{kind=link}

Introduction to the CME Group Volatility Index (CVOL)

An Introduction to the CME Group Volatility Index (CVOL)

Introduction

Options have proven useful instruments in gauging the market’s future expected risk for a given product. However, conventional metrics that use options prices to estimate uncertainty in the days to come do not always capture all available information.

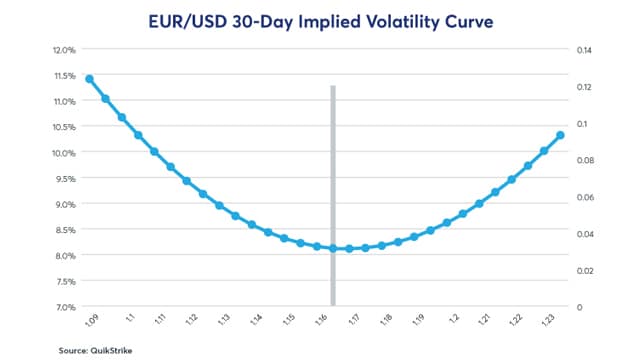

For example, at-the-money (ATM) implied volatility is a widely used barometer to estimate the current level of risk being priced by the options on a given product. ATM implied volatility value is calculated by using option pricing models, such as Black-Scholes, on options with strike prices that are very close to where the underlying is trading at that time. But what about the pricing information available from the options at all the other strike prices for that product (see chart illustration below)—how can those options also be factored into an estimate of future uncertainty?

{kind=link}

CME Group’s new family of implied volatility indexes, the CME Group Volatility Index (CVOLTM), offers an indicator of implied volatility that employs a more complete set of option prices to determine a robust estimate of future uncertainty on any underlying product. These indexes have a variety of advantages including, but not limited to:

- Reflecting the volatility of the entirety of the implied volatility curve

- Allowing for easy comparison of volatilities across different markets

- Allowing for the creation of broad-based indices that can capture the volatility of multiple products/markets in a single number

- Creating an entire family of volatility calculations that allows users to drill into specific parts of the volatility curve, such as viewing implied volatility that specifically applies to call options

- Providing a figure that captures volatility at a constant 30-day forward-looking period

- Available in both a live streaming version (from live option prices) as well as a daily, end-of-day version (from option settlement prices)

How are the CVOL Indexes calculated?

Construction

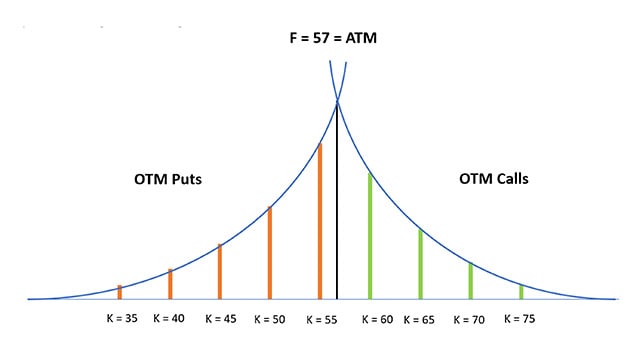

The construction of these indexes involves calculating the Variance Estimate by combining the information of the entire volatility curve. This Variance Estimate is determined by taking the out-of-the-money (OTM) call options and OTM put options for a given expiration. These options can be visualized below, with the boundary between the two sets of options being the price of the underlying, or the ATM:

{kind=link}

Here the option premiums are represented by the height of the bars (i.e., the y-axis) and organized by strike (i.e., the x-axis).

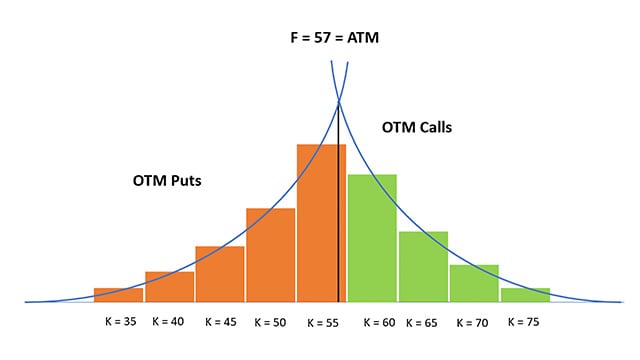

The Variance Estimate is then calculated by approximating the area underneath the combined curves (represented in blue). This is done by taking the option premiums for each strike and multiplying each premium by the average distance of the adjacent strikes. This can be visualized below:

{kind=link}

Here we create the 'base' of each option premium to create an area that is representative of the area underneath the curve.

Summing the areas above allows us to arrive at the Variance Estimate. Taking the Variance Estimate and time weighting it with the Variance Estimate of other expirations then gives us a constant 30-day Variance Estimate. This is then converted into a volatility, which the CVOL Indexes represent. Both the live streaming indexes and end-of-day benchmark versions of CVOL utilize this same methodology.

Derivative indicators

The main CVOL Indexes are also published with a family of derivative indicators. These indicators provide additional insight into the market’s pricing of the implied volatility curve. These derivative metrics include:

- Upward Variance (UpVar)

- Downward Variance (DnVar)

- Skew, the relationship between UpVar and DnVar, expressed as the difference, UpVar – DnVar

- At-the-Money Implied Volatility (ATM)

- Convexity, expressed as the ratio between At-the-Money Implied Volatility and main CVOL Index

The first two indicators of UpVar and DnVar are Variance Estimates for specific segments of the implied volatility curve. UpVar is the Variance Estimate from out-of-the-money (OTM) call options while DnVar is the Variance Estimate from out-of-the-money put options. These metrics provide insight into possible asymmetry in the implied volatility curve by examining the two sides of the curve separately. Skew is the relationship between UpVar and DnVar, calculated as the difference between the two (UpVar – DnVar), and so expresses this asymmetry in a single value.

Broad-based asset-class indexes

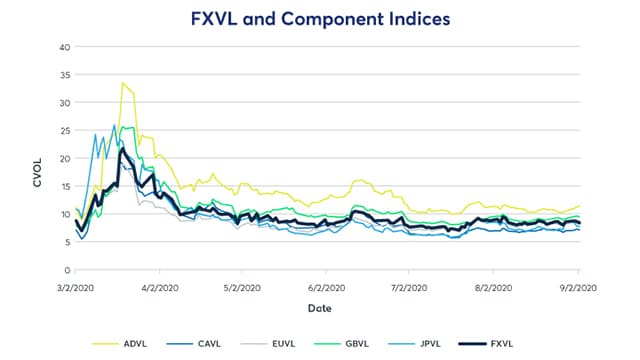

While the main CVOL Indexes provide insight into implied volatility in individual markets, the broad-based indexes provide insight into the implied volatility of associated products when combined. These indexes are constructed to include both the Variance Estimate of each component, as well as the relative quantity of risk held in the options of each component product in the index.

The weights of individual components in the broad-based index are determined by their total Dollar Vega open interest. This metric estimates the aggregate dollar value sensitivity of option premiums in the market given a change in implied volatility for a given product. In other words, total Dollar Vega open interest provides an estimate of the volatility risk profile of all options outstanding for a given product in dollar terms.

The graph below shows how this weighting method combines the G5 currencies into the FX Volatility Index (FXVL) over a six-month period:

{kind=link}