{kind=link}

Trading SOFR Options

Following the successful launch of SOFR futures on 7 May 2018, liquidity, price discovery, volume and open interest of SOFR futures have developed such that Options on Three-Month SOFR futures are the natural next step in the development of the SOFR ecosystem. On 6 January 2020, CME launched Options on Three-Month SOFR futures (SOFR Options).1 SOFR Options can be executed on three venues: open outcry, CME Globex, and as a block trade submitted via CME ClearPort. Each of these platforms offer customers access to deep and diverse pools of liquidity.

In nearly all respects, the design of SOFR Options mirror Options on Three-Month Eurodollar futures (Eurodollar Options). This paper provides in-depth descriptions of SOFR Options:

- Product Suite

- Contract Specifications

- Comparing Three-Month SOFR and Eurodollar Futures Volatility

- Spreading SOFR and Eurodollar Options

Product Suite

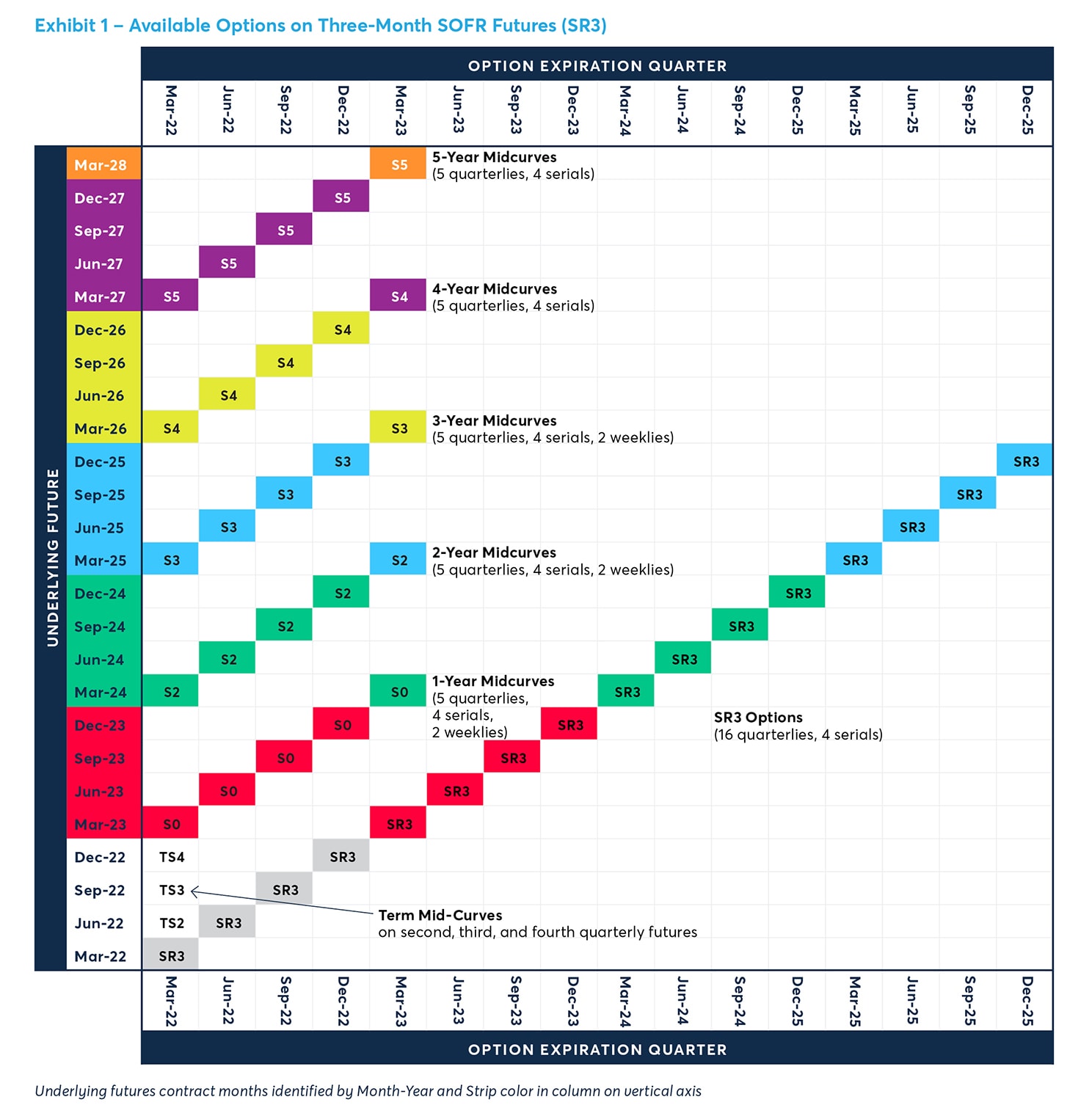

The Option contract listing calendar –generally– is as follows:

- Quarterly Standard Options (SR3) expiring in each of the nearest 16 March Quarterly months (March, June, September, December); Serial Standard Options (SR3) expiring in each of the nearest 4 non-March Quarterly months (January, February, April, May, July, August, October, November);

- Quarterly One-Year (S0) Two-Year (S2), Three-Year (S3), Four-Year (S4), and Five-Year (S5), Mid-Curve Options expiring in each of the nearest 5 March Quarterly months; Serial One-Year, Two-Year, Three-Year, Four-Year, and Five-Year Mid-Curve Options expiring in each of the nearest 4 non-March Quarterly months; and

- Quarterly Three-Month, Six-Month, and Nine-Month Mid-Curve Options expiring in the nearest March Quarterly month. Serial Three-Month, Six-Month, and Nine-Month Mid-Curve Options expiring in each of the nearest 2 non-March Quarterly months; and

- Weekly One-Year, Two-Year, and Three-Year Mid-Curve Options expiring on each of the nearest 2 Fridays not scheduled for expiration of Quarterly or Serial Options.

Please refer to the table (Exhibit 1) below for the complete array of SOFR Options, including commodity codes and underlying futures contract months.

{kind=link}

Contract Specifications

Exhibit 2 summarizes contract specifications. In general, the range of products comprised within the Option product suite, the corresponding listing calendars, and the Option contract features closely mimic the CME’s extant suite of Eurodollar Options. As discussed below, noteworthy differences will be the schedule for termination of trading in expiring Options, conventions for designation of an Option’s underlying instrument.

Exhibit 2

Contract Specifications for Options on CME Three-Month SOFR Futures

(All times of day are Central time.)

| Underlying Instrument | Each Option is exercisable into one (1) specified CME Three-Month SOFR futures contract. |

| Expiries | Quarterly Standard Options: March Quarterly months (Mar, Jun, Sep, Dec) Serial Standard Options: Non-March Quarterly months (Jan, Feb, Apr, May, Jul, Aug, Oct, Nov) Quarterly One-, Two-, Three-, Four-, and Five-Year Mid-Curve Options: March Quarterly months Serial One-, Two-, Three-, Four-, and Five-Year Mid-Curve Options: Non-March Quarterly months Weekly One-, Two-, and Three-Year Mid-Curve Options: Specified Fridays Quarterly Three-, Six-, and Nine-Month Mid-Curve Options: March Quarterly months Serial Three-, Six-, and Nine-Month Mid-Curve Options: Non-March Quarterly months |

| Exercise Price Arrays | For options expiring on a given date, for exercise into a given Underlying Instrument, exercise prices at all integer multiples of 0.25 Underlying Instrument price points (“points” or “price points”) from 5.50 points above to 5.50 points below current at-the-money exercise price, and at all integer multiples of 0.125 points from 1.50 points above to 1.50 points below current at-the-money exercise price. At-the-money exercise price is the Option exercise price closest to previous daily settlement price of the option’s Underlying Instrument. |

| Minimum Option Premium Increment | Quoted in Underlying Instrument price points, at $2,500 per point per Option contract, as follows: Outright -- Quarterly Standard Options expiring in nearest March Quarterly Month 0.0025 points ($6.25 per contract) if Option is for nearest monthly Option expiration date, else 0.0025 points ($6.25 per contract) if Option premium is not greater than 0.05 points, and 0.005 points ($12.50 per contract) if Option premium is greater than 0.05 points. Outright -- Quarterly Standard Options expiring in second-nearest March Quarterly Month, Serial Standard Options, and all Three-Month Mid-Curve Options 0.0025 points ($6.25 per contract) if Option premium is not greater than 0.05 points, and 0.005 points ($12.50 per contract) if Option premium is greater than 0.05 points. Outright -- All other Quarterly Standard Options, and all other Mid-Curve Options 0.005 points ($12.50 per contract), with Cabinet = 0.0025 points ($6.25 per contract). Option Spreads/Combinations 0.005 points, provided that it is 0.0025 points if: (1) spread/combination comprises only Quarterly Standard Options expiring in nearest March Quarterly month, and any component Option contract is for nearest monthly Option expiration date, or (2) spread/combination trades at net premium not greater than 0.05 points and not less than -0.05 points, and any component Option contract is a Quarterly Standard Option expiring in nearest or second-nearest March Quarterly Month, or a Serial Standard Options, or a Three-Month Mid-Curve Option. |

| Termination of Trading | Trading in expiring Options terminates at close of trading – typically 4pm -- on Last Day of Trading. For all Options excluding Weekly Mid-Curve Options, Last Day of Trading is the Friday preceding the 3rd Wednesday of Option expiry month. For Weekly Mid-Curve Options, Last Day of Trading is any Friday not scheduled for expiration of any Quarterly Standard Option or Serial Standard Option. |

| Option Exercise | American Style. Option may be exercised by purchaser on any day that Option is traded. Option purchaser’s clearing member firm must notify CME Clearing of intention to exercise no later than 5:30pm on day of exercise. All expiring Options outstanding and unexercised at Termination of Trading shall expire at 5:30pm on Last Day of Trading and, absent contrary instruction, shall be automatically exercised. |

| Position Accountability and Reportability | Reportability threshold: 850 contracts for Quarterly Standard Options and Serial Standard Options, and 25 contracts for all other. Single-Month and All-Month Accountability thresholds: 10,000 contracts. |

| Trading Hours and Venue | Open Outcry: 7:20am to 2pm, Mon-Fri CME Globex: 5pm to 4pm, Sun-Fri. Options shall trade on and according to the rules of Chicago Mercantile Exchange, pending certification of contract terms and conditions with the US Commodity Futures Trading Commission. |

| CME Globex Algorithm | Threshold Pro-Rata with Lead Market Maker (LMM) (Q Algorithm). Top Order Allocation = 25%. Top Order Min = 50 contracts. Top Order Max = 1,500 contracts. |

| Block Trade Minimum | 1,250 contracts in Asian Trading Hours (4pm–12am, Mon-Fri on Business Days and at all weekend times) 2,500 contracts in European Trading Hours (12am– 7am, Mon-Fri on Business Days) 5,000 contracts in Regular Trading Hours (7am–4pm, Mon-Fri on Business Days) |

| Commodity Code | Quarterly Standard Options and Serial Standard Options: SR3 Three-Month Mid-Curve Options: TS2 Six-Month Mid-Curve Options: TS3 Nine-Month Mid-Curve Options: TS4 One-Year Mid-Curve Options: S0 (“S zero”) Weekly One-Year Mid-Curve options: S01, S02, S03, S04, S05 (“S zero one” … ) Two-Year Mid-Curve Options: S2 Weekly Two-Year Mid-Curve Options: S21, S22, S23, S24, S25 Three-Year Mid-Curve Options: S3 Weekly Three-Year Mid-Curve Options: S31, S32, S33, S34, S35 Four-Year Mid-Curve Options: S4 Five-Year Mid-Curve Options: S5 |

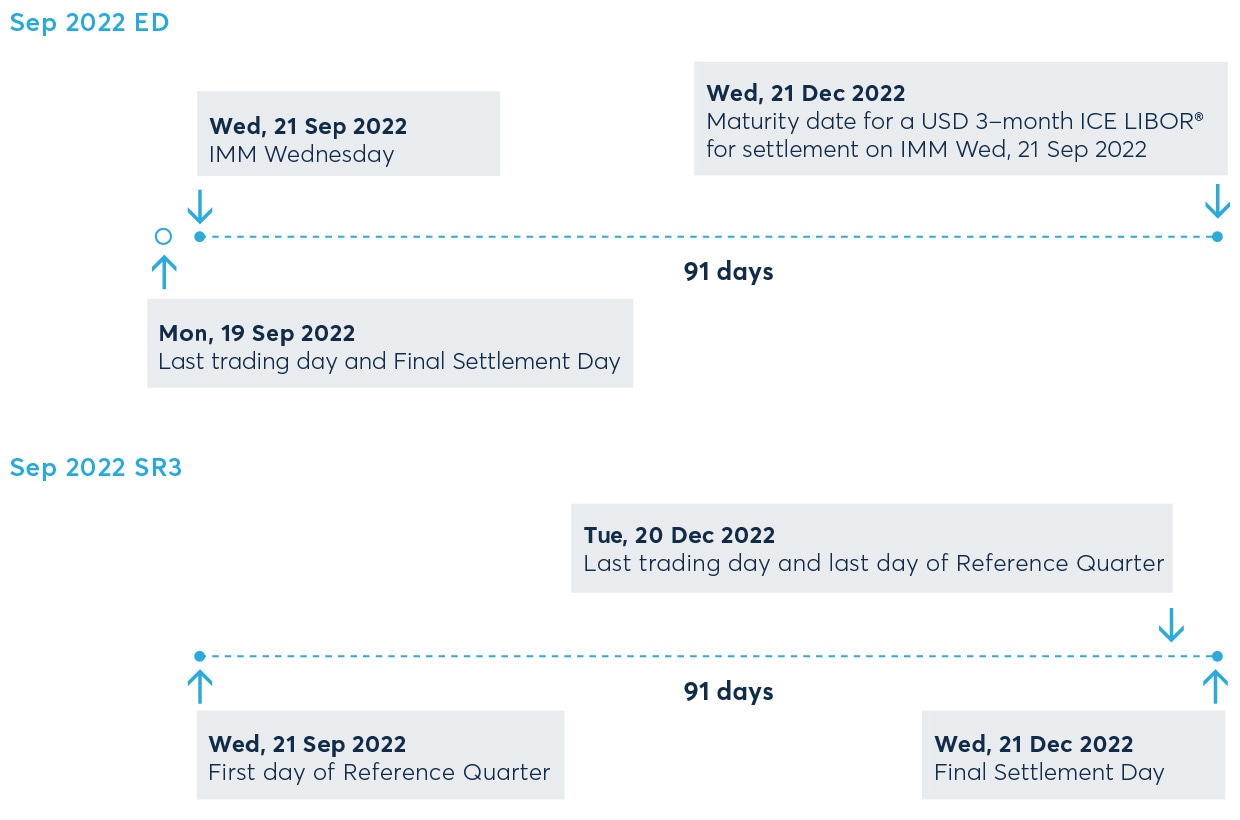

Termination of Trading

Termination of trading in any expiring Option is scheduled to occur at close of trading on a specified Friday. For any Quarterly Standard, Serial Standard, Quarterly Mid-Curve, or Serial Mid-Curve Option, for instance, this typically is the close of CME Globex trading on the Friday before the third Wednesday of the Option’s designated month of expiry.

In the case of Quarterly Standard Options, this contrasts to Quarterly Standard options on CME Three-Month Eurodollar futures, for which termination of trading in any option is scheduled to coincide with termination of trading in the corresponding underlying Three-Month Eurodollar futures contract (scheduled at 11am London time, generally 5am Central time, on the Monday before the third Wednesday of the contract month specified for both the options and the underlying futures).

Underlying Instrument

Each Option is exercisable into a specified CME Three-Month SOFR futures (“futures”) contract. The schedule of futures contract critical dates plays a pivotal role in determining which futures contract is designated to serve as the Option’s underlying instrument.

To see how, consider a hypothetical future that comes to final settlement in December. Its final settlement price is determined on the basis of the rate per annum of daily compounded SOFR interest (in accordance with CME Rule 46003.A.) during the futures contract’s Reference Quarter, the interval beginning on (and including) the third Wednesday of the previous September and ending on (and excluding) the third Wednesday of December.[1] In the nomenclature used by the Exchange to describe its Three-Month SOFR futures listings, this hypothetical futures contract would be referenced as a “September” contract (ie, in terms of the month in which its Reference Quarter begins) and not as a “December” contract.

Crucially, any Option will be associated with its underlying futures contract in terms of the month in which the futures contract Reference Quarter begins. It follows that any Option is exercisable into a futures contract with at least three months of remaining term to final settlement beyond such Option’s expiration date:

- A Serial Standard Option (as summarized in Exhibit 2) scheduled to expire in October or November is specified to exercise into the “December” futures contract for which the Reference Quarter starts on (and includes) the third Wednesday of December and ends on (and excludes) the third Wednesday of the following March.

- A Serial Standard Option scheduled to expire in the preceding July or August is exercisable into the “September” futures contract for which the Reference Quarter starts on (and includes) the third Wednesday of September and ends on (and excludes) the third Wednesday of December.

- A Quarterly Standard Option (as summarized in Exhibit 2) scheduled to expire in September also is specified for exercise into the “September” futures contract for which the Reference Quarter spans from third Wednesday of September to third Wednesday of December.

By contrast, the adjacent Quarterly Standard option on CME Three-Month Eurodollar futures scheduled to expire in September, would be exercisable into the expiring September Three-Month Eurodollar futures contract, which comes to final settlement on the same day as the option comes to expiration, final exercise, and assignment.

Both are referenced as “September” contracts, and the interval of interest rate exposure for one is essentially the same as for the other. Crucially, the settlement date for the Three-Month Eurodollar future (ED) contract’s hypothetical three-month term bank funding rate – the third Wednesday of September 2022 – is identical to the start date of the Three-Month SOFR future (SFR) contract’s Reference Quarter, the period over which daily SOFR interest is compounded –

{kind=link}

Exercise Price Arrays

SOFR Options futures offer exercise prices in increments of 25 basis points (0.25 IMM Index point), 12.5 basis points (0.125 IMM Index point), and 6.25 basis points (.0626 IMM Index point).

The exercise prices for the 25 basis point increments are listed daily 550 basis points (5.50 IMM Index points) above and below the nearest-to-the-money exercise price. For example, assume the prior day’s activity produced a nearest-to-the-money exercise price of 95.00. The 25 basis point increments would have produced a highest exercise price of 100.50 and the following exercise prices that are 100 basis points (1.00 IMM Index point) above the nearest-to-the-money: 95.25, 95.50, 95.75, 96.00. The 25 basis point increments would have produced a lowest exercise price of 89.50 and the following exercise prices that are 100 basis points (1.00 IMM Index point) below the nearest-to-the-money: 94.75, 94.50, 94.25, 94.00.

The exercise prices for the 12.5 basis point increments are listed daily 150 basis points (1.50 IMM Index points) above and below the nearest-to-the-money exercise price. For example, assume the prior day’s activity produced a nearest-to-the-money exercise price of 95.00. The 12.5 basis point increments would have produced a highest exercise price of 96.50 and the following exercise prices that are 50 basis points (0.50 IMM Index point) above the nearest-to-the-money: 95.125, 95.25, 95.375, 95.50. The 12.5 basis point increments would have produced a lowest exercise price of 93.50 and the following exercise prices that are 50 basis points (0.50 IMM Index point) below the nearest-to-the-money: 94.875, 94.75, 94.625, 94.50. As determined by the Exchange, additional exercise prices of 6.25 are made available to trade in shorter dated expirations.

Minimum Option Premium Increment

For users of Eurodollar Options, the pricing of SOFR Options will be familiar. They are based on 100 basis points (1.00 IMM Index point) representing $2500 per contract. Equally, 0.01 IMM Index point represents $25 per contract.

Generally, with a few exceptions, the smallest price increment for SOFR Options are a ½ basis point (0.005 IMM Index point) equal to $12.50 per contract.

Options in the nearest expiring contract month may be quoted in price increments of ¼ basis point (0.0025 IMM Index point) equal to $6.25 per contract. Additionally, some spreads may be quoted in price increments of ¼ basis point. Please refer to the Option Spreads/Combinations of the Minimum Option Premium Increment section of the Contract Specifications (Exhibit 2).

Option Exercise

SOFR Options utilize the American Style option exercise. Therefore, the option buyer has the right to exercise the option on any day they are traded.

Comparing Three-Month SOFR and Eurodollar Futures Volatility

Traders should be mindful of potential differences in SOFR and Eurodollar volatilities as they are developing option pricing models. Based upon Three-Month SOFR and Eurodollar futures price data from Jun 2018-Dec 2021, the rolling front month and fifth quarterly contract months produced the following historical volatilities (annualized) and correlation of daily price changes:

Exhibit 3

Three-Month SOFR and Eurodollar Futures, Historical Volatility and Correlation

| Product | Product Code | Q1 | Q5 |

| Historical Volatility | |||

| Three-Month Eurodollar Futures | ED | 19% | 24% |

| Three-Month SOFR Futures | SR3 | 18% | 23% |

| Correlation | |||

| 0.676 | 0.921 | ||

Q1 and Q5 are rolling front month and fifth quarterly contract months.

Data source: CME Group

Note the historical volatilities were very similar, differing by only one percentage point in each case. However, the difference in correlation between the first (0.676) and the fifth (0.921) quarterly futures contract months suggests as you get closer to expiration the differences in these underlying interest rates become more pronounced. SOFR and Eurodollar markets become more complementary.

Spreading SOFR and Eurodollar Options

Since the launch of SOFR futures, CME Group has experienced significant spreading of our adjacent STIR futures. Similarly, the launch of SOFR Options will create an increasing number of spreading opportunities for relative value traders. Market participants can execute spreads between SOFR and Eurodollar Options on one of three venues: in open outcry, on CME Globex, and as a block trade submitted on CME ClearPort.

Customized spreads may be created on CME Globex using the Exchange’s User Defined Spread (UDS) functionality. The image below demonstrates two types of UDS created on CME Direct prior to launch that might be active.

Exhibit 4

SOFR Option Spreads on Globex

{kind=link}

On Globex users have the ability to create strategies across all SOFR Options including Inter-Commodity spreads consisting of SOFR and Eurodollars together.

- The top strategy is a spread buying a Eurodollar March 22 Call and selling a SOFR March 22 Call.

- The bottom strategy is an example of a SOFR 2-Year Mid Curve put spread vs a SOFR 1-Year Mid Curve Put.

Appendix

Please refer to the table below (Exhibit 5) for each of the associated product codes for SOFR Options.

Exhibit 5

Options on CME Three-Month SOFR Futures –Scope of Product Suite

The Exchange has entered into an agreement with ICE Benchmark Administration Limited which permits the Exchange to use ICE LIBOR as the basis for settling Three–Month Eurodollar futures contracts and to refer to ICE LIBOR in connection with creating, marketing, trading, clearing, settling and promoting Three–Month Eurodollar futures contracts.

Three–Month Eurodollar futures contracts are not in any way sponsored, endorsed, sold or promoted by ICE Benchmark Administration Limited, and ICE Benchmark Administration Limited, has no obligation or liability in connection with the trading of any such contracts. ICE LIBOR is compiled and calculated solely by ICE Benchmark Administration Limited. However, ICE Benchmark Administration Limited, shall not be liable (whether in negligence or otherwise) to any person for any error in ICE LIBOR, and ICE Benchmark Administration Limited, shall not be under any obligation to advise any person of any error therein.

ICE BENCHMARK ADMINISTRATION LIMITED MAKES NO WARRANTY, EXPRESS OR IMPLIED, EITHER AS TO THE RESULTS TO BE OBTAINED FROM THE USE OF ICE LIBOR AND/OR THE FIGURE AT WHICH ICE LIBOR STANDS AT ANY PARTICULAR TIME ON ANY PARTICULAR DAY OR OTHERWISE. ICE BENCHMARK ADMINISTRATION LIMITED MAKES NO EXPRESS OR IMPLIED WARRANTIES OF MERCHANTABILITY OR FITNESS FOR A PARTICULAR PURPOSE FOR USE WITH RESPECT TO THREE–MONTH EURODOLLAR FUTURES CONTRACTS.

Neither futures trading nor swaps trading are suitable for all investors, and each involves the risk of loss. Swaps trading should only be undertaken by investors who are Eligible Contract Participants (ECPs) within the meaning of Section 1a(18) of the Commodity Exchange Act. Futures and swaps each are leveraged investments and, because only a percentage of a contract's value is required to trade, it is possible to lose more than the amount of money deposited for either a futures or swaps position. Therefore, traders should only use funds that they can afford to lose without affecting their lifestyles and only a portion of those funds should be devoted to any one trade because traders cannot expect to profit on every trade. All references to options refer to options on futures.

Any research views expressed those of the individual author and do not necessarily represent the views of the CME Group or its affiliates. The information within this presentation has been compiled by CME Group for general purposes only. CME Group assumes no responsibility for any errors or omissions. All examples are hypothetical situations, used for explanation purposes only, and should not be considered investment advice or the results of actual market experience.

All matters pertaining to rules and specifications herein are made subject to and are superseded by official rulebook of the organizations. Current rules should be consulted in all cases concerning contract specifications

CME Group is a trademark of CME Group Inc. The Globe Logo, CME, Globex and Chicago Mercantile Exchange are trademarks of Chicago Mercantile Exchange Inc. CBOT and the Chicago Board of Trade are trademarks of the Board of Trade of the City of Chicago, Inc. NYMEX, New York Mercantile Exchange and ClearPort are registered trademarks of New York Mercantile Exchange, Inc. COMEX is a trademark of Commodity Exchange, Inc. All other trademarks are the property of their respective owners.

Copyright © 2019 CME Group. All rights reserved.

SOFR options

Explore SOFR options for more information on contract specs, educational resources, and more.