{kind=link}

FX Options Vol Converter User Guide and Methodology

This document is designed to be a user guide to highlight the functionality of the FX Options Vol Converter.

Overview

The FX Options Vol Converter converts the extensive listed options pricing available on the CME, into an OTC-equivalent volatility surface, allowing OTC users to easily compare pricing and optimize execution.

- Available for 5 currency pairs: EUR/USD, JPY/USD, GBP/USD, AUD/USD, CAD/USD

- Provides live updates between 1am and 4pm CST. Outside of these hours, the Settle view described below will be displayed and remain available as a view options during the live session.

- All of the views in the FX Options Vol-Converter display OTC-equivalent values derived from CME traded premium quotes using the process described in the Methodology. These values are displayed using OTC conventions, such that for the inverted CME pairs of JPY/USD and CAD/USD, the display represent values in USD/JPY and USD/CAD format (Puts and Calls are on the USD). However, the Drilldown window (explained below) retrieves the original CME contract formats and data (so inverted strikes and types, i.e. Puts and Calls are on the JPY).

- The Risk Reversal (RiskRev) values in the Summary View are displayed as Call-Put. E.g. in EUR/USD this means EUR Call-EUR Put, in USD/JPY it means USD Call-USD Put.

Select your view

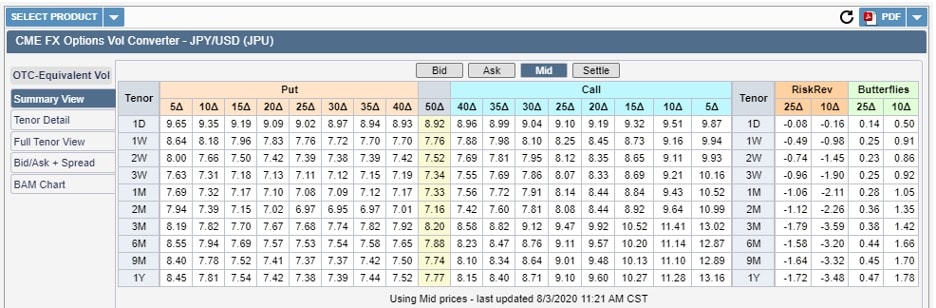

1. summary view:

The OTC Surface summary view shows the OTC-equivalent implied volatility surface at fixed tenors and deltas from a converted CME live price stream, with the ability to see a particular side of the market (Bid, Mid, Ask or Settle) that is of interest (see figure 1). The Settle view provides an OTC-equivalent surface based on CME’s daily 2 p.m. settlement values and is available for reference until the close of the next trading day.

Figure 1: Summary view

{kind=link}

The OTC-Equivalent Vol surface can be refreshed by clicking on the browser button shown below:

{kind=link}

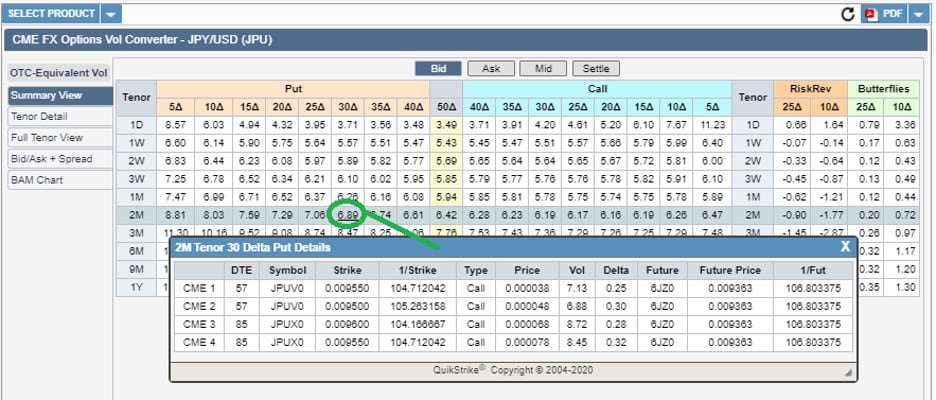

In the Summary view, a drill down functionality may be accessed by clicking on any bucket on the surface (see figure 1a). This will highlight the underlying CME instruments most closely associated with the implied volatility value within the bucket and show the unadjusted pricing data for each. This view allows you to quickly find the associated instruments on CME and recognize the option/futures price combination that feeds into the OTC-equivalent volatility.

For example, in Figure 1a below, when selecting the USD/JPY 2M tenor 30 Delta Put with an OTC-equivalent volatility of 6.89, the dropdown populates the specific CME contract info underlying this value: two October JYP/USD Call Options (JPUV00), two November JPY/USD Call Options (JPUXV0), and their associated DTE (Days To Expiration). It also shows their strikes, prices, deltas, underlying future, and future price. For inverted CME pairs such as JPY/USD and CAD/USD, there are two additional columns (1/Strike) and (1/Fut) displaying the inverse value for the strike and future price to provide a quick confirmation in OTC-like convention.

Figure 1a: OTC Surface drilldown

{kind=link}

2. Tenor Detail view:

The Tenor Detail view compares contributing CME instruments nearest a specific tenor bucket, depicting a graph of the full delta curve. As with the OTC Surface view, you can drill down on a tenor/delta bucket and view a specific side of the market (Bid, Mid, Ask, or Settle).

Figure 2 below shows the OTC-equivalent implied volatility of the EUR/USD 2W tenor (row 2 in the table) alongside the underlying CME contracts most closely associated with this specific option tenor, the September EUR/USD Options (EUUU0) and October EUR/USD Options (EUUV0) ‒ in rows 1 and 3 respectively. The OTC-equivalent volatilities for each are depicted in the graph to show the full delta curve, allowing you to easily compare implied volatility measures of fixed tenors and deltas to associated CME instruments. Please note that when one of the CME contracts has an equivalent DTE to the OTC tenor, the two curves will be identical, and the green graph line will cover the CME line such that only two curves will be visible.

Figure 2: Tenor Detail

{kind=link}

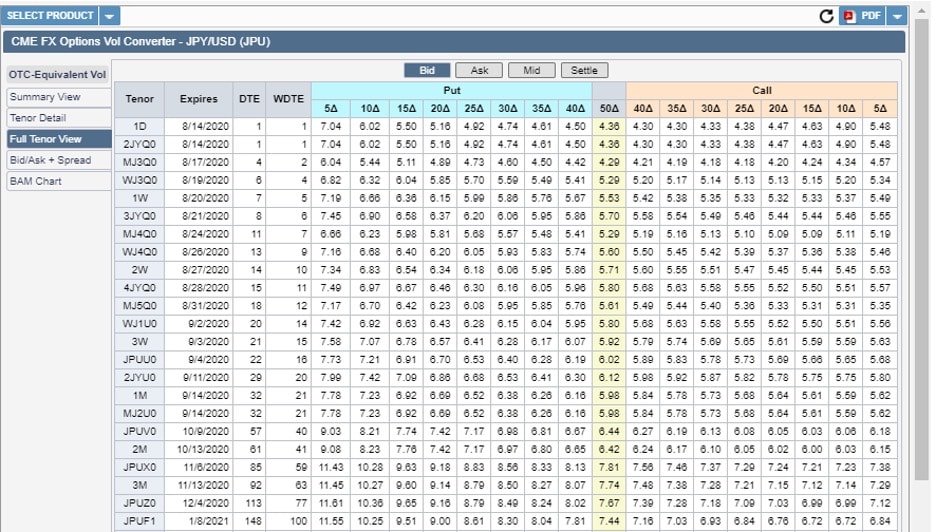

3. Full Tenor view:

The Full Tenor view is an extended surface detailing the implied volatilities of fixed tenors and associated CME contracts intermingled for an overview of the full surface.

Figure 3: Full Tenor view

{kind=link}

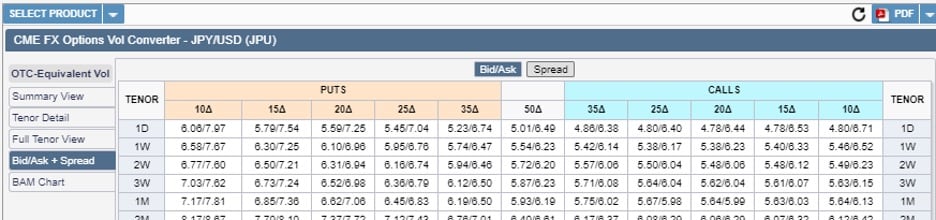

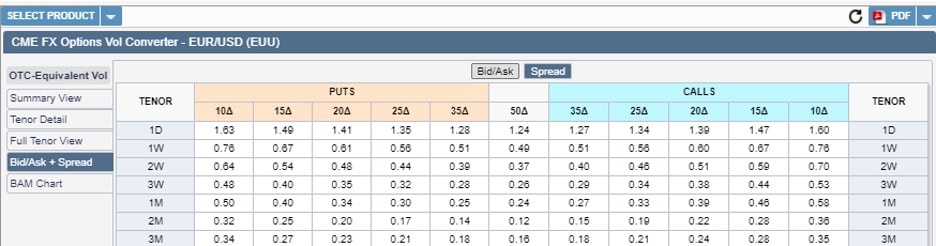

4. Bid/Ask view + Spread

The Bid/Ask + spread view shows the bid and ask implied volatility values in one view for convenience (Figure 4). It also can display the spread between bid and ask (Figure 4a) to help identify areas of trader focus (a tighter spread may reflect active two-way engagement in that specific area of the curve).

Figure 4: Bid/Ask view

{kind=link}

Figure 4a: Spread view

{kind=link}

5. BAM Chart

The BAM Chart display graphically the vol smile for the Bid/Mid/Ask for a select Tenor.

{kind=link}

Methodology

The below provides a basic overview of the process, a more technical description will be available in a separate research paper to be published soon.

The conversion process:

- Extract bid/ask premium price for all strikes and maturities in CME FX pairs

- Adjust for the difference in the underlying by converting CME strikes to OTC equivalent strikes

- Align quote format as needed by flipping CME American term to OTC European term (i.e. USD/JPY, USD/CAD)

- Adjust CME strike by removing the expected forward swap differential between spot and future at option expiration - Back out volatility from premium price attached to new OTC equivalent strikes

- Use a SABR stochastic volatility model to build an interpolated delta/volatility surface used to:

- Generate an implied volatility run at standard OTC Tenor and Delta buckets

- Allow drilldown on any of the standard OTC tenor/delta bucket to view the original details of the nearest CME contracts (up to 4) most responsible for that interpolated OTC-equivalent value. - Steps above performed for the mid, bid and ask side of the vol surface to allow trade level comparison

Some of the Math:

Converting American Term to OTC Term

Let’s assume replicates the payoff V of a long XXXUSD call option with strike K and maturity T. For to be equivalent one has to buy K units of USDXXX put option with strike . Finally, we multiply the ratio by to change the premium currency from USD to XXX.

{kind=link}

Where:

We need to know the value of ϕ at time t, however we only know its value at time Texp. Given the information we have at time t, the expectation of ϕ should be a good approximation of ϕ. Such expectation is observable at time t, as Fut(t,TdelCME ) is traded on the CLOB and Fwd(t,Texp ) can be interpolated from the OTC forward curve:

Changing Option Underlying from Future to Spot

We define Vspot as the premium of a CME option delivering on the OTC value date (Tdelotc), and, Vfut the premium of a CME option with a future underlying (TdelCME). Both options share the same expiry date Texp. The two option premiums are equal if we make a small adjustment to Vspot strike, called Kspot, to consider the future-spot basis ϕ. The equation below defines the relationship in detail.

{kind=link}

SABR Calibration to OTC-Equivalent premium

Objective function

{kind=link}

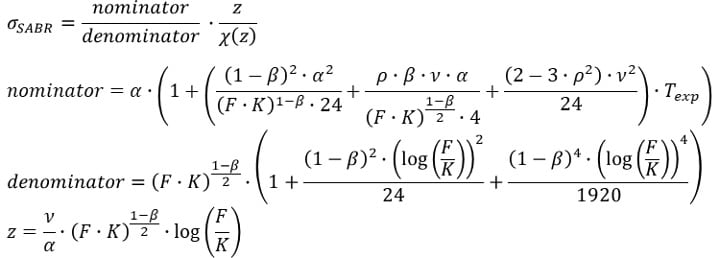

SABR

{kind=link}

Unconstrained Optimizer with Bounded Interval for SABR parameters:

{kind=link}

For more information

Visit The FX Options Vol Converter to start using the tool.

For questions about this tool, contact FXteam@cmegroup.com.

CME FX Products

CME Group offers the largest regulated marketplace for FX in the world, covering more than 40 currency pairs across both G10 and EM.

CME Direct

Made for block execution certainty and compliance, with the convenience of our highly-configurable front-end.