{kind=link}

Substitution among Platinum Group Metals

The opinions expressed in this report are those of WPIC and are considered market commentary. They are not intended to act as investment recommendations. Full disclaimers are available at the end of this report.

Platinum group metals in autocatalysts

Automotive demand is the single largest demand segment for platinum, with platinum automotive demand accounting for around 40% of total platinum demand. Palladium and rhodium automotive use is around 80% and 90% of total palladium and total rhodium demand, respectively.

https://www.cmegroup.com/content/dam/cmegroup/education/images/2022/q1/substitution-among-platinum-group-metals-fig05.jpg

Gasoline three-way catalyst. Picture credit: Johnson Matthey

{kind=link}

Platinum and its sister platinum group metals (PGMs), palladium and rhodium, all have the necessary physical and chemical properties that make them well suited to autocatalysis. Their catalytic properties enable the reactions within an autocatalyst to occur, including during the low temperature-conditions that exist during cold starting of a vehicle, when emissions are at their highest. Durability is also important, as catalytic converters need to perform over the life of a vehicle. Without PGMs, the desired conversion reactions in the catalytic converter would not take place, resulting in the vehicle failing to meet emissions regulations. Other materials have been tried, but have not met the long-term activity, durability, and cost-effectiveness requirements of modern-day emissions control systems.

Although platinum has the longest track record as an autocatalyst of any PGM, with a history of use in both diesel and gasoline vehicles dating back to the 1970s, today it is primarily used in diesel vehicles. The question of which PGM is best suited to a particular emissions-control system (and optimal loadings) and the extent to which platinum, palladium and rhodium can be substituted for one another is complex.

PGM usage is determined by multiple factors including the effectiveness, availability, and price of each metal, as well as tightening emissions standards. The catalytic efficiency of each metal (per specific emission) is influenced by engine temperature, fuel type, fuel quality, and durability of the type of PGM-coating or ‘washcoat’ used to fabricate the autocatalyst.

For example, diesel engines operate at lower temperatures than gasoline engines and run with a leaner air/fuel stream containing lots of oxygen. Under these conditions, platinum is a more active catalyst for the conversion of CO and hydrocarbons to harmless emissions.

In the 1990s, the low price of palladium led to it replacing platinum in gasoline autocatalysts, despite twice as much palladium than platinum being required to achieve the same level of emissions control. This 2:1 substitution ratio was necessary at the time because palladium’s catalytic efficiency is compromised by the presence of sulphur; gasoline then had a relatively high sulphur content.

During the early part of this century, the sulphur content of fuel reduced; gasoline fell significantly from over 400 parts sulphur per million to under 100 parts per million. This reduced sulphur content affected patterns of PGM usage in autocatalysts in two ways. Firstly, it was no longer necessary to use double the amount of palladium than platinum in gasoline autocatalysts, meaning that the ‘substitution ratio’ between the two metals moved from 2:1 to 1:1. Secondly, reducing diesel sulphur content meant that the use of some palladium in diesel autocatalysts became feasible.

Historic substitution of platinum for palladium in autocatalysts due to market imbalance

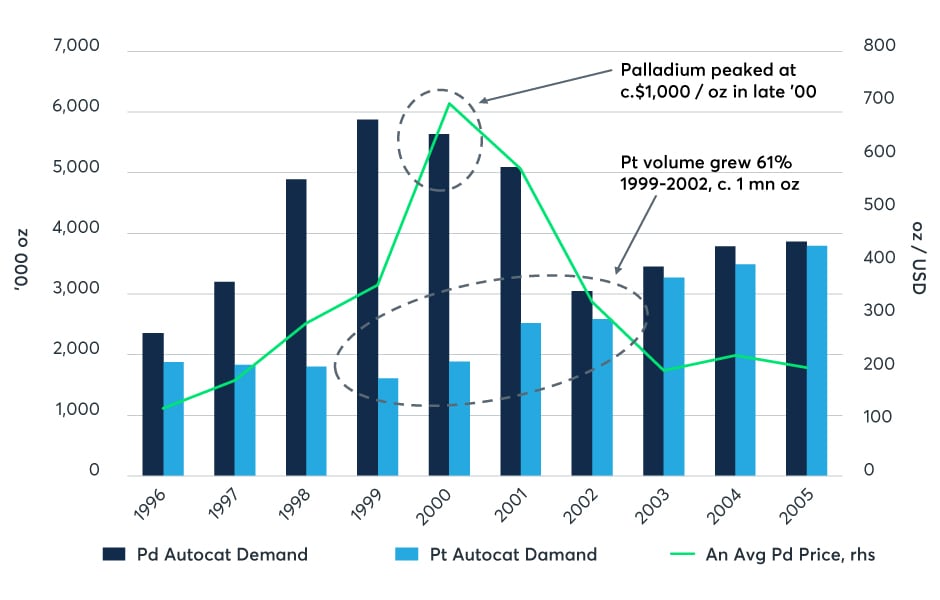

By the late 1990s, palladium demand was consistently outstripping supply. The annual shortfall was supplied from Russian state stocks; palladium was seen as having little value or application during the early years of production as a by-product from the Russian nickel-copper mines, with much of this stock having built up almost accidentally and transferred to state stocks. In 2000, an administrative failure in Russia coincided with a processing failure in South Africa that resulted in the price of palladium increasing from around US$200/oz. to over US$1,000/oz. within a few months.

The consequence of this short-term price spike, to levels well above the price of platinum, was substitution of palladium by platinum with a significant demand increase for less expensive platinum. As illustrated in Figure 1, gross palladium usage in autocatalysts contracted by 48% between 1999 and 2002. Palladium prices reduced in line with reduced demand to US$260/oz. by January 2003. Platinum autocatalyst usage rose by 60% over this same period.

Figure 1: Palladium and platinum auto demand and palladium price, 1996 – 2005

https://www.cmegroup.com/content/dam/cmegroup/education/images/2022/q1/substitution-among-platinum-group-metals-fig01.jpg

Source: Johnson Matthey, Bloomberg, WPIC Research

{kind=link}

Despite the significant substitution of platinum for palladium by 2003, work done to include palladium, particularly in heavy-duty vehicles, continued as by this point the palladium price had returned to below the platinum price, providing a financial incentive for automakers. In addition, the inclusion of some palladium in a platinum-dominant autocatalyst can improve its thermal stability. This is an advantage when reducing diesel particulate matter from the exhaust. This process involves trapping the particulate matter in a filter and then raising the temperature of the system to oxidise the matter to CO2. At these higher temperatures, palladium improves the thermal durability of the catalyst, helping it perform optimally for the lifetime of the vehicle.

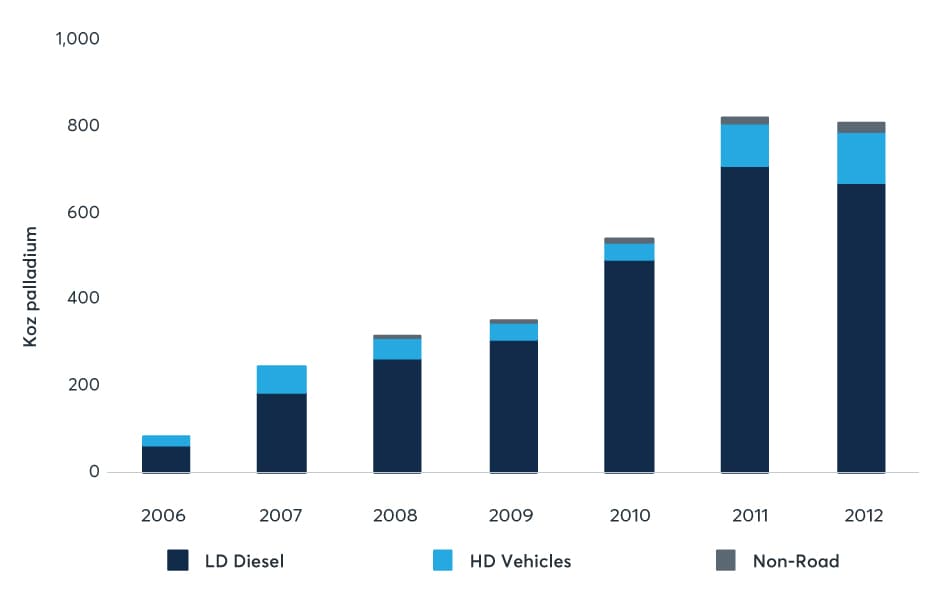

By 2012, data from Johnson Matthey (JM) showed that 800 koz per annum of the then much cheaper palladium had replaced platinum in diesel autocatalysis (Figure 2). This started to reverse from 2014 as palladium had its third consecutive deficit and its cost benefit waned. Although JM ceased publishing the relevant data to demonstrate the trend, it is believed that subsequent palladium deficits drove the substitution of platinum for palladium in diesel autocatalysts, a process that largely completed by 2019, bar some residual palladium in diesel catalysts remaining for thermal stability.

Figure 2: Palladium for platinum substitution in diesel autocatalysts 2006-2012

https://www.cmegroup.com/content/dam/cmegroup/education/images/2022/q1/substitution-among-platinum-group-metals-fig02.jpg

Source: Johnson Matthey, WPIC Research

{kind=link}

Substitution of platinum for palladium in autocatalysts due to market imbalance today

Since 2017, the price of palladium has once again exceeded that of platinum, in 2020 by over $1,500 per ounce. The PGM market today continues to reflect that imbalance, with annual automotive palladium demand exceeding mined supply, resulting in sustained palladium deficits. This has led to a distortion between the price of platinum and palladium, with the latter currently still trading at a significant price premium over platinum.

The sustained demand for palladium in combination with its price premium and supply limitations continues to drive platinum automotive demand growth due to substitution. Indeed, BASF, the global chemicals giant, has demonstrated and tested an autocatalyst with a new washcoat that achieves the partial substitution of high-priced palladium with the relatively lower-priced platinum in light-duty gasoline vehicles already on the road, without compromising emissions standards.

Public discussion by automakers and catalyst fabricators to date has focused on replacing palladium with platinum in the catalysts of vehicle models already available for sale. These substitution efforts started in 2016, driven then by looming palladium shortages and not price differentials. Implementation accelerated once annual cost savings could exceed testing and recertification costs, most likely on larger, high-palladium content models. Fabricators expected platinum demand from substitution defined in this way, to be c.150 koz in 2021 increasing to c.1.5 moz in 2025. The North American market was a natural early substitution target as its regulatory environment requires that emissions are measured across automaker fleets, with emissions control systems replaced gradually over the 5-10 year lower-limit implementation periods.

However, in Europe and China, new lower emissions levels must be met by a specified date. Because Euro 6d and China 6a were implemented by January 2021, all car models intended for sale in Europe and China after that date had their emissions systems redeveloped over the preceding three years in anticipation of the change. This meant that platinum could be used in place of palladium with almost no additional engineering, testing or certification costs and with no public disclosure of these proprietary and confidential developments. The inference is that, by 2021, the gasoline vehicles expected to be produced in China (~20M) and Europe (~8.9M) were already subject to platinum-for-palladium substitution. Taking a conservative view, by assuming that only ~25% of vehicles were considered for a change in metal mix and that the portion of palladium replaced by platinum is only ~30%, additional platinum demand in 2021 from pre-launch metal replacement in Europe and China alone could add ~$440M to OEM profits, importantly increasing annual platinum demand by ~320 koz.

Tightening emissions legislation as a driver of further substitution

Rising PGM loadings is an additional dynamic that is influencing more platinum-for-palladium substitution.

The term ‘loadings’ refers to the quantity of metal used in an emissions control system. Each system on a vehicle comprises one or more autocatalyst ‘bricks’, sometimes in combination with exhaust gas recirculation and liquid urea injection. All parts of the system are intimately integrated with sensors and electronic engine firing controls.

https://www.cmegroup.com/content/dam/cmegroup/education/images/2022/q1/substitution-among-platinum-group-metals-fig06.jpg

Gasoline autocatalyst substrate. Picture credit: Johnson Matthey

{kind=link}

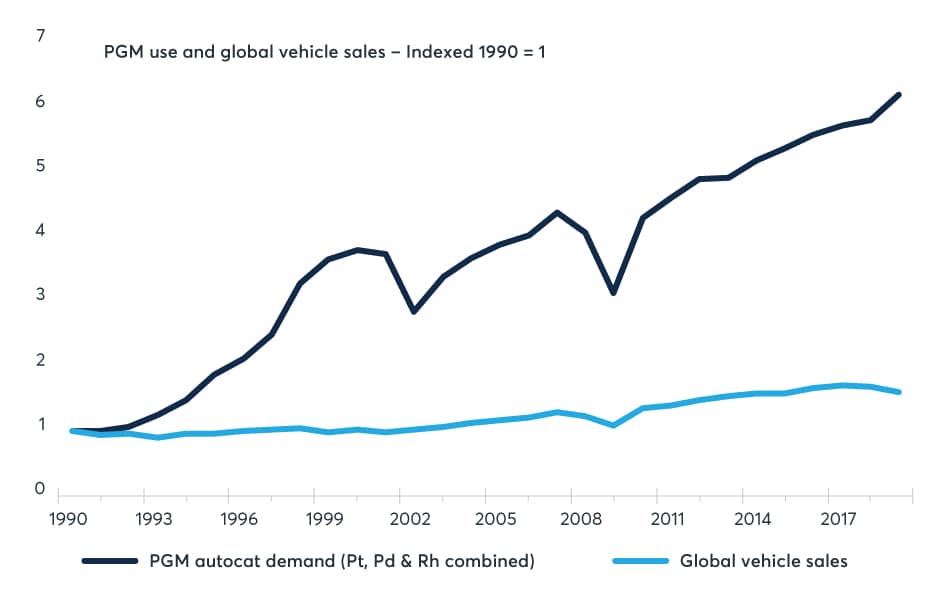

Historically, tightening emissions legislation, more than actual changes in volumes of auto sales, has driven PGM automotive demand growth, as Figure 2 demonstrates. As systems have become increasingly sophisticated in response to more stringent emissions limits and the advent of on-road, rather than in-laboratory, testing, metal loadings have increased.

For example, in Europe, following the 2015 ‘Dieselgate’ scandal, the increased focus on reducing oxides of nitrogen (NOx) from diesel vehicles resulted in higher urea dosing rates and more platinum per catalyst to convert nitrogen oxide to nitrogen dioxide, optimizing the removal of NOx.

In China, the implementation of China VI standards is currently influencing platinum loadings. Applicable to heavy-duty vehicles from July 2021, catalyst fabricators have publicly indicated that compliance with China VI requires PGM loadings on trucks to increase threefold compared to the loadings previously necessary to meet the requirements of predecessor regulations, with platinum accounting for most of this increase.

Figure 3: Total PGM autocatalyst demand growth is well above global auto sales growth over 28 years (6.2 times v 1.6 times)

https://www.cmegroup.com/content/dam/cmegroup/education/images/2022/q1/substitution-among-platinum-group-metals-fig03.jpg

Source: OICA, LMC Automotive, Johnson Matthey. Indexed chart with 1990 = 1

{kind=link}

Since January 2021, all light-duty gasoline vehicles sold in both Europe and China have been required to meet new, lower emissions limits. The combined impact of these limits, known respectively as Euro 6d and China 6 regulations, has led to significantly higher palladium loadings on the gasoline vehicles produced in these regions. These higher loading requirements are exacerbating shortages in the palladium market, which in 2020 experienced its ninth consecutive supply/demand deficit. In addition to the price of palladium significantly overshooting the price of platinum and presenting a material financial incentive to substitute, automakers concern regarding availability of palladium increases the likelihood and magnitude of substitution.

Substitution as a driver of platinum demand growth

The post-pandemic recovery in platinum automotive demand in 2021 was weaker than originally anticipated due to the impact of the ongoing global semiconductor shortage on the automotive industry, with global light vehicle production in 2021 reducing from an expected 87 million vehicles to around 76 million vehicles. Notwithstanding this reduction, automotive demand for platinum in 2021 grew by 14% (+340 koz) to 2,704 koz due to the tighter emission standards and substitution. By way of comparison, pre-COVID demand in 2019 was 2,836 koz against vehicle production of 89 million vehicles.

Turning to 2022, automotive demand for platinum is set to grow 20% (+533 koz) to 3,237 koz, based upon production of 85 million light-duty vehicles, up on 2021 levels, but still short of the projections that prevailed pre-COVID and the ensuing semiconductor shortage. Nevertheless, the 2021 forecast reflects a modest recovery in the automotive sector as the impact of the semiconductor shortage begins to ease and takes demand for platinum in the sector above the pre-pandemic level.

Automotive platinum demand for 2021 included 200 koz of substitution, with a doubling of that forecast in 2022. However, it is possible that the scale of actual platinum-for-palladium substitution has been underestimated, especially given the recent – unexplained – trend for China’s net platinum imports to consistently exceed the country’s identifiable demand.

It is certainly of note that per vehicle platinum loadings under China VI appear to be significantly lighter than those of vehicles in other regions meeting comparable emissions standards. For example, in the heavy-duty vehicle segment, it is estimated that, in 2021, platinum loadings in China were less than 3g per vehicle, in comparison to an estimate of over 20g per vehicle in Europe (albeit that China VI was implemented only in July 2021). This effect is perhaps overlooked because historically, emissions limits in China lagged those in Europe and North America, while China VI and China 6 are, for the first time, slightly more stringent than those in the other two major markets.

An important consideration in forecasting the annual demand impacts of substitution is the fact that, for example, once platinum has replaced palladium in a catalyst, the design of which is a bespoke match per vehicle model platform, the associated annual demand remains in place each year for the c.7-year life of that vehicle platform. If platinum and palladium prices then were to move to parity (reflecting their 1:1 substitution ratio) and thereby removing the financial incentive to replace palladium, the annual platinum demand level would be sustained over the platform life.

IMPORTANT NOTICE AND DISCLAIMER

This publication is general and solely for educational purposes. The publisher, The World Platinum Investment Council, has been formed by the world’s leading platinum producers to develop the market for platinum investment demand. Its mission is to stimulate investor demand for physical platinum through both actionable insights and targeted development, providing investors with the information to support informed decisions regarding platinum and working with financial institutions and market participants to develop products and channels that investors need. No part of this report may be reproduced or distributed in any manner without attribution to the authors. The research for the period 2019 and 2020 attributed to Metals Focus in the publication is © Metals Focus Copyright reserved. All copyright and other intellectual property rights in the data and commentary contained in this report and attributed to Metals Focus, remain the property of Metals Focus, one of our third party content providers, and no person other than Metals Focus shall be entitled to register any intellectual property rights in that information, or data herein. The analysis, data and other information attributed to Metals Focus reflect Metal Focus’ judgment as of the date of the document and are subject to change without notice. No part of the Metals Focus data or commentary shall be used for the specific purpose of accessing capital markets (fundraising) without the written permission of Metals Focus.

Any research for the period 2013 to 2018 attributed to SFA in the publication is © SFA Copyright reserved. All copyright and other intellectual property rights in the data for the period 2013-2018 contained in this report remain the property of SFA, one of our third party content providers, and no person other than SFA shall be entitled to register any intellectual property rights in the information, or data herein. The analysis, data and other information attributed to SFA reflect SFA’s judgment as of the date of the document. No part of the data or other information shall be used for the specific purpose of accessing capital markets (fundraising) without the written permission of SFA.

This publication is not, and should not be construed to be, an offer to sell or a solicitation of an offer to buy any security. With this publication, neither the publisher nor its content providers intend to transmit any order for, arrange for, advise on, act as agent in relation to, or otherwise facilitate any transaction involving securities or commodities regardless of whether such are otherwise referenced in it. This publication is not intended to provide tax, legal, or investment advice and nothing in it should be construed as a recommendation to buy, sell, or hold any investment or security or to engage in any investment strategy or transaction. Neither the publisher nor its content providers is, or purports to be, a broker-dealer, a registered investment advisor, or otherwise registered under the laws of the United States or the United Kingdom, including under the Financial Services and Markets Act 2000 or Senior Managers and Certifications Regime or by the Financial Conduct Authority.

This publication is not, and should not be construed to be, personalized investment advice directed to or appropriate for any particular investor. Any investment should be made only after consulting a professional investment advisor. You are solely responsible for determining whether any investment, investment strategy, security or related transaction is appropriate for you based on your investment objectives, financial circumstances and risk tolerance. You should consult your business, legal, tax or accounting advisors regarding your specific business, legal or tax situation or circumstances.

The information on which this publication is based is believed to be reliable. Nevertheless, neither the publisher nor its content providers can guarantee the accuracy or completeness of the information. This publication contains forward-looking statements, including statements regarding expected continual growth of the industry. The publisher and Metals Focus note that statements contained in the publication that look forward in time, which include everything other than historical information, involve risks and uncertainties that may affect actual results and neither the publisher nor its content providers accepts any liability whatsoever for any loss or damage suffered by any person in reliance on the information in the publication.

The logos, services marks and trademarks of the World Platinum Investment Council are owned exclusively by it. All other trademarks used in this publication are the property of their respective trademark holders. The publisher is not affiliated, connected, or associated with, and is not sponsored, approved, or originated by, the trademark holders unless otherwise stated. No claim is made by the publisher to any rights in any third-party trademarks.