{kind=link}

3-Year Treasury Note futures ‒ Yield curve spreads

The July 13, 2020 relaunch of 3-Year Treasury Note futures has created new yield curve spread opportunities on the US Treasury futures curve. In August, CME Globex-listed curve spreads accounted for 15% of trading volume in 3-Year Note futures. 2Y vs. 3Y (Globex code TYT) and 3Y vs. 5Y (Globex code TOF) spreads account for the majority of activity, but 3Y vs. 10Y (Globex code TUN) and 3Y vs. Ultra 10Y (Globex code TYX) spreads have seen growing activity in recent weeks.

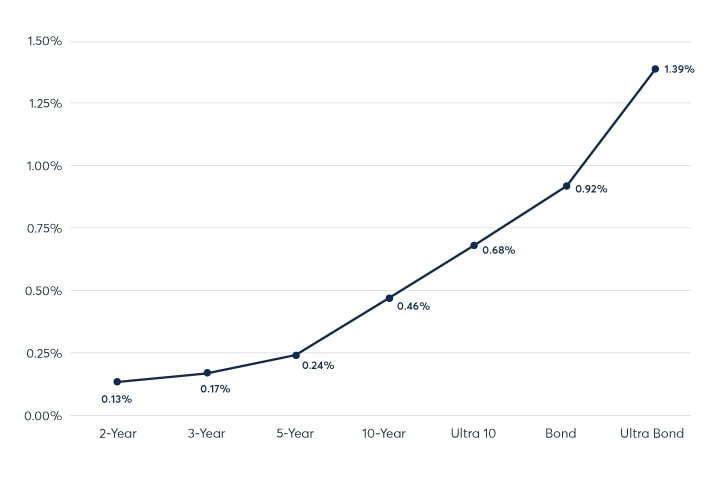

The 3-year is clearly a distinct point on the Treasury curve, both for purposes of position management and yield curve spreads. Please refer to Exhibit 1 for a chart of implied Treasury futures yields from our Treasury Analytics tool, powered by QuikStrike.

Exhibit 1: Treasury futures implied yields, Sep 14, 2020

{kind=link}

Source: QuikStrike Treasury Analytics

As with all Treasury futures, CME Group offers a full complement of inter-commodity spreads listed on CME Globex to efficiently execute 3-Year Note yield curve spreads. The most actively traded 3Y spreads are the adjacent tenors, 2Y and 5Y. Currently, the Dec-20 2Y (ZTZ0) vs. 3Y (Z3NZ0) spread (TYT) has an approximately DV01 neutral ratio of 3:2. By selling the spread, you are selling the front leg and buying the deferred tenor. Selling one spread produces two exposures: short three ZTZ0 contracts and long two Z3NZ0 contracts.

According to the Treasury Analytics tool, Dec 2020 2-Year Note and 3-Year Note futures had DV01s of $36.95 (2-Year) and $61.69 (3-Year) as of Sep 14, 2020. The short ZTZ0 exposure has a DV01 of -$110.85 (=-3*36.95). The long Z3NZ0 exposure has a DV01 of $123.38 (=2*$61.69). Therefore, the combined positions from one TYT spread has a tail of $12.53 (= (-$110.85) + $123.38) to manage with additional 2-Year Note futures to be risk neutral in terms of DV01 exposure.

Suppose you need to execute 2Y vs. 3Y (TYT) yield curve spreads that either results in a position of being long 200 Z3NZ0 contracts due to rolling a risk neutral position from ZTZ0 or establishing a risk neutral yield curve spread. In either case, you would have a tail of 34 ZTZ0 contracts to manage via the outright order book. As demonstrated in the table below, spreading 334 ZTZ0 and 200 Z3NZ0 produces nearly a risk neutral exposure with a tail of -$3.30, which is small relative to the tail, $1253, prior to hedging.

Exhibit 2: 2Y vs. 3Y Treasury futures yield curve spread positions, Sep 14, 2020

| Tenor | Futures DV01 | Contracts | Spread Leg DV01 |

| 2Y | $36.95 | -300 | -$11,085.00 |

| 3Y | $61.69 | 200 | $12,338.00 |

| Sum of Spread Legs (Spread Tail) |

$1,253.00 | ||

| Additional 2Y (Tail/Futures DV01) | 33.911 | ||

| 2Y Leg DV01 w/Hedged Tail | -$12,341.30 | ||

| Sum of Legs w/Hedged Tail | -$3.30 | ||

For more analysis of inter-commodity (yield curve) spreads, Treasury futures DV01s, and our implied yield curve, check out our Treasury Analytics tool.