https://www.cmegroup.com/content/dam/cmegroup/education/images/2020/assessing-liquidity984x137.jpg

{kind=link}

Assessing liquidity – Revisiting whether book depth is a sufficiently representative measure of market liquidity

This article looks to revisit an analysis on how to gauge liquidity which initially was compiled after the market downturn in Q4 2018.[1] This framework is applied to the recent market conditions we have witnessed in Q1 2020.

It looks to compare trade matching performance under different market volatility environments.

Executive Summary:

- Order book depth in isolation is not the correct method to gauge “liquidity”.

- An analysis of fill quality via metrics, such as price impact together with density functions, relating to volume can provide a more insightful picture into “liquidity”.

- Analysis shows that in the week starting 16 March 2020 when volatility rose over 7x to over 75%, E-mini S&P 500 futures traded at 85% more volume despite the orderbook depth decreasing by 90% (vs. the week of 20 January 2020).

- The average fill rate per second was approximately 100% higher in the week of 16 March 2020 (vs. the week of 20 January). The degradation in fill quality was a maximum 7.5 ticks (1.875 index points, approximately 7.5 basis point of the value of the instrument) based on a trading volume of 275 contracts.

- This was a reasonable re-pricing of risk, given the rapid acceleration in volatility.

- In April 2020, the fill quality improved and thus the magnitude of degradation seen in late March was temporary.

Introduction:

The first quarter of 2020 witnessed the impact of the coronavirus crisis on equity markets. It resulted in the highest level of volatility in recent decades and precipitated the quickest bear market in history with the S&P 500 index falling by over 20% in just 16 days. Within the quarter the index fell from a close of 3,386.15 on February 19 to 2,237.40 on March 23, a drop of almost 34%. The implied volatility of S&P 500 peaked at over 75% vs. an average of roughly 13% witnessed throughout 2019.[2]

These periods of greater volatility or stress often result in some market observers commenting on a “lack of liquidity” in the market. The source of this conclusion is typically the fact that the depth of the “displayed top of order book” has seen a significant reduction.

When these volatile episodes occur, a reduction in the displayed top of order book is often expected given the increase in risk, however it is just one metric and can result in an incomplete picture of “liquidity” being ascertained. Indeed, if one was to just look at another metric in isolation, e.g. volume, one would come to a completely different conclusion on whether a market was deemed to be liquid or not.

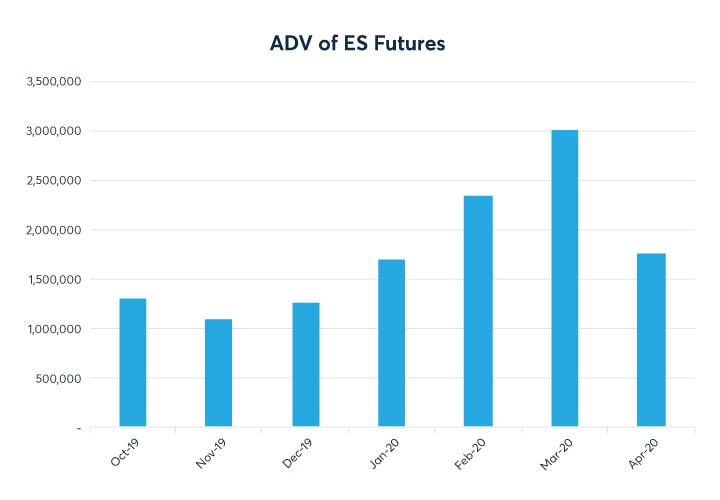

Figure 1. Average daily outright volume of E-mini S&P 500 index futures[3]

| Month | ADV |

| Oct-19 | 1,294,448 |

| Nov-19 | 1,089,364 |

| Dec-19- | 1,269,394 |

| Jan-19 | 1,696,133 |

| Feb-19 | 2,335,776 |

| Mar-19 | 3,008,383 |

| Apr-19 | 1,757,541 |

https://www.cmegroup.com/content/dam/cmegroup/education/images/2020/assessing-liquidity-fig01.jpg

{kind=link}

Source: CME Group

If we look at Figure 1, we can see that during the volatile period of March 2020 the volume was approximately 3x that of November 2019 and 1.8x that of January 2020. Thus, based on analyzing liquidity with a volume metric alone, the E-mini S&P 500 futures market would appear much more liquid in March 2020 than in the last quarter of 2019 and the start of 2020. The two metrics outlined so far, book depth and volume, appear inconsistent to each other and result in different conclusions. Therefore, both need to be better contextualised.

A better way to assess liquidity is to assess one’s ability to execute an order with the smallest market impact possible. Another way to think about this is the “fill quality” of an order.

The central limit order book is a repository for currently unmatched orders. Passive market participants supply two-way orders in the order book and provide liquidity to the market. Other aggressing participants send a single-sided order to buy or sell into the order book and can be viewed as demanding liquidity. When the velocity of trading accelerates, the quote refresh rate of those making markets and providing passive order flow at the top of the book often increases as a response to serve the increased demand of aggressing single-sided orders.

Thus, it is not always valid to assume that a low level of resting volume at the top of order book signifies a lack of “liquidity.” High refresh rates of quoting at the top of the order book, may result in all the inbound buy and sell orders being served without the price moving, despite the order book depth being lower than in a slower paced trading environment.

Indeed, the definition of a liquid market is that a large quantity of transaction can be executed without significant impact to the arrival price. If that is the case, it is hard to argue that the market is illiquid just because there are less idle orders in the book. The “fill quality” as a function of execution prices versus arrival prices of the transactions should be considered before this illiquidity conclusion can be reached.

At the end of this article, the conclusion is that liquidity in the E-mini S&P 500 index futures, measured in terms of fill quality, did decline during the volatile period of March 2020, but to a more moderate and understandable extent than an analysis of book depth in isolation would lead one to believe. When contextualized with several different metrics together with market conditions, it is evident that liquidity was still available but had been rationally re-priced, as to be expected, to reflect the prevailing risk conditions.

Looking at order book depth:

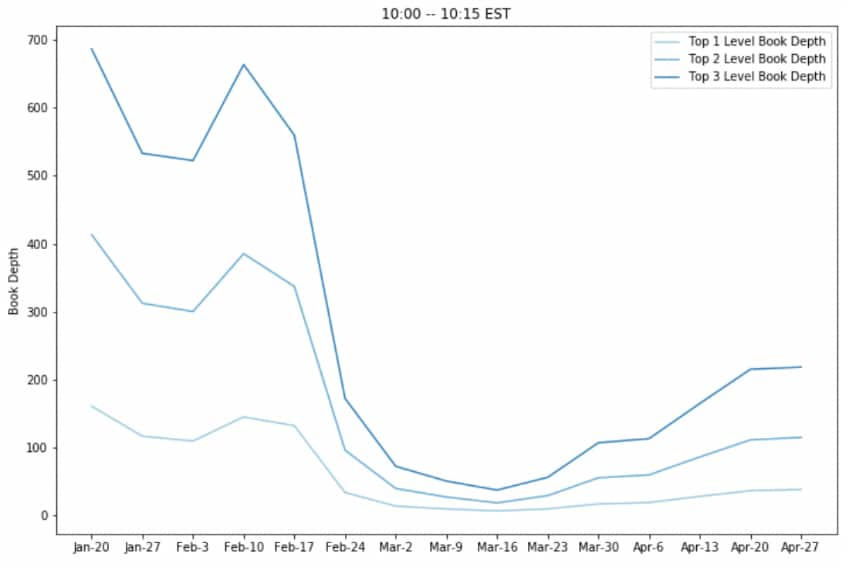

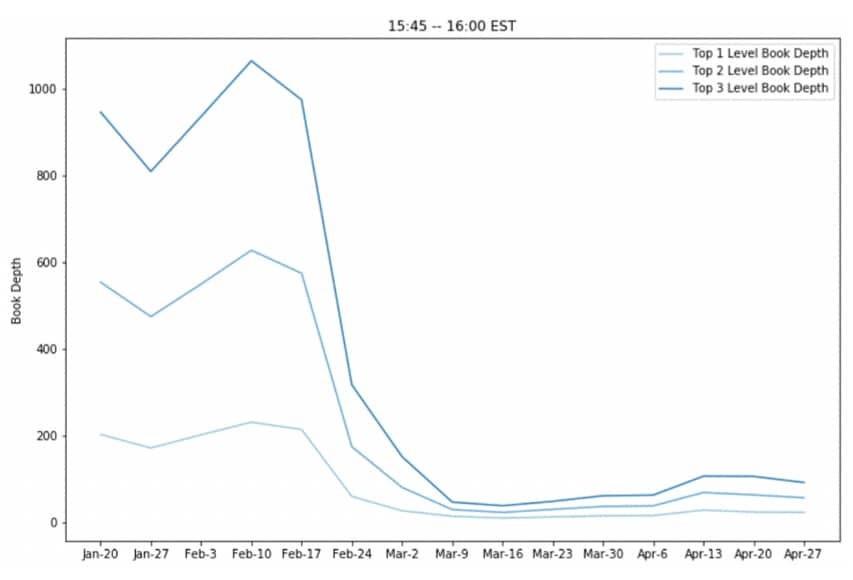

Figure 2 shows the average book depth by week in the period from 20 January 2020 through the week starting 27 April 2020. The book depth at the top one, two, and three levels for the middle weeks of March 2020 appeared to have dropped by approximately 90%, when compared to the first few weeks of the period. The conclusions apply similarly to two different 15-minute time slices within the trading day, one from the morning and one towards the end of the cash trading day. During April 2020, once the peak levels of volatility started to subside, the book depth recovered somewhat for the morning period but only by a minor amount for the end of the trading day. This empirically backs up the assertion that book depth declined as the market became more volatile but does not provide any indication of the quality of the fills.

Figure 2. Average central limit order book depth for E-mini S&P 500 Index futures[4]

https://www.cmegroup.com/content/dam/cmegroup/education/images/2020/assessing-liquidity-fig02.jpg https://www.cmegroup.com/content/dam/cmegroup/education/images/2020/assessing-liquidity-fig03.jpg

{kind=link}

{kind=link}

Source: CME Group

Price dispersions:

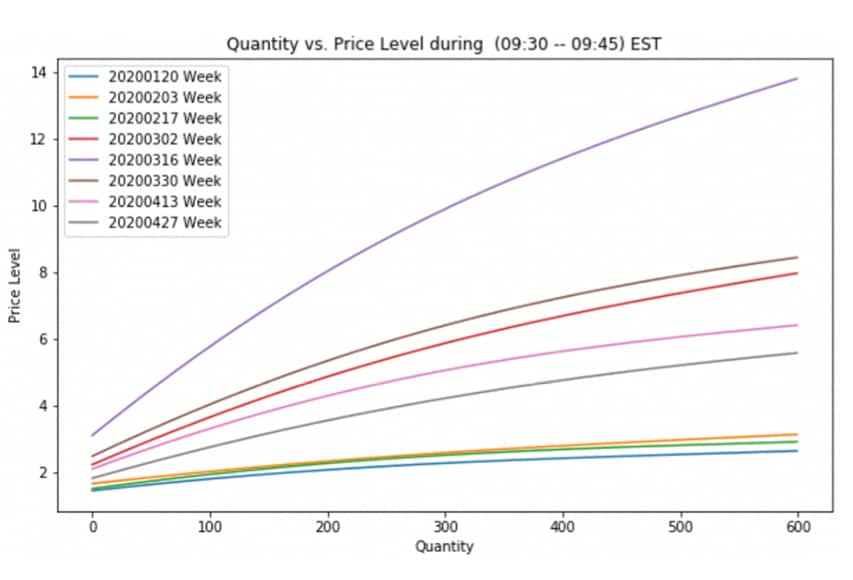

To measure fill quality, we propose to first look at the price range of transactions that occur in close temporal proximity to each other. In a liquid market, the range would be narrow; whereas the range would be wide in an illiquid market. Since E-mini S&P 500 index futures are continuously traded, one could group all the trades consummating within the same second and find out the trading range within each one-second interval. Since the prices only move in fixed minimum price increments, the number of prices traded within that one second interval signifies the trading range.

Figure 3 provides a comparison of price dispersion in relation to the rate of trading in a certain week. These weekly periods were taken at two-week intervals starting from 20 January 2020 through to the week starting 27 April 2020. For example, if all the trades within the one-second interval have an identical price, the number of prices would naturally be one. If trades bounce between the top bid and offers without exhausting either, the number of prices would be two. Thus, the lower bound for the measure would be one. When the trading volume is light, this measure tends to average close to one. As the trading volume that occurs within a single second increases, the number of different prices consummated within that time frame also increases, as the top of the order book together with the refreshing of quotes at the top of the order book are insufficient to cater for the volumes being transacted.

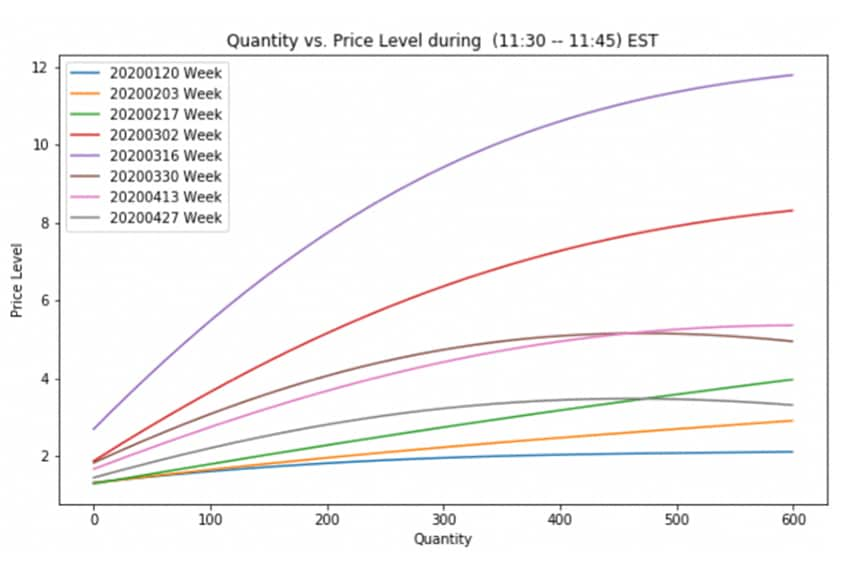

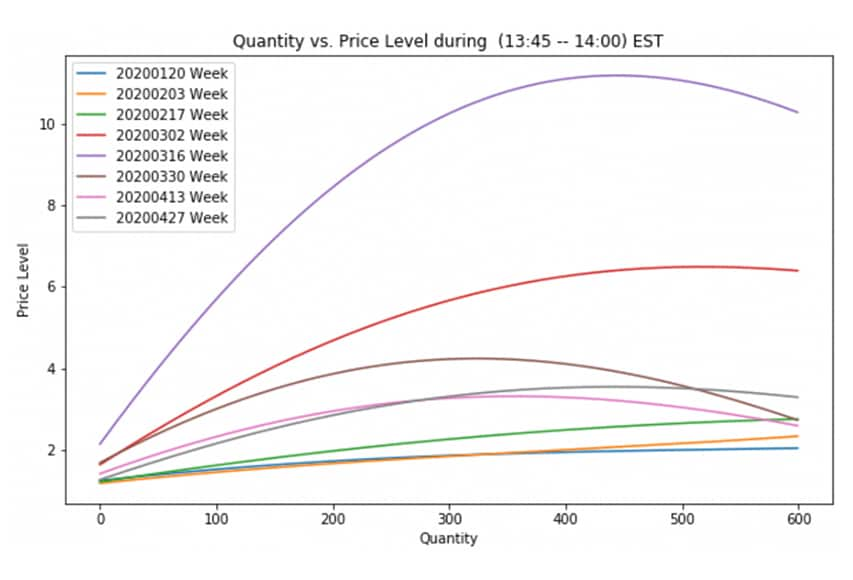

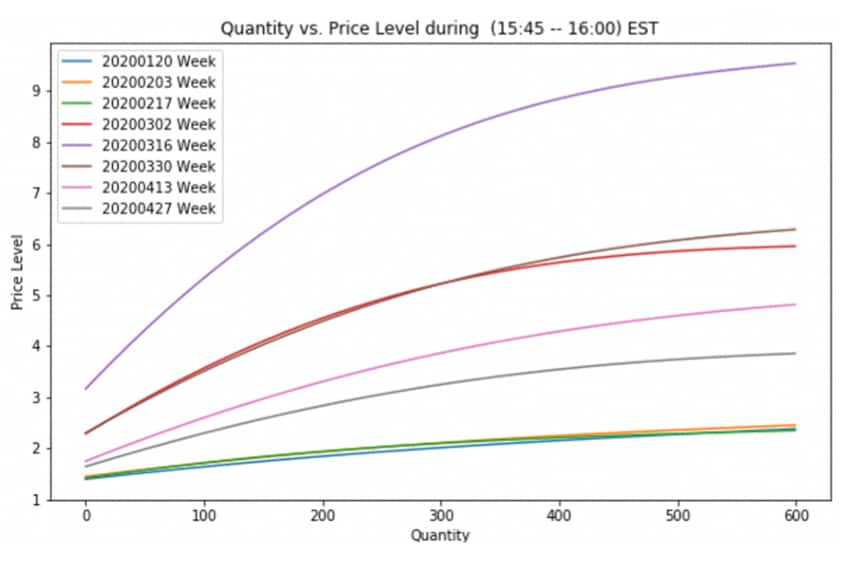

Figure 3 illustrates wherethe x-axis denotes the rate of trading, i.e. number of contracts traded per second, whilst the y-axis denotes the level of price dispersion. At a low rate of trading, the price dispersion (i.e. the average number of traded prices) is low (one or two prices incurred). As the rate of trading increases, the top level of the order book gets depleted, and the price moves onto the next level. Thus, the average number of prices will increase. Below it applies this methodology to four different 15-minute time slices of the trading day.

Figure 3. Price dispersion measure vs. trading volume per second

https://www.cmegroup.com/content/dam/cmegroup/education/images/2020/assessing-liquidity-fig04.jpg https://www.cmegroup.com/content/dam/cmegroup/education/images/2020/assessing-liquidity-fig05.jpg https://www.cmegroup.com/content/dam/cmegroup/education/images/2020/assessing-liquidity-fig06.jpg https://www.cmegroup.com/content/dam/cmegroup/education/images/2020/assessing-liquidity-fig07.jpg

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Source: CME Group

The y-axis serves as a proxy to the trading range whilst the x-axis denotes the trading volume per second. For example, in the week starting 20 January during the 15-minute window of each day for 9:30 a.m.-9:45 a.m. Eastern Standard Time (EST) (blue line in the top left panel), a trading rate of 100 contracts per second would on average have approximately a trading range of 1.8 prices (or ticks).

Each line represents the estimated average price range within a second for each week during the time frame indicated in the heading of each chart. A wider dispersion of prices, after controlling for trading volume, indicates a less liquid market.

In a low volatility environment, like the week starting 20 January, the increase in trading rate is associated with a relatively low increase in the trading range. In a volatile market environment such as in the week starting 16 March (purple line), the same increase in trading rate will be associated with a more significant increase in the trading range. This can be seen from the four panels in Figure 3, and this in isolation could be taken as an indication that the market in the second half of March 2020 was significantly less liquid than in late January 2020. It then appears during April 2020 the price dispersion calms down and reverts towards the late January 2020 environment.

However, this analysis is still incomplete and needs to be contextualized together with volume. The extent of the fill quality degradation is an interesting aspect to be examined.

A set of complementary graphs to show the trading volume pattern will be introduced below to put the comparison in proper context.

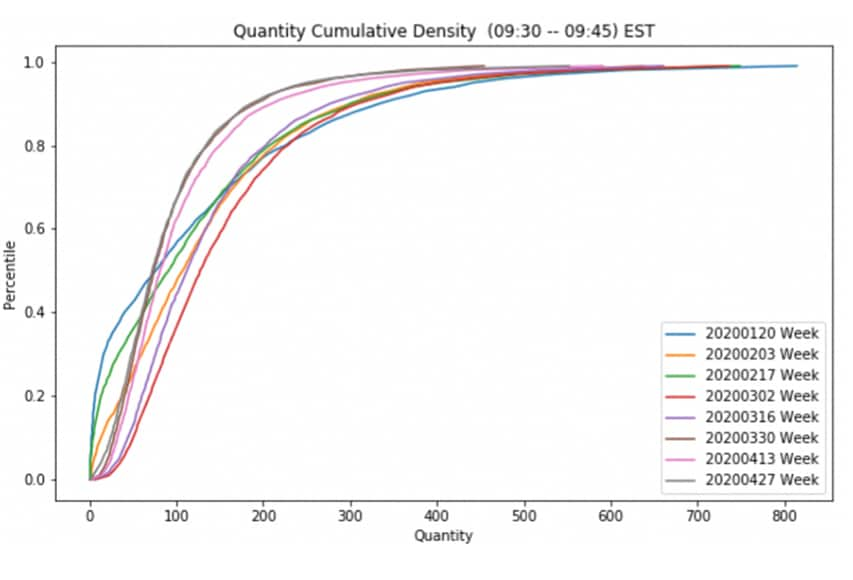

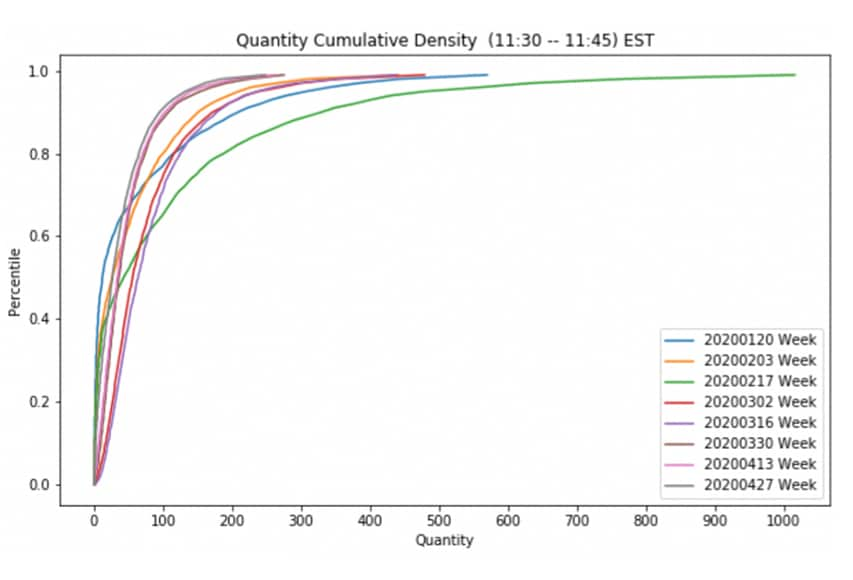

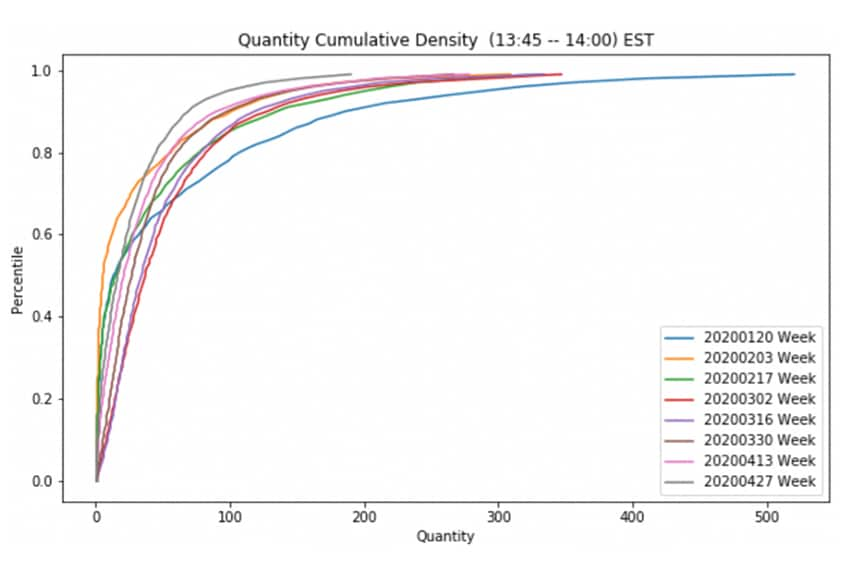

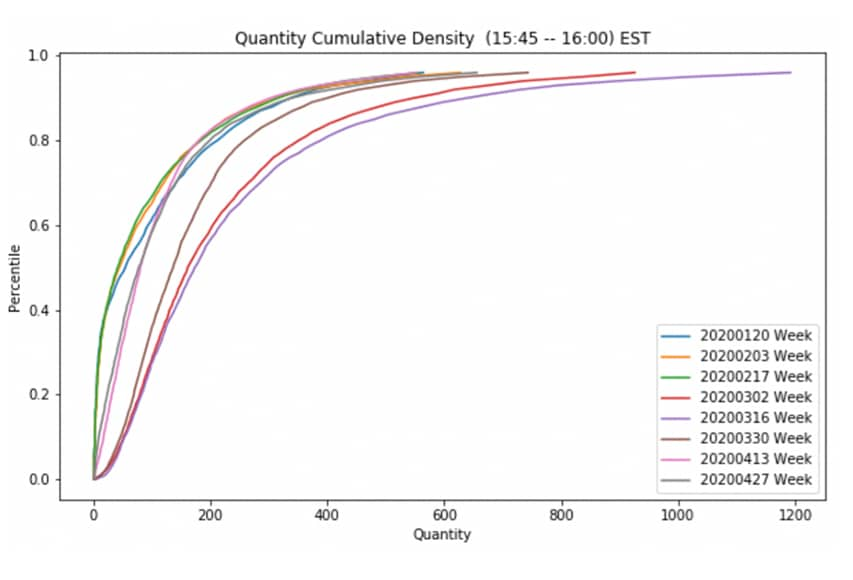

Figure 4. Cumulative density function of trading volume per second

https://www.cmegroup.com/content/dam/cmegroup/education/images/2020/assessing-liquidity-fig08.jpg https://www.cmegroup.com/content/dam/cmegroup/education/images/2020/assessing-liquidity-fig09.jpg https://www.cmegroup.com/content/dam/cmegroup/education/images/2020/assessing-liquidity-fig10.jpg https://www.cmegroup.com/content/dam/cmegroup/education/images/2020/assessing-liquidity-fig11.jpg

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Source: CME Group

In each graph, the y-axis represents the cumulative probability and X-axis represents trading volume per second. For example, during the 15-minute window each day of 3:45 p.m. - 4 p.m. EST in the week staring on 20 January (blue line, top left panel), trading at approximate 55 contracts per second or less has a cumulative density of 0.50. In other words, the 50th percentile of trading volume per second is approximately 55. The same 50th percentile of per second trading rate is over 170 for the week starting on 16 March. The cumulative density function for the week of 16 March lies to the right of that of the week of 20 January, meaning the rate of trading for 16 March week was much higher than that of 20 January week. Once volatility started to subside in April 2020, we can see the rate of trading for the 50th percentile revert towards levels seen during the week of 20 January.

Rate of trading:

Figure 4 shows the range of trading for the weeks from 20 January 2020 to 27 April 2020. It is a well-known fact that trading concentrates a lot around the time of cash market open (9:30 a.m. EST) and close (4 p.m. EST). The rate of trading is typically lower during the middle of the U.S. trading day.

For the week of 20 January, the 50th percentiles of trading rate were approximately 65 (contracts per second) around the cash market open and close and 12 around the middle of the U.S. trading day.

If we contrast this with the rate of trading in the week of 16 March, the same 50th percentiles were in most cases at least double those of the week of 20 January.

Equipped with this set of graphs, one can observe that 90% of the time (i.e. the 90th percentile), the trading rate was approximately at or below 275 contracts per second for the cash market open and close. The rate is at or below approximately 175 contracts per second around the middle of the trading day 90% of the time.

Magnitude of the increase in price dispersion:

By using the trading rates of 275 and 175 (i.e. the 90th percentile) for the market open/close and middle of the trading day and applying these quantities to the price dispersion charts shown in Figure 3, the magnitude of the increase in price dispersion between two different periods can be identified

Cash market open/close - at 275 contracts per second, the average number of traded prices increases from approximately 2.1 on 20 January to 9.6 on 16 March. In other words, 90% of the time the price dispersion for the week of 16 March (the least liquid and the most volatile week) was at most 7.5 ticks wider than the week of 20 January (a far more liquid and less volatile week).

Middle of the day – at 175 contracts per second, the price dispersion for 90% of the time increased from 1.7 (11:30am, 20 January) to about 7.3 (11:30am, 16 March), an increase of 5.6 ticks at most.

By the end of April 2020, the price dispersion for a trading rate of 275 and 175 had fallen back to 3.1 and 2.7, respectively, which is just 1 tick more than that found in the low volatility week of 20 January. This shows how the market adjusted to price risk more expensively, when volatility was at its peak in middle to late March and cheapened thereafter as volatility subsided. The relationship between volatility and cost to trade appears to hold as one would expect.

It is worth noting that the significant retracement in market impact costs for April is at odds with the conclusions from the book depth charts found in Figure 2, suggesting “fill quality” is a superior way to assess “liquidity.”

Concluding remarks:

Traditional indicators of liquidity such as order book depth and price dispersion, if taken in isolation, provide an incomplete picture indicating that the market was less liquid in the week of 16 March than in late January. However, 90% of the time during the US trading day, this increase of price dispersion was no more than 7.5 ticks (or 1.875 index points at the open/end of the cash trading day and no more than 5.6 ticks during the middle of the day (or 1.4 index points). Expressed in another way, 90% of the time it cost a maximum of 7.50bps more to trade 275 contracts.[5]

This increase in the trading range is to be expected when put into context. The market incurred the fastest bear market in history and during the week of 16 March alone, the S&P 500 index fell from 2,711.02 to 2,304.92, a fall of 15% with an 11% drop on the first day of that week. The volatility rose to over 75% during the week of 16 March, yet it was below 10% during the week of 20 January. The surge in the pace of market movements meant it was rational for a unit of risk to be priced more expensively, given the extraordinary market conditions. As market conditions eased in April, the market impact of a given quantity of risk reduced and moved towards the low market impact environment seen in late January 2020.

As pointed out in Figure 2, the book depth decreased by 90% and this fact in isolation could lead one to incorrectly conclude that the market in mid- to late-March 2020 was “illiquid”, and few transactions were able to occur. However, record volume was still able to be transacted, in fact at a rate of nearly twice as much as late January 2020. Given this, it is hard to argue that the market was “illiquid” in some absolute sense. The “fill quality” did degrade but not to the extent that looking at book depth would lead one to believe – or indicate an inability to access the market or manage the risk required.

The deeper analysis shown here indicates that the market adjusted to price risk more expensively, at logical levels, due to the rapid acceleration in volatility. The April 2020 data shows this was a temporary phenomenon, and the market impact of an order started to revert towards the conditions found prior to the market sell off in March.

In summary, to measure liquidity and to understand one’s ability to access the market, one must look beyond book depth and consider other metrics, such as price dispersion and rate of trading, that will help to contextualize fill quality.

A note on the methodology

The price dispersion charts are constructed in the following manner: for each second of trading, the volume traded in the lead month of the E-mini S&P 500 index futures as well as the range of traded prices, expressed in the form of number of traded prices, are recorded. These data points are sorted into the corresponding 15-minute windows.

Using the data points collected in the 15-minute windows, the curve representing the average price range in relation to the volume traded per second was estimated by applying kernel regression techniques. It is akin to finding the weighted “local” average (i.e. the average price dispersion at a given level of trading volume rate) without imposing too many assumptions on the underlying probability distributions of the data.

Similarly, the cumulated density functions are produced based on kernel density estimation methodology.

Sources

- CME Group

- Source: Quikstrike for ’30-Day ATM Constant Maturity’

- Note that “calendar spreads” trades, or rollover volume, are excluded from the data, as those are position management trades that were separate entering and exiting positions in E-mini S&P 500 futures per se, the inclusion of which would obscure the “illiquidity” picture.

- The graphs are the cumulative limit order book quantity for E-mini S&P 500 index futures by month at the top three price levels. Average of the bid/ask quantities are sampled once per second for each of the fifteen-minute intervals from the lead-month futures outright order book.

- Based on an index level of 2500