{kind=link}

Spread Trading Sector Index Futures

It has been very well known that, over the course of time, volatility in the equity market goes through ebbs and flows. Much less attention has been paid to the fact that an offshoot of this phenomenon is equally significant and fascinating. When volatility crests, performance of all stocks tend to be highly correlated. When volatility subsides, the stocks in different sectors start to wander in different directions.

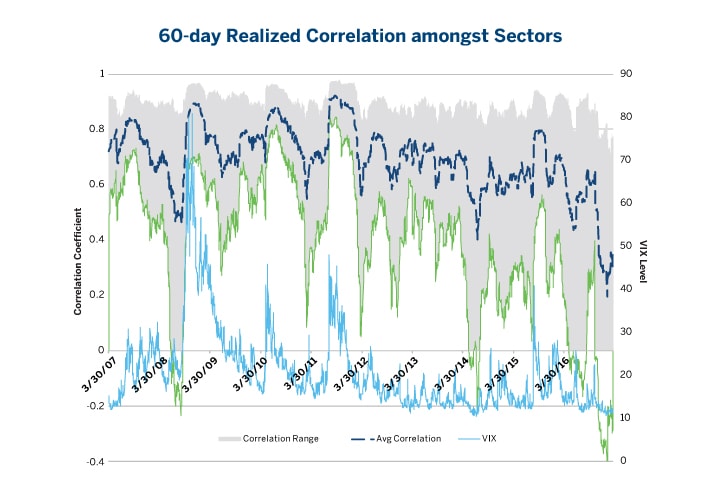

Figure 1 shows a 10-year history of the US equity market volatility, with the venerable VIX index being the proxy. During this decade, there were many episodes of volatility spikes, e.g. the financial crisis, European sovereign debt crisis, etc. There were also many long stretches of time in which the equity market was trending up slowly – melting up, as some observers commented – with implied volatility hovering at around 10% - 12% per annum.

Volatility spikes appear to correspond to periods of high correlation amongst the returns of different sectors. When the spikes subside, sectors tend to decouple, especially after a prolonged period of low volatility. The blue dotted line corresponds to average correlation for all pairs of sectors based on the S&P Select Sector Indexes (9 sectors, 10 if the real estate sector is included). The shaded area shows the range of correlation amongst different sectors.

Figure 1. 60-day Realized Correlation amongst Sectors

{kind=link}

If the correlation coefficient between GICS level sectors was calculated for the same 10-year period, the lulls in volatility coincide with periods in which these correlations drop. Note that the dispersion of correlation has been particularly pronounced in the last 2 years, with few macroeconomic or geopolitical events interrupting the low volatility regime. Under this environment, there could be a lot of room for spread trading in different sectors. CME Group’s suite of E-mini S&P Select Sector Index Futures is a very convenient and effective tool for this purpose.

E-mini S&P Select Sector Index Futures

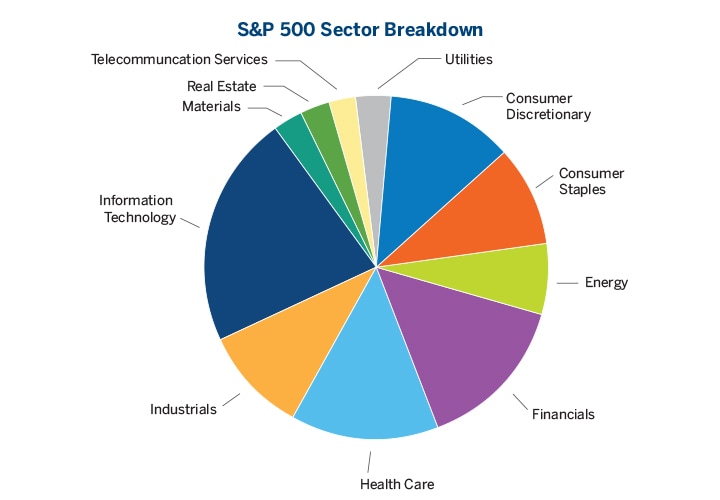

Global Industry Classification Standard classifies company into 11 different top level sectors. Figure 2 shows the GICS level 1 sector breakdown. The Information Technology and Telecommunication Services are combined into the Technology sector under the S&P Select Sector Indexes for purpose of maintaining broad-based nature of the index.

CME Group has been listing E-mini S&P Select Sector Index Futures suite1 for trading since 2011. Table 1 shows the size of the contract as well as bid/ask spread for an approximately $1-$2 million trade.

As of March 17, 2017. Note that the S&P Select Sector indexes combined the Information Technology and Telecommunication Services into a single S&P Technology Select Sector Index.

Figure 2. S&P 500 Sector Breakdown

{kind=link}

Table 1. E-mini S&P Select Sector Index Futures Market

Data taken from 3/10 – 3/16, 2017. Approximate contract value, ticker symbol, approximate notional value of a 25-contract trade and the associated bid/ask spread in basis point is shown.

| Sector | Ticker | Contract Value ($) | 25-contract Notional Value ($ ‘000) | 25-contract Bid/Ask Spread (bps) |

| Consumer Discretionary | XAY | 87,774 | 2,194 | 4.44 |

| Consumer Staples | XAP | 55,260 | 1,382 | 5.37 |

| Energy | XAE | 69,832 | 1,746 | 5.92 |

| Financial | XAF | 76,115 | 1,903 | 7.11 |

| Healthcare | XAV | 76,066 | 1,902 | 4.99 |

| Industrial | XAI | 65,540 | 1,639 | 4.88 |

| Materials | XAB | 55,238 | 1,381 | 6.48 |

| Real Estate | XAR | 37,233 | 931 | 11.49 |

| Technology | XAK | 53,300 | 1,333 | 6.16 |

| Utilities | XAU | 51,510 | 1,288 | 7.27 |

Similar to the E-mini S&P 500 index futures listed at CME, trading in E-mini Select Sector index futures benefit from the capital efficiency, electronic market access, tax treatment and other features of futures markets. In particular, margin offsets between the long and short leg of the trade provide additional capital efficiency for the strategy. Furthermore, there is no need to locate for borrow the security that is the subject of the short leg – a further convenience when implementing the spread trading strategy using index futures.

Constructing Sector Spread Trade

There is no “correct” way of constructing a spread trade between sectors. The most common strategy is a simple notional value matching exercise. By way of example, if a market participant has a view that the Energy sector will underperform the market while the Financial sector will outperform the market, one can conceivably buy $10 million of the Financial sector exposure while short selling $10 million of the Energy sector exposure. Using the value from the table 1, this trade can be consummated by buying 131 XAF contracts and selling 143 XAE contracts.

This simple strategy makes the most sense in the context as an overlay of a broad-based portfolio. For example, if the current investment is indexed to the S&P 500 index futures, by buying and selling equal notional value of sector exposure is tantamount to shifting the sector exposure in the overall portfolio, underweighting one sector while overweighting another. The total dollar amount of the investment remains unchanged – thus, no additional leverage is deployed.

One unintended consequence of using the equal notional value approach is the distinct possibility that the spread strategy itself is not market-neutral. If the premise of the trade is that one sector is expected to outperform the market while the other underperforms the market, the spread trade itself might intuitively have been expected to remain invariant to market condition. In other words, the trade should not yield significant P/L solely due to the market drifting in one direction or the other. To borrow an analogy from the fixed income market, a trade that is supposed to benefit from the yield curve steepening (i.e. short duration bonds outperforming long duration ones) should not be marred by the yield curve shifting up or down. The loose equivalence of matching DV012 in the yield curve steepening trade is to adjust the size of the long and short position based on their relative sensitivity to market movement, viz. a larger position in the leg with lower sensitivity to overall market directional move.

Side-stepping the question of how the relevant coefficients are estimated, one can contemplate the following equation:

The coefficient β indicates the sensitivity of the sector return to market return, while ε denotes the sector specific return. Typically, β is estimated by regressing the historical returns of the sector on those of the overall market, perhaps indexed by the S&P 500. If 1 dollar of exposure is purchase in Sector A and µ dollar of exposure is sold in Sector B, the total sensitivity to the market returns would be (βA–μβB). To eliminate exposure to the market returns, µ can be set to:

Thus, if sector B is less sensitive than sector A to the market return, µ will be greater than 1. This means the position in sector B needs to be adjusted upward, beyond parity in notional value.

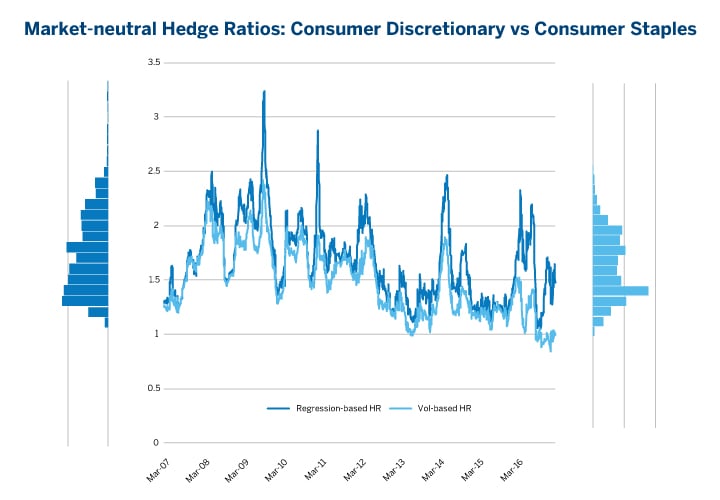

While this approach is intellectually appealing, its result could be more volatile than one would hope to achieve. Figure 3 illustrates this feature.

The spread between the consumer discretionary and consumer staples sector was popular in 2016. As such, this spread is used for our illustrative purpose. To amplify the issue, suppose the two sectors “betas” were estimated with very limited sample3. The blue line shows the rolling estimate of the hedge ratio. While all estimates are subject to estimation errors – to say nothing about the ensuing forecasting error by simply adopting the historical estimate, the estimates are prone to large sudden shifts and spikes. Indeed, the histogram associated with the estimates on the left panel in the figure shows a very wide distribution of the estimates with a discernable tail.

If the theoretical hedge ratio is broken down further, one can further deduce that it is equivalent to the following:

The blue line in the middle panel shows the hedge ratio based on the ratio of betas vs S&P 500 using 60-day samples. The left panel shows the histogram of such hedge ratio estimates. The red line in the middle panel shows the hedge ratio based on historical volatility of the two Select Sector Indexes. The right panel shows the histogram of the estimates where the ρ's are the sector indexes' correlation with the market, and the σ's are the sector indexes' .

Figure 3. Market-neutral Hedge Ratios: Consumer Discretionary vs Consumer Staples

{kind=link}

Thus, the hedge ratio is the product of the ratio of correlation and the ratio of volatilities.

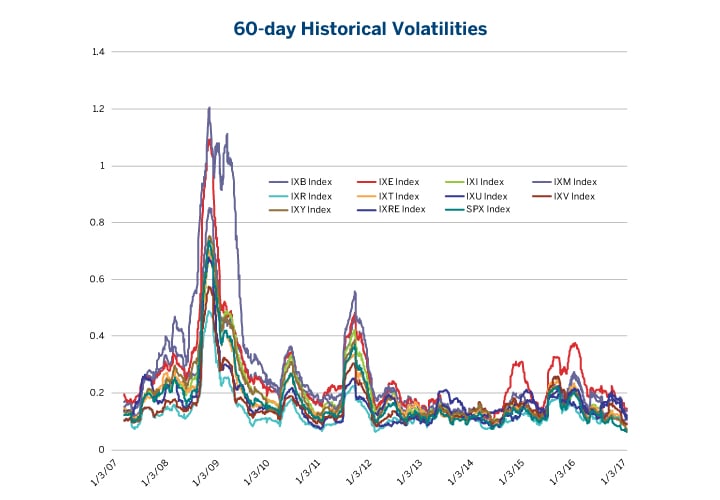

As shown in Figure 1, the correlation coefficients during the last decade has been quite volatile. Indeed, during the period when volatility is low, the breakdown in correlation tend to occur. The ratio of the volatilities could be a much more stable quantity. Figure 4 shows the co-movement of 60-day historical volatilities amongst the Select Sector indexes as well as the S&P 500 index.

As such, an alternative hedge ratio could just the ratio of volatilities, or:

The red line in figure 3 shows the hedge ratio derived in this manner, using the same rolling short samples. It is quite evident that the estimates are less volatile than the original regression-based hedge ratios. The histogram on the right panel illustrated as much.

Historical Volatilities for S&P 500 and the S&P Select Sector Indexes. It is apparent that the sector volatilities tend to follow the overall market volatility to varying extent. That the Financial Sector volatility was highest during the financial crisis (2008-2009) is not surprising. That market stress extended to other sectors is also expected.

Figure 4. 60-day Historical Volatilities

{kind=link}

There is also a natural interpretation to using this ratio: the spread thus constructed attempts to recalibrate the moves in terms of “standard deviations” in their respective sectors, and put the same dollar amount on both sides couched in such terms.

A further advantage of using the approach of volatilities-based hedge ratio is the fact that it is possible to use forward looking volatilities to construct the hedge ratios. Options on related instruments exist to provide a market-based volatility estimates for the hedge ratio.

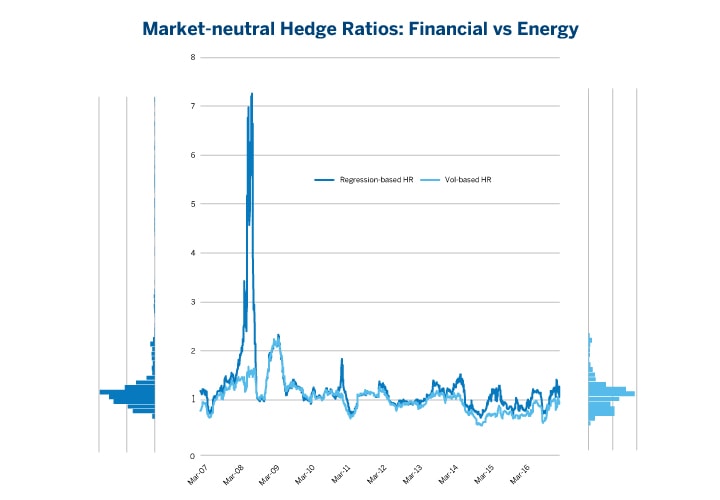

As a final illustration, the same graphic as in figure 3 is provided in figure 5 but is constructed for a “financial vs energy” sector spreads. While there is no natural, thematic interpretation for the spread, these two sectors had been particularly volatile during the past decade. The volatility-based hedge ratios curtailed much of the wild swings in the estimates.

The blue line in the middle panel shows the hedge ratio based relative historical volatilities. The left panel shows the histogram of such hedge ratio estimates. The red line in the middle panel shows the hedge ratio based on historical volatility of the two Select Sector Indexes. The right panel shows the histogram of the estimates.

Figure 5. Market-neutral Hedge Ratios: Financial vs Energy

{kind=link}

1 More details about the contracts and their specifications can be found at http://www.cmegroup.com/sectors.

2 By equating the dollar value per 1 basis point (DV01) on both long and short leg, a parallel shift of the yield curve will produce an offsetting P/L in the spread trade.

3 The problem of whether a historical regression based for purpose of estimating the “beta” is sidestepped in this discussion. Rather, the focus is on the question of stability. The short sample of rolling 60-day daily return data is deliberately chosen to exacerbate the issue.