FF”) futures in nearly all respects.

Exhibit 5 -- CME One-Month SOFR Futures Contract Specifications

| Trading Unit | Average daily SOFR interest during futures contract Delivery Month, such that each basis point per annum of interest is worth $41.67 per futures contract. |

| Price Basis | Contract-grade IMM Index: 100 minus R. R = average daily SOFR interest during contract Delivery Month. Example: Contract price of 97.295 IMM Index points signifies R = 2.705 percent per annum. |

| Contract Size | $41.67 per basis point per annum (or $4,167 per contract-grade IMM Index point) |

| Minimum Price Increment (MPI) |

0.005 IMM Index points (½ basis point per annum) equal to $20.835 per contract, provided that :

|

| Termination of Trading | Last Day of Trading: Last Exchange Business Day of contract Delivery Month. Termination of Trading: Close of CME Globex trading on Last Day of Trading. |

| Delivery | By cash settlement, by reference to Final Settlement Price, on first US government securities market business day following Last Day of Trading. Final Settlement Price: Contract-grade IMM Index evaluated at R = arithmetic average of daily SOFR during Delivery Month. |

| Delivery Months | Nearest 13 calendar months. |

| Trading Venues and Hours | CME Globex and CME ClearPort: 5pm to 4pm, Sun-Fri. |

| CME Globex Algorithm | Split FIFO and Pro-Rata (K Algorithm, with Top Order Allocation = 100% and Pro Rata Allocation = 100%) |

| Block Trade Minimum Size |

Asian Trading Hours (4pm–12am, Mon-Fri on regular business days and at all weekend times) 125 contracts European Trading Hours (12am– 7am, Mon-Fri on regular business days) 250 contracts Regular Trading Hours (7am–4pm, Mon-Fri on regular business days) 500 contracts |

| Product Codes | CME: SR1 Bloomberg: SER Cmdty |

Last Trading Day

…is the last business day of the contract delivery month. Example: For October 2018 SER futures, the scheduled last day of trading is Wednesday, 31 October.

Final Settlement Price

…is 100 contract price points minus average daily SOFR interest during the contract delivery month, with the average value rounded to the nearest 1/10th of one bp per annum. Normally, the exchange will compute an expiring contract’s final settlement price on the morning of the first business day following the end of the expiring contract’s delivery month. Example: For October 2018 SER futures, the delivery month ends on (and includes) Wednesday, 31 October, and determination of the final settlement price is scheduled to occur on Thursday, 1 November, after FRBNY has published the SOFR value based on trade activity for Wednesday, 31 October.

Similar to SFR futures, determination of the final settlement price for an expiring SER future will incorporate any revised values that FRBNY publishes for all but the last business day in the contract delivery month. For the delivery month’s last business day, the SOFR value that enters calculation of the final settlement price shall be the value first published by the FRBNY. To be clear, any revised SOFR value such as FRBNY might publish at 2:30pm that day would not enter into the final settlement price.9

Price = 100 Minus Rate

Like FF futures, the SER futures contract price is quoted in IMM Index form, equal to 100 price points minus the expected value of average daily SOFR interest during the contract delivery month.

Example: If market participants generally expect the average level of daily SOFR to be 2.718 percent during the month of October, then the price of October SER futures should trade in the neighborhood of 97.280 or 97.285 (ie, around 97.282, equal to 100.000 minus 2.718). If the October SER futures contract is eligible to trade in ¼ bp minimum price increments, then the price more likely would trade at or around 97.2800 or 97.2825 (as before, either side of 97.282).

1 Basis Point = $41.67

Gains or losses on a contract position are calculated simply by determining the number of bps by which the contract price has moved, then multiplying by the value of one bp. As with FF futures, each bp of contract interest is worth $41.67. Thus, contract size = $4,167 x the contract IMM Index.

Price Increments = Either ¼ Bp or ½ Bp

The SER contract price trades in increments of either ¼ bp or ½ bp, depending on the proximity of the contract final settlement date. As with FF futures, the minimum price increment is ½ bp, worth $20.835 per contract, up to the start of the first day of the Delivery Month. From the first day of the Delivery Month until termination of trading, the contract minimum price increment is ¼ bp, worth $10.4175 per contract.

Additionally, in cases where the first day of the Delivery Month is a Tuesday, Wednesday, Thursday, or Friday, the contract minimum price increment reduces to ¼ bp at the start of CME Globex trading on the Sunday preceding the first day of the Delivery Month.

Examples: For October 2018 SER futures, the first day of the Delivery Month is Monday, 1 October. Thus, the minimum price increment is ½ bp until the start of CME Globex trading on Sunday, 30 September (ie, for trade date Monday, 1 October). From then until termination of trading in the contract, the minimum price increment is ¼ bp.

For August 2018 SER futures, by contrast, the first day of the Delivery Month is Wednesday, 1 August. In this case, the minimum price increment is ½ bp until the start of CME Globex trading on Sunday, 29 July. From that point – the start of the Monday, 30 July, trade date -- until trading terminates in the contract on Friday, 31 August, the minimum price increment is ¼ bp.

Contract Listings = Nearest 13 Serial Calendar Months

At any given time, the Exchange lists 13 contracts for trading, one for each of the 13 nearest calendar months. By implication, a newly-listed SER futures contract trades for 13 months until it goes to final settlement.

Complementarity Between SER and SFR

Prior to the start of the contract’s Reference Quarter, the SFR futures contract rate -- the “Rate” portion of the “100 minus Rate” contract price – gauges market expectation of business-day-compounded SOFR during the Reference Quarter, expressed as an interest rate per annum. After the nearby contract enters its Reference Quarter, the contract rate becomes a mix of (i) known SOFR values, ie, published values for all days from start of the Reference Quarter to the present, and (ii) market expectations of SOFR values for all remaining days in the Reference Quarter that lie ahead.

As the expiring contract progresses through its Reference Quarter, the forward-looking expectational component of its price plays a diminishing role in fair valuation. In general, progressively decreasing uncertainty about the contract’s final settlement price means steadily less contract price volatility.

Market practitioners familiar with 30-Day Federal Funds futures will recognize this quandary immediately. As an expiring FF contract makes its way through its delivery month, contract users know increasingly more of the daily EFFR values that will determine the contract’s final settlement price. Room for price volatility in the contract shrinks accordingly.

Seen in this light, the SER futures strip makes a useful complement to SFR futures for market participants who seek finer granularity in framing expectations of SOFR values, or who seek finer resolution of SOFR volatility, within horizons out to six months or so.

Spread Trading with SOFR Futures

For SFR futures, CME Globex enables trading of standardized intramarket calendar spreads and combinations, largely matching those available for ED futures. Likewise for SER futures, CME Globex intramarket calendar spreads are enabled so as to match those for FF futures.

A diverse array of CME Globex intermarket spreads are available among SFR and SER futures and the incumbent ED and FF futures. These are summarized graphically below and tabularly in Exhibit 6, and are discussed at greater length in the following paragraphs.

{kind=link}

Exhibit 6 – Futures Intermarket Spreads: SOFR, 30-Day Federal Funds, and Three-Month Eurodollars

| Globex Symbol Example | Front Leg | Back Leg | Leg Ratio (# contracts) | Minimum Price Increment (fraction of 1 bp) | Implied Pricing (Y/N) | # Spread Months Listed | |

| SER:FF | July 2018: SR1N8:ZQN8* | SER | FF | 1:1 | 0.25 | N | 1** |

| 0.50 | Y | 6 | |||||

| SFR:ED | September 2018 SR3U8:GEU8* | SFR | ED | 1:1 | 0.25 | N | 1** |

| 0.50 | Y | 19 | |||||

| SER:SFR | (Oct+Nov) vs Sep 2018 SR1V8X8:SR3U8 | SER | SFR | (3+3) : 10 | 0.25 | N | 3 |

| FF:SFR | (Oct+Nov) vs Sep 2018 ZQV8X8:SR3U8 | FF | SFR | (3+3) : 10 | 0.25 | N | 4 |

* For convenience of reference, GE is the CME Globex symbol for ED, ZQ is the CME Globex symbol for FF, SR1 is the CME Globex symbol for SER, and SR3 is the CME Globex symbol for SFR.

** Implied pricing is disabled when the minimum price increments in the nearby futures contract and in the spread are reduced from 0.5 basis points to 0.25 basis points.

Intercommodity Spread Basics

All CME Globex intermarket spreads described here are subject to pro rata trade matching. (For more information, see Appendix -- Technical Details of SOFR Inter-Commodity Spreads on CME Globex.)

The SER:FF spread comprises purchase (sale) of one One-Month SOFR futures contract and sale (purchase) of one 30-Day Federal Funds futures contract. Each leg is weighted at $41.67 per bp in the corresponding underlying interest rate.

Similarly, the SFR:ED spread consists of the purchase (sale) of one Three-Month SOFR future and the sale (purchase) of one Three-Month Eurodollar future, with each leg weighted at $25 per bp in the respective underlying interest rate.

As Exhibit 6 indicates, implied pricing functionality links the liquidity between the CME Globex order book for either of these spreads – SER:FF or SFR:ED -- and the order books for outright trades in the component contracts. Worth note is that implied pricing applies in these spreads only when the component contracts are trading in minimum price increments of 0.5 bps. Specifically –

- For the seven delivery months for which CME Globex SER:FF intermarket spreads are listed, implied pricing applies to all but the nearby month, for which both the nearby SER contract and the nearby FF contract trade in minimum price increments of ¼ bp.

- For the 20 March Quarterly contract months for which CME Globex SFR:ED intermarket spreads are listed, implied pricing applies to all but the nearby contract month, when the SFR contract trades in minimum price increment of ¼ bp.

For each of the three spreads involving futures with different basis point values, the corresponding CME Globex intermarket spread is standardized so that each leg is weighted at $250 per basis point. For instance, the SER:SFR spread comprises purchase (sale) of six SER futures (six contracts x $41.67 per bp per contract) and sale (purchase) of 10 SFR futures (10 contracts x $25 per bp per contract).

Additionally, the one-month contract leg (either FF futures or SER futures) is split between two different futures delivery months so as to approximate coverage of the period of interest rate exposure embodied in the three-month contract leg.

Example: Consider a September 2018 SER:SFR spread (SR1V8X8:SR3U8 in CME Globex symbology). On the front leg, the SER position consists of purchase (sale) of three each of October and November futures. The back leg is a sale (purchase) of 10 September 2018 SFR contracts, for which the Reference Quarter spans from 19 September through 18 December (ie, from IMM Wednesday in September through the Tuesday before IMM Wednesday in December). In effect, the SER contracts in the front leg are distributed so as to encompass the inner two months of the three-month interest rate exposure period in the SFR position.

The same construction and proportions apply to the CME Globex standardized FF:SFR spread and FF:ED spread (the latter of which was introduced in March 2018).

One-Month SOFR Futures and 30-Day Federal Funds Futures

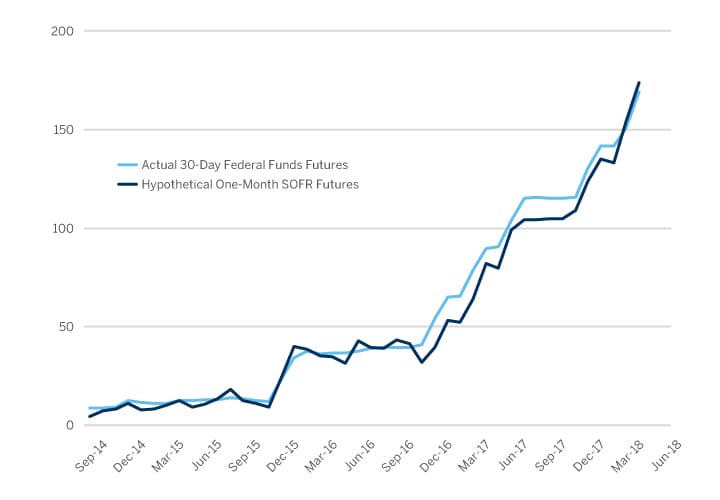

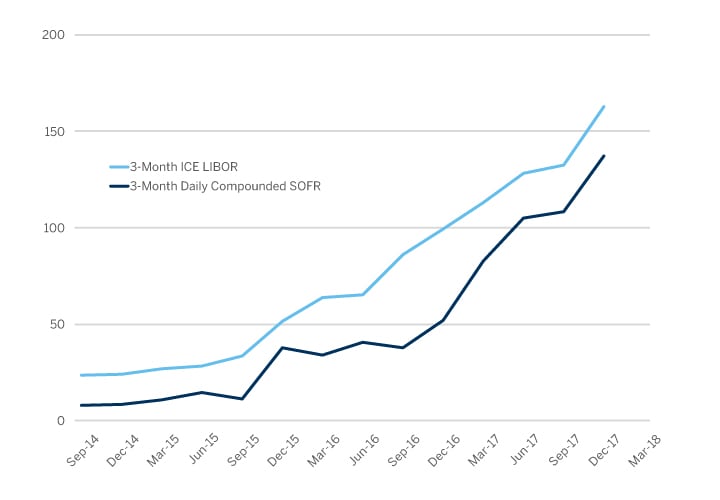

For the CME Globex SER:FF spread, the price display convention is “SER price minus FF price”. To the extent that the SOFR values underlying the SER contract are typically lower than the EFFR values underlying the FF contract, SER:FF spread values typically will be positive. Example: The hypothetical SER contract final settlement price and the actual FF final settlement price for the September 2017 contract month imply a price spread of 9.9 basis points: SERU7 minus FFU7 = 98.946 minus 98.847 = 0.099 price points = 9.9 bps.

The gray line in Exhibit 7 traces the contract rates at futures final settlement for FF for each of the 44 months between September 2014 and April 2018, inclusive. The blue line in Exhibit 7 is the outcome, if the same calculation is applied to obtain the arithmetic average of estimated historical daily SOFR values for each those same months.10

Exhibit 7 -- Contract Interest Rates at Futures Final Settlement (Basis Points per Year): Actual FF and Hypothetical SER, Sep 2014 through Apr 2018

{kind=link}

Source: FRBNY, CMEG calculations

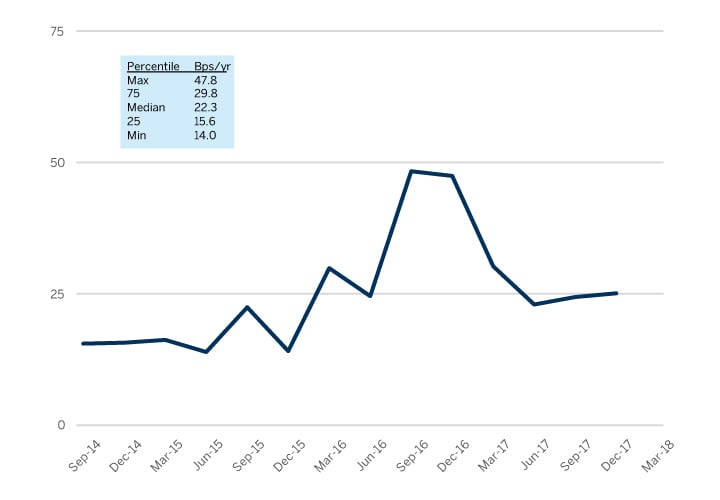

Although month-averaging smooths much of SOFR’s comparatively lively day-to-day volatility, at least some residual effect persists. In Exhibit 7, the median absolute change from one month-average level to the next is 0.8 bps for EFFR. By contrast, it is 3.1 bps for SOFR, nearly four times more volatile.

Exhibit 8 highlights two other comparative features that warrant mention --

- Over the entire 44-month span, monthly SOFR levels normally run 2.6 bps below monthly EFFR.

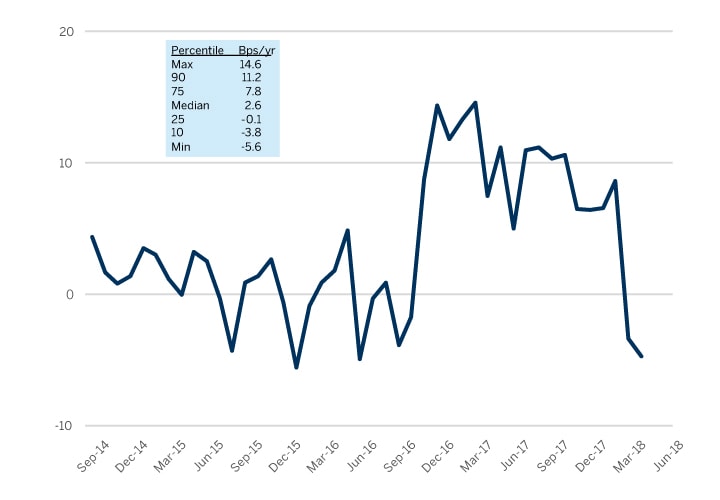

- Occasionally, anomalies in daily SOFR volatility are large enough to exert impact on month-average SOFR. During the final weeks of June and September 2016, for example, Treasury GC repo rates spiked, causing the usually positive SOFR-EFFR interest rate spread to flip temporarily, with month-average SOFR exceeding the corresponding month-average EFFR by 4.9 bps in June and 3.9 bps in September.

Exhibit 8 -- Contract Interest Rate Spreads at Futures Final Settlement (Basis Points per Annum): Actual FF minus Hypothetical SER, Sep 2014 through Apr 2018

{kind=link}

Source: FRBNY, CMEG calculations

Three-Month SOFR Futures and Three-Month Eurodollar Futures

CME Globex SFR:ED intermarket spreads are enabled for each of the 20 contract months for which SFR is listed for trading. Eg, at SFR launch on 7 May, contract months for SFR:ED spreads span from June 2018 through March 2023, inclusive. Here too, the price display convention is “SFR price minus ED price."

These should furnish a clear view of the market assessment of the term structure of basis spreads between forward-starting 3-month SOFR OIS fixed rates and the corresponding forward-starting 3-month Eurodollar deposit rates. Exhibit 9 depicts the corresponding futures contract final settlement rates, and Exhibit 10 shows the corresponding interest rate spreads, for each of the 14 March Quarterly contract months between September 2014 and December 2017, inclusive.

Exhibit 9 -- Futures Contract Final Settlement Rates (Basis Points per Year): Actual ED and Hypothetical SFR, Sep 2014 through Dec 2017

{kind=link}

Data Sources: ICE Benchmark Administration Limited, FRBNY, CMEG calculations

Exhibit 10 -- Contract Final Settlement Rate Spreads (Basis Points per Annum): Actual ED minus Hypothetical SFR, Sep 2014 through Dec 2017

{kind=link}

Data Sources: ICE Benchmark Administration Limited, FRBNY, CMEG calculations

Product Codes

| Three-Month SOFR Futures | One-Month SOFR Futures | |

| CME Globex | SR3 | SR1 |

| Bloomberg | SFR Comdty | SER Comdty |

| Broadway Technology | SR3 | SR1 |

| CQG | SR3 | SR1 |

| Fidessa | SR3 | SR1 |

| FIS/SunGard | SR3 | SR1 |

| ION (Pats & FFastFill) | SR3 | SR1 |

| Reuters Globex Chain RICs | 0#1SRA: | 0#1S1R: |

| Reuters Composite Chain RICs | 0#SRA: | 0#S1R: |

| TT | SR3 | SR1 |

Appendix -- Technical Details of SOFR Inter-Commodity Spreads on CME Globex

| Product | MDP 3.0: tag 6937-Asset |

iLink: tag 55-Symbol MDP 3.0 tag 1151 – Security Group |

Future Tag 762-Security SubType |

MDP 3.0 Market Data Channel |

|

30-Day Fed Funds future vs 1-Month SOFR [text-align: right] |

SR1 [text-align: center] |

SY [text-align: center] |

IS [text-align: center] |

312 [text-align: center] |

|

Eurodollar future vs 3-Month SOFR future [text-align: right] |

SR3 [text-align: center] |

SS [text-align: center] |

IS [text-align: center] |

312 [text-align: center] |

|

1-Month SOFR future vs 3-Month SOFR future [text-align: right] |

SR1 [text-align: center] |

SS [text-align: center] |

EF [text-align: center] |

312 [text-align: center] |

|

30-Day Fed Funds future vs 3-Month SOFR future [text-align: right] |

ZQ [text-align: center] |

SY [text-align: center] |

EF [text-align: center] |

348 [text-align: center] |

Contact Us

For more information about SOFR and CME SOFR futures, please visit www.cmegroup.com/sofr or contact interestrates@cmegroup.com.

1. For more about SOFR and intermarket spreading applications, see What is SOFR?, 16 March 2018, which is available at http://www.cmegroup.com/education/articles-and-reports/what-is-sofr.html, and Spreading SOFR, FF and ED Futures, 4 April 2018, which is available at http://www.cmegroup.com/education/spreading-sofr-ff-and-ed-futures.html.

2. For SOFR data, and for more information about SOFR, visit FRBNY, Treasury Repo Reference Rates, at: https://www.newyorkfed.org/markets/treasury-repo-reference-rates and see Statement Regarding the Initial Publication of Treasury Repo Reference Rates, Statements and Operating Policies, 28 February 2018, which is available at: https://www.newyorkfed.org/markets/opolicy/operating_policy_180228

3. See Federal Reserve System, Request for Information Relating to Production of Rates, 82 FR 41259, 30 August 2017, which includes a detailed overview of the Treasury repo market, and which is available at: https://www.federalregister.gov/documents/2017/08/30/2017-18402/request-for-information-relating-to-production-of-rates

4. See Frost, Joshua, Presentation at the Alternative Reference Rates Committee Roundtable, FRBNY, New York, 8 November 2017, which is available at: https://www.newyorkfed.org/newsevents/speeches/2017/fro171108; and Lorie K Logan, The Role of the New York Fed as Administrator and Producer of Reference Rates, Remarks at the Annual Primary Dealer Meeting, FRBNY, New York, January 9, 2018, which is available at: https://www.newyorkfed.org/newsevents/speeches/2018/log180109

5. See FRBNY, Statement Regarding the Calculation Methodology for the Effective Federal Funds Rate and Overnight Bank Funding Rate, Operating Policy Statement, 8 July 2015, which is available at: https://www.newyorkfed.org/markets/opolicy/operating_policy_150708

6. Or on the next following business day, if the third Wednesday happens to be a US government securities market holiday.

7. EFFR and SOFR are subject to slightly different holiday schedules –

For EFFR, FRBNY produces a value for every weekday, excluding days on which the Fedwire Funds Service is closed (https://www.federalreserve.gov/paymentsystems/fedfunds_about.htm). As a rule, such excluded days also are identified as banking holidays by FRBNY (https://www.cmegroup.com/aboutthefed/holiday_schedule.html).

For SOFR, FRBNY produces a value for every weekday, excluding days recommended by SIFMA for observance as US government securities market holidays. The SIFMA holiday calendar includes all Fedwire Funds Service holidays, plus Good Friday and any ad hoc National Day of Mourning. See https://www.sifma.org/resources/general/holiday-schedule/ and https://www.sifma.org/wp-content/uploads/2017/11/market-response-statement.pdf

8. See FRBNY, Additional Information about the TGCR, BGCR, and SOFR, addendum to Statement on Treasury Repo Reference Rates, Operating Policy Statement, 16 April 2018, which is available at: https://www.newyorkfed.org/markets/treasury-repo-reference-rates-information

9. It warrants emphasis that different holiday schedules apply to EFFR and SOFR. See Footnote 6.

10. Historical daily values of the SOFR are as estimated and published by FRBNY. See https://apps.newyorkfed.org/markets/autorates/~/media/b0b4d847295143f9858c6fb946412f00.ashx

SOFR Home

Return to the SOFR homepage for more information regarding contract specs, educational resources, and more.