{kind=link}

Introduction to Crack Spreads

The energy markets at CME Group serve as a means of price discovery for the international marketplace. The crude oil, gasoline and diesel (ULSD) derivatives contracts offered at CME Group under the rules and regulations of NYMEX, a CME Group exchange, are reliable risk management tools that serve as global benchmarks. All contracts provide the safety and security of central clearing through CME Clearing, whether they are exchange-traded futures contracts or contracts traded over-the-counter and submitted for clearing through CME ClearPort.

This handbook is designed to facilitate trading of the crack spread, which is the spread between crude oil prices and products derived from crude oil processing — gasoline and diesel. It offers detailed explanations of the types of crack spreads and provides numerous examples of how they can be traded.

What is a Crack Spread?

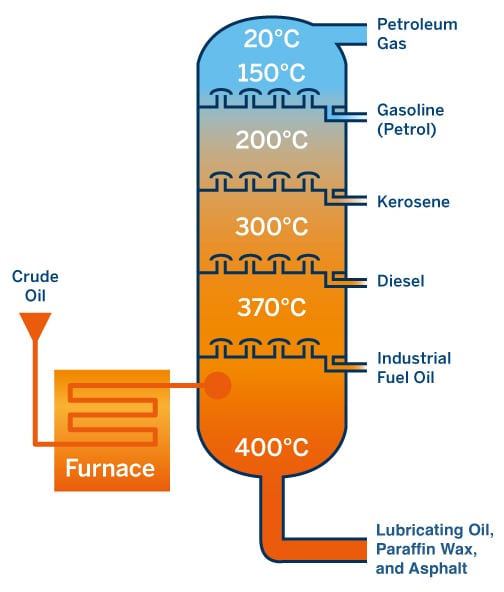

In the petroleum industry, refinery executives are most concerned about hedging the difference between their input costs and output prices. Refiners’ profits are tied directly to the spread, or difference, between the price of crude oil and the prices of refined products — gasoline and distillates (diesel and jet fuel).

This spread is referred to as a crack spread. It is referenced as a crack spread due to the refining process that “cracks” crude oil into its major refined products.

A petroleum refiner, like most manufacturers, is caught between two markets: the raw materials he needs to purchase and the finished products he offers for sale. The price of crude oil and its principal refined products are often independently subject to variables of supply, demand, production economics, environmental regulations and other factors. As such, refiners and non-integrated marketers can be at enormous risk when the price of crude oil rises while the prices of the refined products remain stable, or even decline.

Such a situation can severely narrow the crack spread, which represents the profit margin a refiner realizes when he procures crude oil while simultaneously selling the refined products into a competitive market. Because refiners are on both sides of the market at once, their exposure to market risk can be greater than that incurred by companies who simply sell crude oil, or sell products to the wholesale and retail markets.

In addition to covering the operational and fixed costs of operating the refinery, refiners desire to achieve a rate of return on invested assets. Because refiners can reliably predict their costs, other than crude oil, an uncertain crack spread can considerably cloud understanding of their true financial exposure.

Further, the investor community may use crack spread trades as a hedge against a refining company’s equity value. Other professional traders may consider using crack spreads as a directional trade as part of their energy portfolio, with the added benefit of its low margins (the crack spread trade receives a substantial spread credit for margining purposes). Together with other indicators, such as crude oil inventories and refinery utilization rates, shifts in crack spreads or refining margins can help investors get a better sense of where some companies— and the oil market may be headed in the near term.

{kind=link}

Hedging the Crack Spread

There are several ways to manage the price risk associated with operating a refinery. Because a refinery’s output varies according to the configuration of the plant, its crude slate, and its need to serve the seasonal product demands of the market, there are various types of crack spreads to help refiners hedge various ratios of crude and refined products. Each refining company must assess its particular position and develop a crack spread futures market strategy compatible with its specific cash market operation

1. Simple 1:1 Crack Spread

The most common type of crack spread is the simple 1:1 crack spread, which represents the refinery profit margin between the refined products (gasoline or diesel) and crude oil. The crack spread — the theoretical refining margin — is executed by selling the refined products futures (i.e., gasoline or diesel) and buying crude oil futures, thereby locking in the differential between the refined products and crude oil. The crack spread is quoted in dollars per barrel; since crude oil is quoted in dollars per barrel and the refined products are quoted in cents per gallon, diesel and gasoline prices must be converted to dollars per barrel by multiplying the centsper-gallon price by 42 (there are 42 gallons in a barrel). If the refined product value is higher than the price of the crude oil, the cracking margin is positive. Conversely, if the refined product value is less than that of crude oil, then the gross cracking margin is negative.

When refiners look to hedge their crack spread risk, they typically are naturally long the crack spread as they continuously buy crude oil and sell refined products. If refiners expect crude oil prices to hold steady, or rise somewhat, while products prices fall (a declining crack spread), the refiners would “sell” the crack; that is, they would sell gasoline or diesel (ULSD) futures and buy crude oil futures. Whether a hedger is “selling” the crack or “buying” the crack reflects what is done on the product side of the spread, traditionally, the premium side of the spread.

At times, however, refiners do the opposite: they buy refined products and sell crude oil, and thus find “buying” a crack spread a useful strategy. The purchase of a crack spread is the opposite of the crack spread hedge or “selling” the crack spread. It entails selling crude oil futures and buying refined products futures. When refiners are forced to shut down for repairs or seasonal turnaround, they often have to enter the crude oil and refined product markets to honor existing purchase and supply contracts. Unable to produce enough products to meet term supply obligations, the refiner must buy products at spot prices for resale to his term customers. Furthermore, lacking adequate storage space for incoming supplies of crude oil, the refiner must sell the excess crude oil on the spot market. If the refiner’s supply and sales commitments are substantial and if it is forced to make an unplanned entry into the spot market, it is possible that prices might move against it. To protect itself from increasing product prices and decreasing crude oil prices, the refinery uses a short hedge against crude oil and a long hedge against refined products, which is the same as “purchasing” the crack spread.

Diversified 3:2:1 and 5:3:2 Crack Spreads

There are more complex hedging strategies for crack spreads that are designed to replicate a refiner’s yield of refined products. In a typical refinery, gasoline output is approximately double that of distillate fuel oil (the cut of the barrel that contains diesel and jet fuel). This refining ratio has prompted many market participants to concentrate on 3:2:1 crack spreads — three crude oil futures contracts versus two gasoline futures contracts and one ULSD futures contract.

In addition, a refiner running crude oil with a lower yield of gasoline relative to distillate might be interested in trading other crack spread combinations, such as a 5:3:2 crack spread. This crack spread ratio is executed by selling the five refined products futures (i.e., three RBOB gasoline futures and two ULSD futures) and buying five crude oil futures contracts, thereby locking in the 5:3:2 differential that more closely replicates the refiner’s cracking margins.

3:2:1 crack spreads — three crude oil futures contracts versus two gasoline futures contracts and one ULSD diesel futures contract.

Further, professional traders may consider using diversified crack spreads as a directional trade as part of their overall portfolio. Also, the hedge fund community may use a diversified 3:2:1 or 5:3:2 crack spread trade as a hedge against a refining company’s equity value.

Factors Affecting Crack Spread Value

| # | Issue | Typically Affects | Crack Spread Effect |

| 1 | Geopolitical issues: Politics, geography, demography, economics and foreign policy | Crude oil supply | Crack weakens initially — higher crude oil prices relative to refined products. Crack strengthens later, as refineries respond to tighter crude oil supply and reduce product outputs. |

| 2 | Winter seasonality | Winter seasonality | Crack strength |

| 3 | Slower economic growth | Slower economic growth | Crack weakness |

| 4 | Strong sustained product demand | Strong sustained product demand | Crack strength |

| 5 | Environmental regulation on tighter product specifications | Tightening of product supply | Crack strength |

| 6 | Expiration of trading month | Expiration of trading month | Cracks values can vary due to closing of positions |

| 7 | Tax increase after certain date | Tax increase after certain date | Crack weakens in front of tax deadline and strengthens post deadline |

| 8 | Summer seasonality | Summer seasonality | Crack strength |

| 9 | Refinery maintenance | Refinery maintenance | Crack strength |

| 10 | Currency weakness | Crude oil strength | Crack weakness |

Cracks are affected by more forces than ever before:

- As investors shift funds into crude oil due to weakness in currencies, crude oil prices can quickly increase causing a decrease in crack spreads.

- The U.S. Renewable Fuels Standard’s blending requirements, which displace refinery hydrocarbon products with renewable products, impact crack spreads by weakening them by introducing new supply sources for demand needs.

Issues to Consider When Implementing Trades

1. Trade purpose? Trader must understand and be disciplined to trade purpose.

a. Refiner Hedge — Trying to hedge margins, shutdown time, capital asset purchase, or current market opportunity.

b. Investor Opportunity — Investor perceives market is over- or under-valued and desires to capture current market value. May also be using to complement another equity position in portfolio.

2. Crack ratio to implement? Simple 1:1 Crack Spread, Diversified 3:2:1 or 5:3:2 Crack Spread.

a. Refiner — Which crack spread matches your refinery configuration, crude type, and resultant product output?

b. Investor — Which crack spread matches perspective of investor or the refining entity’s configuration?

3. Time period (month, quarter, etc.) of trade?

a. If spot market is extremely strong, consider capturing some of that strength at the back of curve if it meets your hedge/trade goals.

b. Excessively weak market may elicit opportunities to buy undervalued crack spreads.

4. Buy or sell the Crack Spread?

a. “Buying” the crack spread means you “buy” the refined products while selling crude oil. This assumes you expect the crack spread will increase in value, i.e., from $5.00 per barrel to $6.00 per barrel.

b. “Selling” the crack spread means you “sell” the refined products while buying crude oil. This assumes you expect the crack spread will decrease in value, i.e., from $5.00 to $4.00 per barrel

Examples

Below are some crack spread trading examples.

Example 1 — Fixing Refiner Margins Through a Simple 1:1 Crack Spread

In January, a refiner reviews his crude oil acquisition strategy and his potential gasoline margins for the spring. He sees that gasoline prices are strong, and plans a two-month crude-to-gasoline spread strategy that will allow him to lock in his margins. Similarly, a professional trader can analyze the technical charts and decide to “sell” the crack spread as a directional play, if the trader takes a view that current crack spread levels are relatively high, and will probably decline in the future.

In January, the spread between April crude oil futures ($50.00 per barrel) and May RBOB gasoline futures ($1.60 per gallon or $67.20 per barrel) presents what the refiner believes to be a favorable 1:1 crack spread of $17.20 per barrel. Typically, refiners purchase crude oil for processing in a particular month, and sell the refined products one month later.

The refiner decides to “sell” the crack spread by selling RBOB gasoline futures, and buying crude oil futures, thereby locking in the $17.20 per barrel crack spread value. He executes this by selling May RBOB gasoline futures at $1.60 per gallon (or $67.20 per barrel), and buying April crude oil futures at $50.00 per barrel.

Two months later, in March, the refiner purchases the crude oil at $60.00 per barrel in the cash market for refining into products. At the same time, he also sells gasoline from his existing stock in the cash market for $1.75 per gallon, or $73.50 per barrel. His crack spread value in the cash market has declined since January, and is now $13.50 per barrel ($73.50 per barrel gasoline less $60.00 per barrel for crude oil).

Since the futures market reflects the cash market, April crude oil futures are also selling at $60.00 per barrel in March — $10 more than when he purchased them. May RBOB gasoline futures are also trading higher at $1.75 per gallon ($73.50 per barrel). To complete the crack spread transaction, the refiner buys back the crack spread by first repurchasing the gasoline futures he sold in January, and he also sells back the crude oil futures. The refiner locks in a $3.70 per barrel profit on this crack spread futures trade.

The refiner has successfully locked in a crack spread of $17.20 (the futures gain of $3.70 is added to the cash market cracking margin of $13.50). Had the refiner been un-hedged, his cracking margin would have been limited to the $13.50 gain he had in the cash market. Instead, combined with the futures gain, his final net cracking margin with the hedge is $17.20 — the favorable margin he originally sought in January.

In January, Refiner sells the 1:1 Gasoline Crack Spread Futures contract at $17.20:

Sells 1 May RBOB gasoline futures contract at $1.60 per gallon ($67.20 per barrel) Buys 1 April CL futures contract at $50.00 per barrel

Locks in the crack spread at $17.20 per barrel

In the Cash Market in March, Refiner sells the Gasoline Crack Spread at $13.50:

Sells 1000 barrels of physical gasoline at $1.75 per gallon ($73.50 per barrel) Buys 1000 barrels of physical crude oil at $60.00 per barrel

Receives a positive cracking margin of $13.50 per barrel

In March, Refiner buys back (liquidates) the 1:1 Gasoline Crack Spread Futures contract at $13.50 per barrel:

Buys 1 May RBOB gasoline futures contract at $1.75 per gallon ($73.50 per barrel) Sells 1 April CL futures contract at $60.00 per barrel

Futures gain of $3.70 per barrel (which can be applied to the cash market cracking margin)

Profit/Loss calculation:

Hedged crack spread = $17.20 per barrel

Un-hedged cash market cracking margin = $13.50

Example 2 — Refiner with a Diversified Slate Hedging with the 3:2:1 Crack Spread

An independent refiner who is exposed to the risk of increasing crude oil costs and falling refined product prices runs the risk that his refining margin will be less than anticipated. He decides to lock-in the current favorable cracking margins, using the 3:2:1 crack spread strategy, which closely matches the cracking margin at the refinery.

On September 15, the refiner decides to “sell” the 3:2:1 crack spread by selling two RBOB gasoline futures and one ULSD futures, and buying three crude oil futures, thereby locking in the 3:2:1 crack spread of $18.60 per barrel. He executes this by selling two December RBOB gasoline futures at $1.60 per gallon ($67.20 per barrel) and one December ULSD futures at $1.70 per gallon ($71.40 per barrel), and buying three November crude oil futures at $50.00 per barrel.

One month later, on October 15, the refiner purchases the crude oil at $60.00 per barrel in the cash market for refining into products. At the same time, he also sells gasoline from his existing stock in the cash market for $1.70 per gallon ($71.40 per barrel) and diesel fuel for $1.80 per gallon ($75.60 per barrel). The 3:2:1 crack spread value in the cash market has declined since September, and is now $12.80 per barrel.

Since the futures market closely reflects the cash market, November crude oil futures are also selling at $60.00 per barrel — $10 more than when he purchased them. December RBOB gasoline futures are also trading higher at $1.70 per gallon ($71.40 per barrel) and December ULSD futures are trading at $1.80 per gallon ($75.60 per barrel). To liquidate the 3:2:1 crack spread transaction, the refiner buys back the crack spread by first repurchasing the two gasoline futures and one ULSD futures he sold in January, and he also sells back the three crude oil futures. The refiner locks in a $5.80 per barrel profit on this crack spread futures trade.

The refiner has successfully locked in a 3:2:1 crack spread of $18.60 (the futures gain of $5.80 is added to the cash market cracking margin of $12.80). Had the refiner been un-hedged, his cracking margin would have been limited to the $12.80 gain he had in the cash market. Instead, combined with the futures gain, his final 3:2:1 cracking margin with the hedge is $18.60 — the favorable margin he originally sought in January.

On September 15, Refiner sells the 3:2:1 Crack Spread Futures contract at $18.60:

Sells 2 Dec RBOB gasoline futures contracts at $1.60 per gallon ($67.20 per barrel) Sells 1 Dec ULSD futures contract at $1.70 per gallon ($71.40 per barrel)

Buys 3 Nov CL futures contracts at $50.00 per barrel Locks in the 3:2:1 crack spread at $18.60 per barrel

One Month Later, in the Cash Market on October 15, Refiner sells the 3:2:1 Crack Spread at $12.80:

Sells 2000 barrels of physical gasoline at $1.70 per gallon ($71.40 per barrel)

Sells 1000 barrels of physical diesel at $1.80 per gallon ($75.60 per barrel) Buys 3000 barrels of physical crude oil at $60.00 per barrel

Receives a positive 3:2:1 cracking margin of $12.80

On October 15, Refiner buys back (liquidates) the 3:2:1 Crack Spread Futures contract at $12.80 per barrel:

Buys 2 Dec RBOB gasoline futures contracts at $1.70 per gallon ($71.40 per barrel) Buys 1 Dec ULSD futures contract at $1.80 per gallon ($75.60 per barrel)

Sells 3 Nov CL futures contracts at $60.00 per barrel

Futures gain of $5.80 per barrel (which can be applied to the cash market cracking margin)

Profit/Loss calculation:

Hedged 3:2:1 crack spread = $18.60 per barrel

Un-hedged cash market cracking margin = $12.80

Example 3 — Purchasing a Crack Spread (or Refiner’s Reverse Crack Spread)

The “purchase” of a crack spread is the opposite of the crack spread hedge or “selling” the crack spread. It entails selling crude oil and buying refined products. Refiners are naturally long the crack spread as they continuously buy crude oil and sell refined products. At times, however, refiners do the opposite: they buy refined products and sell crude oil, and thus find “purchasing” a crack spread a useful strategy.

When refiners are forced to shut down for repairs or seasonal turnaround, they often have to enter the spot crude oil and refined products markets to honor existing purchase and supply contracts. Unable to produce enough refined products to meet supply obligations, the refiner must buy products at spot prices for resale to customers. Furthermore, lacking adequate storage space for incoming supplies of crude oil, the refiner must sell the excess crude oil in the spot market.

If the refiner’s supply and sales commitments are substantial and if it is forced to make an unplanned entry into the spot market, it is possible that prices might move against it. To protect itself from increasing refined products prices and decreasing crude oil prices, the refinery uses a short hedge against crude oil and a long hedge against refined products, which is the same as “purchasing” the crack spread.

The “reverse crack spread” is also a useful strategy for professional traders as a directional move if traders take a view that current crack spread levels are relatively low, and will probably rise in the future.

In this example, the refiner is planning for upcoming maintenance, and decides to “buy” the simple 1:1 crack spread in January by buying RBOB gasoline futures, and selling crude oil futures, thereby locking in the current $17.20 per barrel crack spread value. He executes this by buying May RBOB gasoline futures at $1.60 per gallon (or $67.20 per barrel), and selling April crude oil futures at $50.00 per barrel.

Two months later, in March, when the refiner begins the refinery maintenance, he sells the crude oil at a lower price of $40.00 per barrel in the cash market because of the refinery closure. At the same time, he also buys gasoline in the spot market for $1.70 per gallon, or $71.40 per barrel. The crack spread value in the cash market has increased since January, and is now $31.40 per barrel ($71.40 per barrel gasoline less $40.00 per barrel for crude oil).

Since the futures market reflects the cash market, April crude oil futures are also selling at $40.00 per barrel in March — $10.00 less than when he purchased them in January. May RBOB gasoline futures are trading higher at $1.70 per gallon ($71.40 per barrel). To complete the crack spread transaction, the refiner liquidates the crack spread by first selling the gasoline futures he bought in January, and he buys back the crude oil futures, at a current level of $31.40 per barrel. The refiner locks in a $14.20 per barrel profit on this crack spread futures trade ($31.40 per barrel less the $17.20 per barrel crack spread in January).

The refiner has successfully hedged for the rising crack spread (the futures gain of $14.20 is added to the cash market cracking margin of $17.20). Had the refiner been unhedged, his margin would have been limited to the $17.20 gain he had in the cash market. Instead, combined with the futures gain, his final net cracking margin with the hedge is $31.40.

In January, Refiner buys the 1:1 Gasoline Crack Spread Futures contract at $17.20:

Buys 1 May RBOB gasoline futures contract at $1.60 per gallon ($67.20 per barrel) Sells 1 April CL futures contract at $50.00 per barrel

Hedges the crack spread at $17.20 per barrel

In the Cash Market in March, Refiner buys the Gasoline Crack Spread at $31.40:

Buys 1000 barrels of physical gasoline at $1.70 per gallon ($71.40 per barrel) Sells 1000 Barrels of physical crude oil at $40.00 per barrel

The cracking margin has increased to $31.40 per barrel

In March, Refiner sells (liquidates) the 1:1 Gasoline Crack Spread Futures contract at $31.40 per barrel:

Sells 1 May RBOB gasoline futures contract at $1.70 per gallon ($71.40 per barrel) Buys 1 April CL futures contract at $40.00 per barrel

Futures gain of $14.20 per barrel (which is applied to the $17.20 crack spread from January)

Profit/Loss calculation:

Hedged crack spread = $31.40 per barrel

Un-hedged cash market cracking margin = $14.20

For more information about Crack Spreads, please contact Dan Brusstar at daniel.brusstar@cmegroup.com

To learn more about our suite of Energy products, visit cmegroup.com/energy or email energy@cmegroup.com