{kind=link}

Platinum Industrial Demand

Industrial demand is a key segment for platinum

Understanding the dynamics of platinum demand is essential to understanding the investment case for platinum, which is based on an evaluation of trends in platinum demand, supply, and market balances. Currently, platinum demand growth drivers, against a backdrop of constrained supply, increase the consequent likelihood of future deficits.

Platinum demand is complex. Firstly, as a commodity, platinum is not always well understood. Is it a precious metal or is it an industrial metal? These distinctions can sometimes cause confusion. The truth is that platinum is both a precious metal and an industrial metal. From an investment perspective, platinum is closely correlated to gold and brings similar diversification benefits to a portfolio, as well as being a hedge against currency and interest rate fluctuations and a store of value. However, platinum’s price also reflects its supply/demand fundamentals which are closely linked to demand growth and its industrial value-in-use.

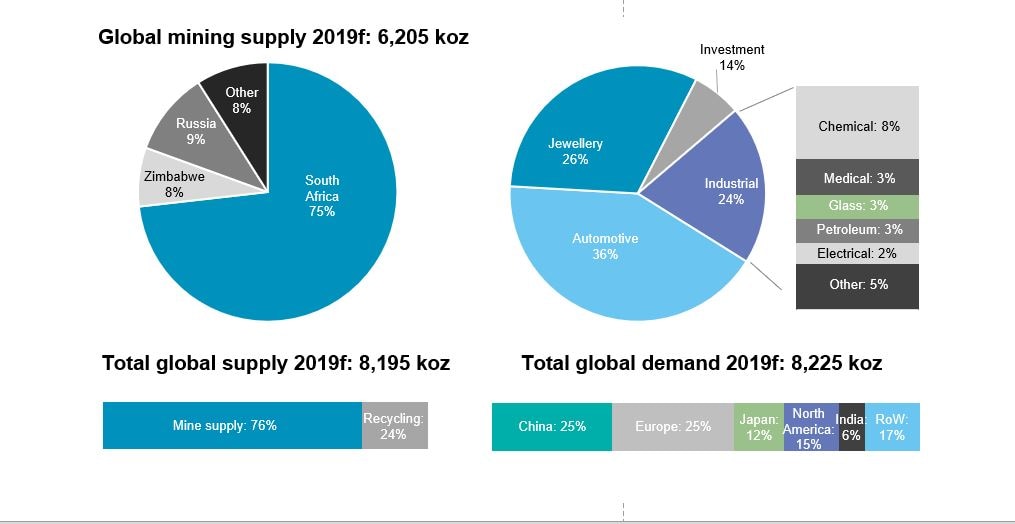

Platinum demand is broadly split between four segments with their relative portion of annual demand related to application and value (five-year annual % ranges shown for the period 2015-2019):

- Automotive applications (36-42%) - autocatalysts controlling emissions from internal combustion engine vehicles, currently mainly in diesel vehicles

- Jewellery (26%-35%) - the premier jewellery metal in Asia and the West

- Industrial (21-26%) - myriad uses

- Investment (0%-15%) - changes in holdings of physically backed ETFs and futures exchange physical stocks as well as purchases of bars and coins

Automotive demand can be viewed as an ‘industrial’ use of platinum, but it is considered as a separate category due to its size and the strategic nature of vehicle emissions control. Vehicle sales are not possible without regulatory compliance which is also integral to avoiding negative reputational risk for automakers. This article focuses on non-automotive industrial demand for platinum; platinum’s other demand drivers will be considered in future articles.

Figure 1: Sources of platinum demand

{kind=link}

Source: WPIC Platinum Quarterly, five-year annual % ranges 2015-2019

What is industrial demand?

Industrial use of platinum is diverse in terms of both end uses and geography, coming from six main sectors, as figure 2 sets out.

Figure 2: Sources of industrial demand for platinum

{kind=link}

Source: WPIC, SFA (Oxford)

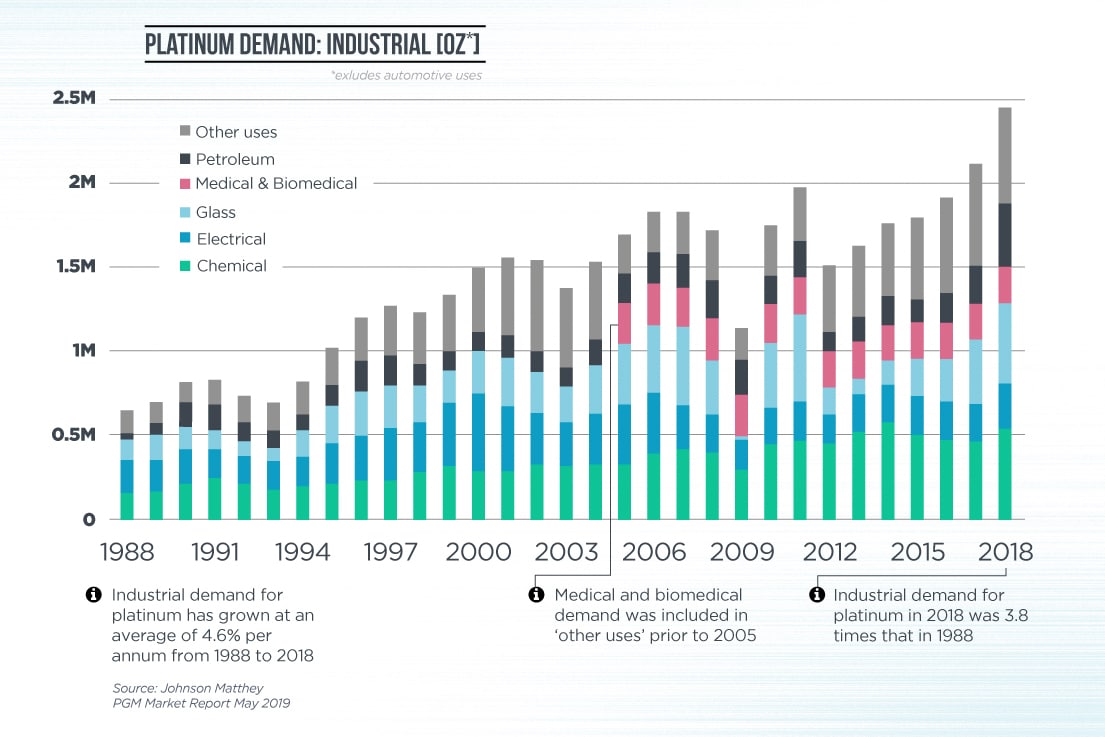

Annual growth in platinum demand from industrial uses has averaged over 3% for the past 20 years, and over 7% for the past five years. This growth has resulted in the amount of industrial platinum demand in 2018 being nearly four times the level in 1988. Industrial demand growth is driven by global economic growth – it is closely correlated to GDP growth – and advances in technology.But demand can exhibit short-term ‘lumpiness’ which is unrelated to macro trends, but rather linked to the nature of the technical application that drives the demand. This includes platinum catalysts and tooling for glass manufacturing, both major sources of industrial demand.

Where platinum catalysts are concerned, there are two types of demand that need to be taken into consideration. The first type of demand comes from the relatively small volumes attributable to the ongoing ‘wear’ of platinum catalysts already in service. In contrast, the second source of demand can be significant, coming as it does from the deployment of entirely new catalysts as new plant capacity is constructed.

Further, platinum from recycled industrial catalysts that have been subject to ‘wear’ is typically recycled and used to produce these entirely new catalysts. This process is known as closed-loop recycling. Typically, the industrial user owns or leases the metal necessary while the old catalyst, plus the ‘top up’ metal to account for wear, is used to produce a replacement catalyst.

Unlike other sources of demand, consumption of platinum in industrial applications is usually expressed on a net basis, that is the gross demand less the supply of ‘closed-loop’ recycled metal. This net industrial demand is in contrast to automotive demand, for example, which is gross demand with metal recycled from used catalysts treated as recycle supply, and is from open loop recycling.

Figure 3: Industrial platinum demand, 1988 to 2018

{kind=link}

Graphic Credit: WPIC, Visual Capitalist

How is platinum used in industry?

Introduction

Platinum has a unique combination of physical and chemical properties, which is why it is used so extensively in industry and manufacturing, where its high melting point, density, ultra-stability, extreme non-corrosiveness and catalytic effects are highly valued.

Indeed, one of platinum’s most important uses is as a catalyst – the presence of even a small molecule can speed up chemical reactions, reducing process energy needs and improving yields.

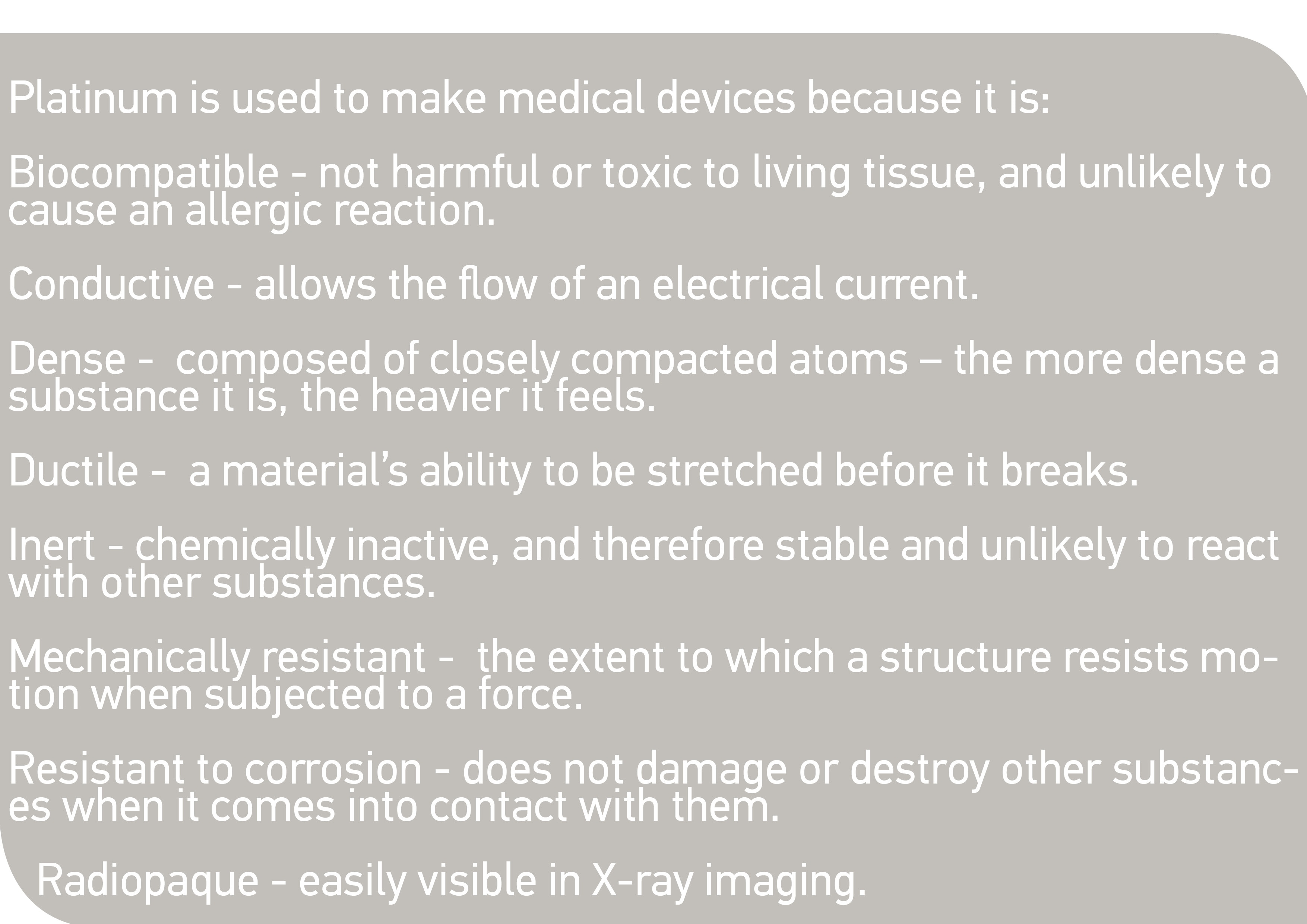

Biocompatible and well-tolerated by the body, platinum is used in numerous established medical treatments and is at the forefront of many new ones. It is radiopaque due to its density, giving high x-ray visibility, especially important in stents and clot-retrieval devices used to treat cardiovascular disease. In addition, platinum is an excellent electrical conductor when used in pacemakers and cochlear implants. Compounds made from platinum are used in the treatment of many cancers.

Figure 4: Summary of the properties that make platinum highly suited for medical use

{kind=link}

Physical strength and stability, maintained at very high temperatures and in chemically hostile environments, support platinum’s use in glass manufacturing (including: flat screen TV glass; mobile phone glass; glass fibre for fabrication and thermal insulation; and high-quality data transmission).

Platinum in manufacturing

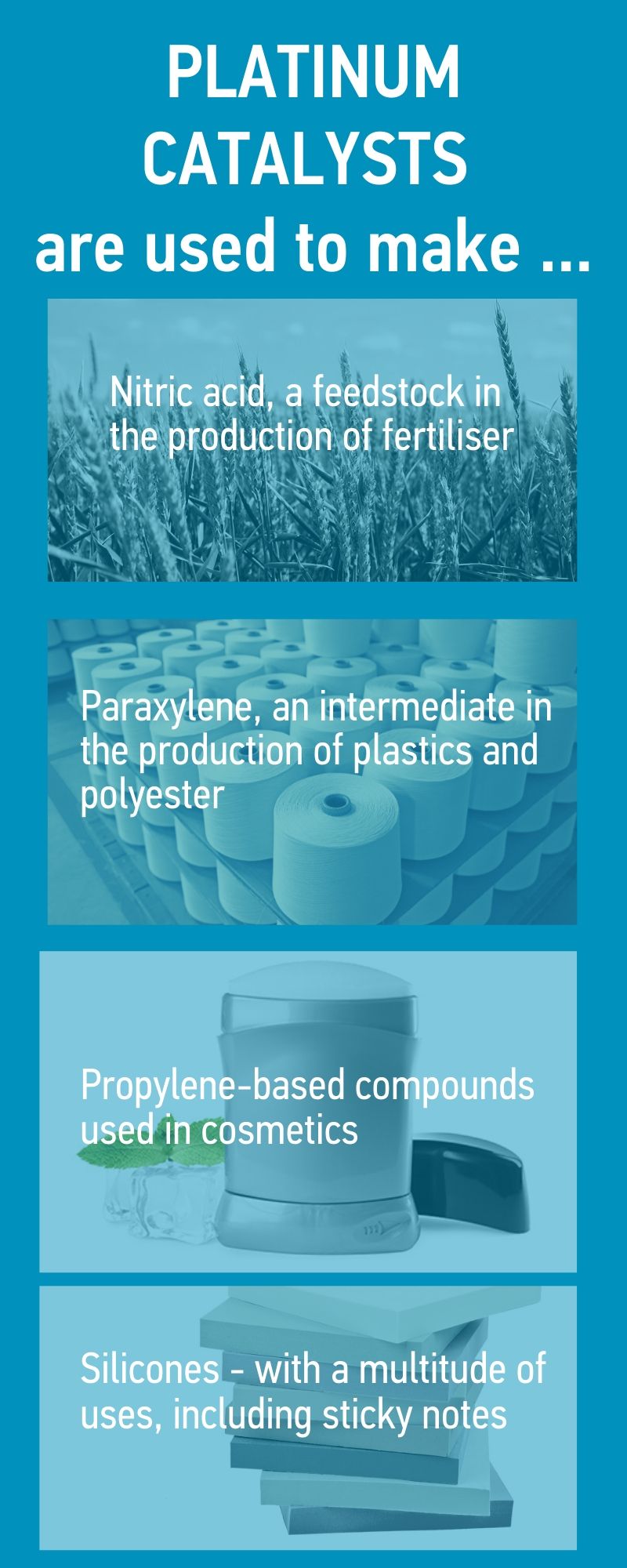

Due to its catalytic properties, platinum has been used in the commercial production of nitric acid - a key component of fertiliser - since the early 20th century. Around 90 % of nitrogen manufactured using platinum goes towards producing the c.190m tonnes of fertiliser nutrients used each year.

Elsewhere in the chemicals sector, platinum catalysts are used in propane dehydrogenation (PDH) facilities and to make paraxylene, an intermediate that is used in the production of plastics and polyester textiles. PDH is used in the production of propylene from propane.

The petroleum industry uses platinum in the refinery process – the process by which crude oil is transformed into more useful petrochemicals needed for a wide range of industrial applications. Petroleum refinery happens in several stages, and platinum catalysts are involved once the initial separation of the crude oil has occurred, helping to manufacture higher-octane fuels such as gasoline.

Platinum is also frequently used as a catalyst in the curing process in the manufacture of specialty silicones, where performance characteristics such as high purity, tear-resistance, transparency and low toxicity are important.

Figure 5: Uses of platinum catalysts

{kind=link}

Platinum components

As well as in medical devices and glass products, platinum components are used in the manufacture of a vast number of other products.

Stable and corrosion resistant, with excellent conductivity, platinum is well-suited as a sensor component, for example, often in ‘mission-critical’ situations that call for reliability and efficiency. Airbags, breathalysers, resistance thermometers and carbon monoxide detectors all contain platinum.

In the tech industry, cloud-based data storage and management services are run from data centres that pool together a large number of servers to provide the capacity and applications needed to meet user demand. A server – like most computers – uses hard disk drives (HDDs) to store data.

Platinum plays a vital role in the magnetic media alloy used in modern HDDs. Its inclusion in their ultra-thin magnetic storage layer improves thermal and magnetic stability, enabling higher density storage. Modern HDDs could not exist without platinum, and it will continue in the same crucial role in upcoming, next-generation technologies.

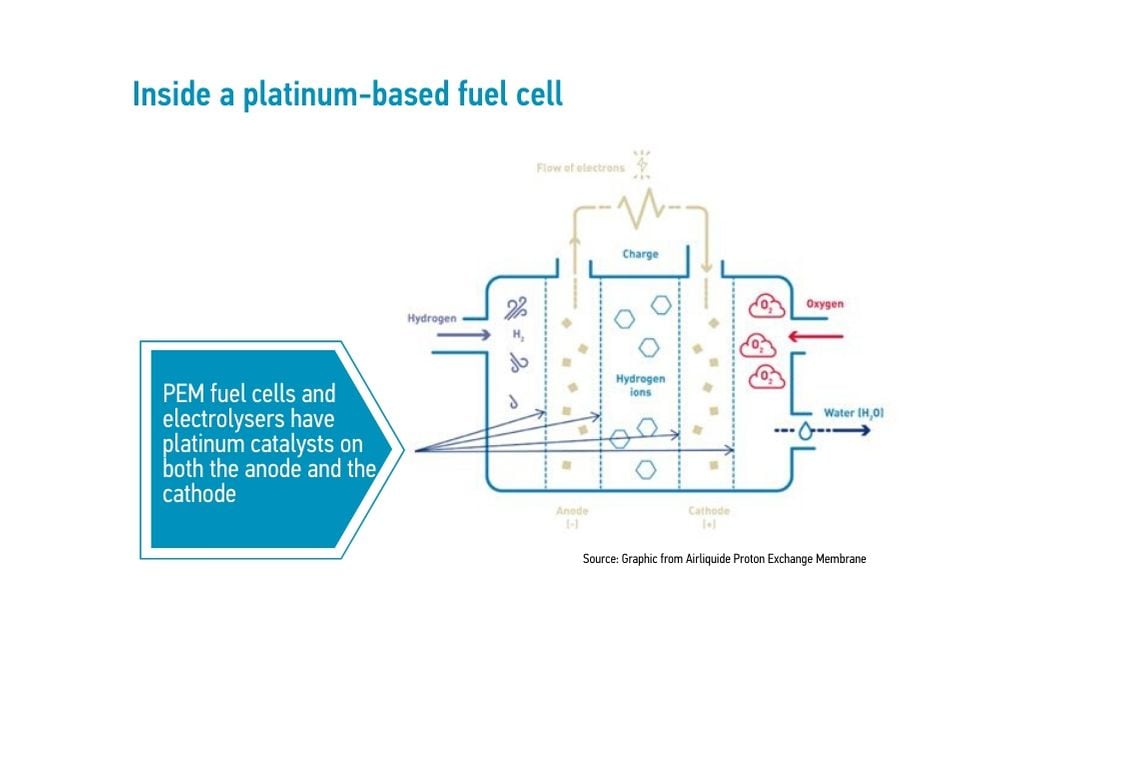

Fuel cells

The use of electricity from hydrogen fuel cells is gaining recognition as an alternative to electricity from fossil fuels or batteries in electric vehicles. A fuel cell is a device that generates electricity through an electrochemical reaction, not combustion.

In a platinum-based hydrogen fuel cell, hydrogen and oxygen are combined to generate electricity, with heat and water as the only by-products. Molecules of hydrogen and oxygen react and combine using a proton exchange membrane which is coated with a platinum catalyst.

Platinum is especially suited as a mobile / transport fuel cell catalyst as it enables the hydrogen and oxygen reactions to take place at an optimal rate, while being stable enough to withstand the complex chemical environment within a fuel cell and high electrical current density, performing efficiently over the long-term.

Fuel cells share many of the characteristics of a battery – silent operation, no moving parts and an electrochemical reaction to generate power. However, unlike a battery, fuel cells need no recharging and will run indefinitely when supplied with fuel. A fuel cell can have a battery as a system component to store the electricity it is generating.

Platinum-based hydrogen fuel cells are particularly important in providing clean electric mobility and are already being used to move goods across the supply chain – from hydrogen powered trucks to fork-lift trucks moving goods around a warehouse. Passenger transportation is also using fuel cells, with hydrogen-fuelled ferries, trains, trams and buses appearing with increasing frequency in a number of cities around the globe. FCEVs combine the emissions-free driving of battery electric vehicles with the quick refuelling times and range of a traditional gasoline or diesel vehicles.

Many of the world’s leading automotive companies are developing, or have developed, hydrogen platinum-based fuel cell electric vehicles (FCEVs) as a preferred technology in response to the challenge of improving air quality and reducing tail-pipe emissions to zero.

Figure 6: Inside a platinum-based fuel cell

{kind=link}

Future prospects for industrial demand growth

Industrial demand for platinum is not reliant on any one sector or territory and is likely to continue growing at or above the rate of global growth. Current forecasts indicate that in 2020 industrial demand will grow by 2 per cent.

Other factors, including population growth and demographics, also have the potential to positively impact platinum demand over the long term. For example, the United Nations Food and Agricultural Organisation projects that food and feed production will need to increase by 70% by 2050 to meet the world’s food needs. Maintaining food production for the growing world population requires the ability to grow more food on current cropland, and fertiliser production – which needs nitric acid – is key to achieving this.

Platinum’s medical applications are similarly affected. The number of people aged 65 or older is forecast to double to 20%of the global population (which is itself growing) by 2050. In addition, access to healthcare in both developed and developing countries is on the rise.

Industrial demand growth is also poised to come from new technologies and fuel cells in particular, as there is increasing acceptance that FCEVs will sit alongside battery electric vehicles as part of a multi-drivetrain solution to achieve zero on-road emissions. Platinum’s demand growth from fuel cells will come initially from heavy duty applications.

IMPORTANT NOTICE AND DISCLAIMER: This publication is general and solely for educational purposes. The publisher, The World Platinum Investment Council, has been formed by the world’s leading platinum producers to develop the market for platinum investment demand. Its mission is to stimulate investor demand for physical platinum through both actionable insights and targeted development: providing investors with the information to support informed decisions regarding platinum; working with financial institutions and market participants to develop products and channels that investors need. No part of this publication may be reproduced or distributed in any manner without attribution to the authors. Unless otherwise specified in this document all material is © World Platinum Investment Council 2017. Material sourced from third parties may be copyright material of such third parties and their rights are reserved. Content within the publication that has been provided by SFA, one of our third party providers, is © SFA Copyright reserved. All copyright and other intellectual property rights in such content contained in this publication remain the property of SFA, and no person other than SFA shall be entitled to register any intellectual property rights in the information, or data herein. The analysis, data and other information attributed to SFA reflect SFA’s judgment as of the date of the document and are subject to change without notice. No part of the content provided by SFA shall be used for the specific purpose of accessing capital markets (fundraising) without the written permission of SFA.

This publication is not, and should not be construed to be, an offer to sell or a solicitation of an offer to buy any security. With this publication, neither the publisher nor SFA intend to transmit any order for, arrange for, advise on, act as agent in relation to, or otherwise facilitate any transaction involving securities or commodities regardless of whether such are otherwise referenced in it. This publication is not intended to provide tax, legal, or investment advice and nothing in it should be construed as a recommendation to buy, sell, or hold any investment or security or to engage in any investment strategy or transaction. Neither the publisher nor SFA is, or purports to be, a broker-dealer, a registered investment advisor, or otherwise registered under the laws of the United States or the United Kingdom, including under the Financial Services and Markets Act 2000 or Senior Managers and Certifications Regime or by the Financial Conduct Authority.

This publication is not, and should not be construed to be, personalized investment advice directed to or appropriate for any particular investor. Any investment should be made only after consulting a professional investment advisor. You are solely responsible for determining whether any investment, investment strategy, security or related transaction is appropriate for you based on your investment objectives, financial circumstances and risk tolerance. You should consult your business, legal, tax or accounting advisors regarding your specific business, legal or tax situation or circumstances.

The information on which this publication is based is believed to be reliable. Nevertheless, neither the publisher nor any third party can guarantee the accuracy or completeness of the information. This publication contains forward-looking statements, including statements regarding expected continual growth of the industry. The publisher notes that statements contained in the publication that look forward in time, which include everything other than historical information, involve risks and uncertainties that may affect actual results and neither the publisher nor any third party accepts any liability whatsoever for any loss or damage suffered by any person in reliance on the information in the publication.

The logos, services marks and trademarks of the World Platinum Investment Council are owned exclusively by it. All other trademarks used in this publication are the property of their respective trademark holders. The publisher is not affiliated, connected, or associated with, and is not sponsored, approved, or originated by, the trademark holders unless otherwise stated. No claim is made by the publisher to any rights in any third-party trademarks.